This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

4 New $ Deals Launched; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers & Losers

June 21, 2022

US equity markets were closed on Monday due to Juneteenth holiday. US 10Y Treasury yields were 6bp higher at 3.23%. European markets inched higher with the DAX, CAC and FTSE were up 1%, 0.6% and 1.5% respectively. Brazil’s Bovespa ended almost unchanged. In the Middle East, UAE’s ADX closed 1% lower while and Saudi TASI gained 0.6%. Asian markets have opened on a positive note – Shanghai, HSI, STI and Nikkei were up 0.1%, 1.2%, 0.7% and 1.8% respectively. US CDS markets were closed. EU Main CDS spreads were 3.1bp tighter and Crossover spreads were also narrowed by 4.7bp. Asia ex-Japan IG CDS spreads tightened 2.8bp.

This masterclass will be conducted by Asian bond and liability management expert Florian Schmidt and will cover sovereign debt crises and solutions, key elements of a debt restructuring, restructuring mind map, creditor types, restructuring frameworks, case studies and discussion on Sri Lanka. The masterclass is ideal for bond investors, advisors, wealth managers and relationship managers.

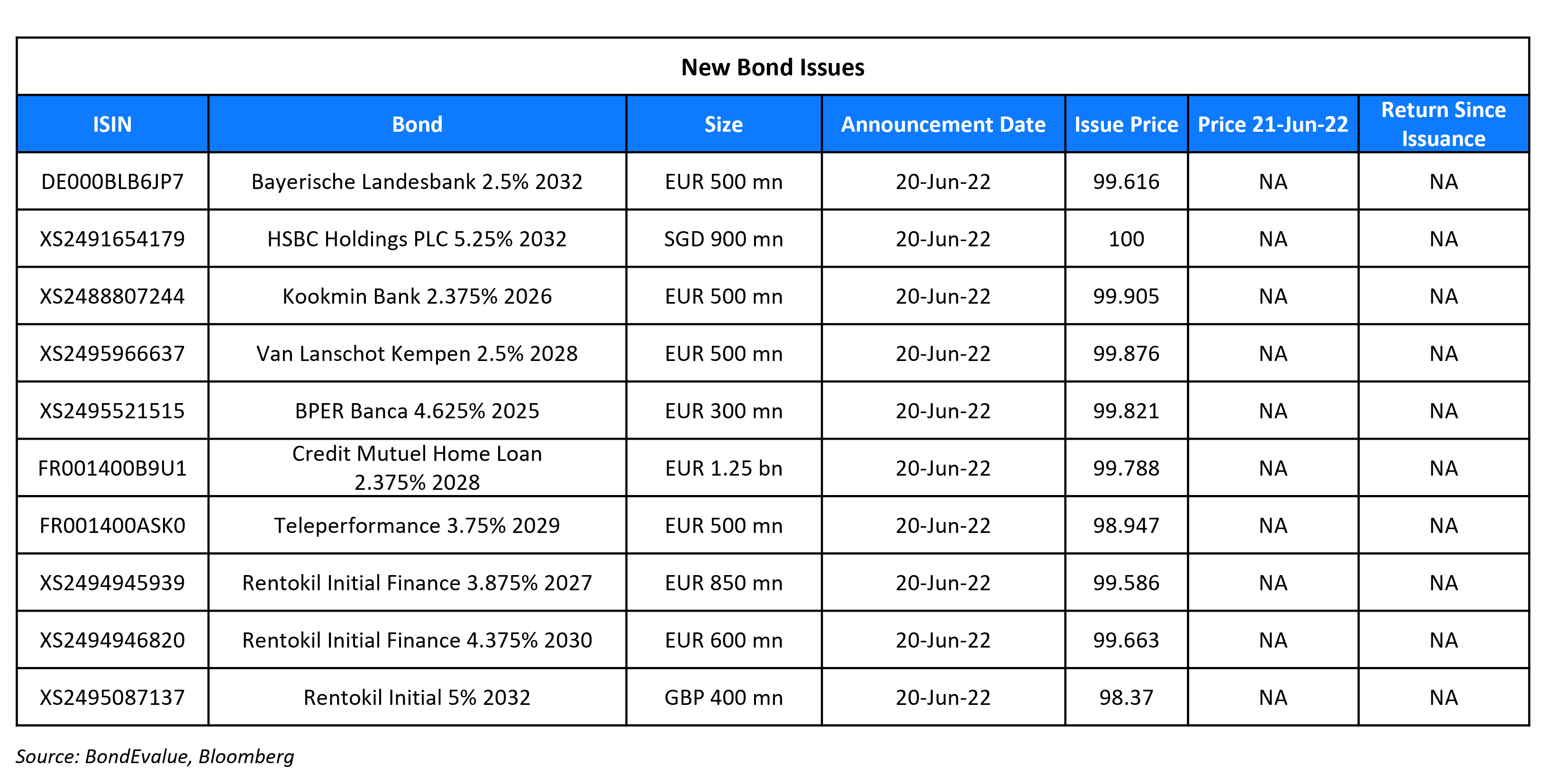

New Bond Issues

- Linyi City Development Group $ 3Y at 5.5% area

- Korea Western Power $ 3Y Green at T+130bp area

- Hanwha Energy $ 3Y Green at T+125bp area

- Fujian Jinjiang Urban Construction $ 364-day at 4.8% area

HSBC Holdings raised S$900mn via a 10NC5 Tier 2 bond (Term of the Day, explained below) at a yield of 5.25%, 25bp inside initial guidance of 5.5% area. The bonds are rated Baa/BBB/A-, and received orders over S$1bn, 1.1x issue size. Proceeds will be used for general corporate purposes and to strengthen the bank’s capital base under UK regulations. HSBC last issued SGD-denominated bonds in 2018, raising $750mn via an AT1 at a yield of 5%. It is the third foreign bank to borrow money for tier 2 capital purposes in the Singaporean markets this year after Credit Agricole’s S$250mn 10.5NC5.5 at 3.95% in April and BNP Paribas’ S$350mn 10NC5 in February at 3.125%.

Rentokil raised a multi-currency three-tranche deal. It raised

- €850mn via a 5Y bond at a yield of 3.968%, 30bp inside initial guidance of MS+200bp area.

- €600mn via a 8Y bond at a yield of 4.426%, 30bp inside initial guidance of MS+230bp area.

- £400mn via a 10Y bond at a yield of 5.147%, 20bp inside initial guidance of UKT+275bp area.

The bonds have expected ratings of BBB (S&P). The proceeds will be used for general corporate purposes, and for the refinancing of bridge loans and other obligations in relation to the acquisition of Terminix, announced on December 14, 2021.

Kookmin Bank raised €500mn via a 3.5Y sustainability bond at a yield of 2.405%, unchanged from initial guidance of MS+27bp. The bonds have expected ratings of AAA/AAA (S&P/Fitch). The new bonds are priced roughly in-line with its existing 0.048% 2026s that yield 2.41%.

New Bonds Pipeline

- GS Caltex hires for $ bond

- BNZ hires for € bond

- Jinjiang Road and Bridge Construction hires for $ bond

- Busan Bank hires for $ Social bond

- Continuum Energy Aura hires for $ Green Bond

Rating Changes

- Moody’s changes BRF’s outlook to stable from positive; affirms Ba2 ratings

- Moody’s downgrades Helenbergh to Caa1/Caa2; outlook remains negative

Term of the Day

Tier 2 Bond

Tier 2 bonds are debt instruments issued by banks to meet their regulatory tier 2 capital requirements. Tier 2 capital (and thus tier 2 bonds) rank senior to tier 1 capital, which consists of common equity tier 1 (CET1) and additional tier 1 (AT1) capital. CET1 consists of a bank’s common shareholders’ equity while AT1 consists of preferred shares and hybrid securities or perpetual bonds. Tier 2 capital consists of upper tier 2 and lower tier 2 wherein the former is considered riskier to the latter. From a bond investor’s perspective, tier 2 bonds are senior, and therefore less risky, compared to AT1 bonds as AT1s would be the first to absorb losses in the event of a deterioration in bank capital.

Talking Heads

On Larry Summers Says US Needs 5% Jobless Rate for Five Years to Ease Inflation

“We need five years of unemployment above 5% to contain inflation — in other words, we need two years of 7.5% unemployment or five years of 6% unemployment or one year of 10% unemployment. There are numbers that are remarkably discouraging relative to the Fed Reserve view… The gap between 7.5% unemployment for two years and 4.1% unemployment for one year is immense”

On ECB’s Policy Normalization Will Be Done Gradually – Bank of Portugal Governor Centeno

“The inflation phenomenon in Europe is very imported. From the point of view of monetary policy, the instruments exist and the availability to create new instruments is on the table. We are talking about instruments that will allow the introduction in the market of a set of market discipline, which at this moment seems not to exist… There will be a new insurance that will only be used in case of need, and if it is well designed it will probably never be used.”

On RBA’s Lowe Signals 25-to-50 Basis-Point Rate Hike in July

“We’re going to look at the data we have each month and the level of interest rates and the inflation rate. I expect that next month we’ll be having the same discussion at our board meeting– 25 or 50 basis points… I don’t think it’s particularly likely, but the market has been a better judge of where interest rates are going than we have over the past few years”.

On ECB Will Act With ‘Cool Head’ on Market Volatility – Governing Council member Martins Kazaks

“If action is going to be necessary, we will be on top of it. It is natural to see some increased uncertainty and volatility. We need to live through this situation with a cool head and steady hand showing to the market, what’s our direction… This is in a way natural to see increased volatility after years of monetary policy not raising the rates”.

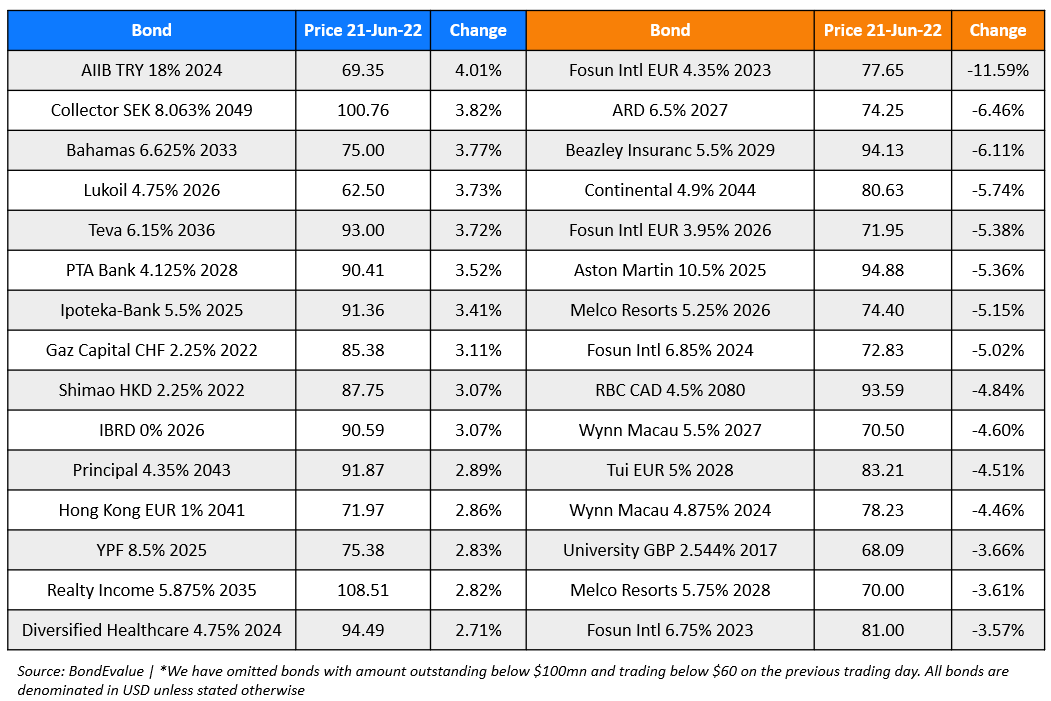

Top Gainers & Losers – 21-June-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.