This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

66% of Dollar Bonds Traded Higher in May 2021 with IG Outperforming

June 1, 2021

The month of May continued April’s trend with 66% of dollar bonds in our universe delivering a positive price return ex-coupon during the month. Bond investors are on track for an upbeat Q2 after a dismal Q1, especially in February and March when 66% and 82% of dollar bonds delivered negative price returns respectively.

Both Investment Grade (IG) and High Yield (HY) bonds performed well with the former performing relatively better after months of underperformance. 70% of IG dollar bonds ended higher in May, compared to 62% of HY bonds that ended May in the green.

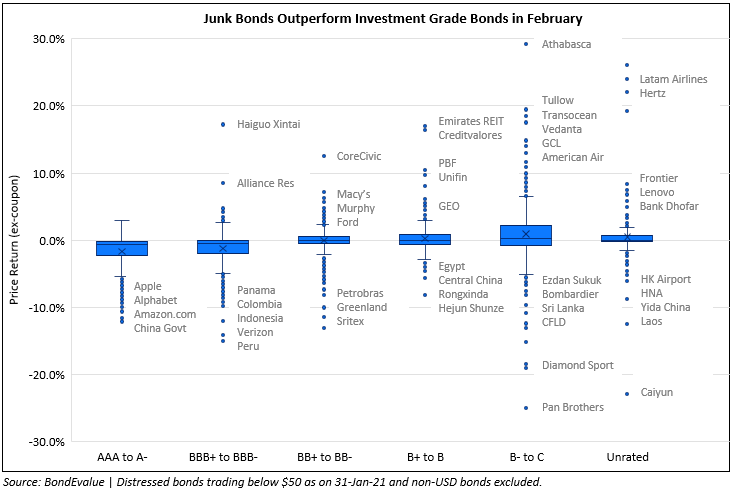

The box and whisker plot above shows the price return of IG dollar bonds in May by rating. Huarong’s bonds due 2022 and beyond once again dominated the losers falling 7-12% in May. In contrast, Huarong’s 2021s inched higher during the month as news emerged of Huarong wiring money to repay its maturing bonds.

Below is a similar box and whisker plot for HY dollar bonds’ price return in May by rating.

-PNG.png?width=1084&upscale=true&name=Price%20Return%20of%20HY%20Dollar%20Bonds%20in%20May%202021%20(1)-PNG.png)

Most notable movers in the junk bond space were HNA Group’s 6.25% 2021s that lost over 60% of their value falling from ~56 to ~22 cents on the dollar. Another noteworthy name was Malaysian corporate Serba Dinamik, whose dollar bonds have plummeted 30-40% over the last few days on the back of audit concerns. Yunnan Energy’s bonds rose 10-15% after news of the company providing 460mn shares of Shanghai-listed Lancang River Hydropower as collateral for debt payments. The company said that the pledge would last for one year and that it will be able to repay bondholders. Among the LatAm names, Brazil’s Andrade Gutierrez’s bonds rose 40-50% on the back of a PE-fund acquiring a 14.86% stake in infrastructure company CCR, which is controlled by Andrade.

Issuance Volume & Largest Deals

Global corporate dollar issuance volume stood at $133.6bn for May 2021 down 41% vs. last May’s issuance of $225bn and 23% higher than April’s issuance.

APAC ex-Japan & Middle East G3 issuance stood at $34.1bn, just 6% lower vs. last May’s issuance of $36.2bn, and 9% lower than last month’s issuance of $37.4bn.

The largest deals last month were dominated by Amazon’s $18.5bn eight-trancher that received orders of ~$50bn. Other large deals include UnitedHealth’s $3bn dual-trancher, Abu Dhabi’s $2bn 7Y issuance and JPMorgan’s $2bn PerpNC5 AT1.

In the APAC & Middle East region, besides Abu Dhabi’s $2bn issuance, Mubadala’s $1.5bn dual-trancher and New World Development (NWD)’s $1.2bn PerpNC7 led the issuances. Other large deals from the region included GLP China’s $950mn Perp, Enn and Chinalco’s 5Y issuances worth $800mn and Emirates NBD’s $750mn PerpNC6 AT1.

The month of May also saw a 3 month high in AT1 issuance volumes at $13bn. These included UBS’s $750mn PerpNC5, Santander’s$1bn PerpNC5 , SocGen’s $1bn PerpNC5, Emirates NBD’s $750mn PerpNC6 and Oman Arab Bank’sdebut $250mn PerpNC5 besides other issuances

Top Gainers & Losers

The top gainers and losers were dominated by Asian corporates. HNA Group and Serba Dinamik were the biggest losers with the former dropping a massive 35 cents on the dollar on a single day while Serba Dinamik’s bonds fell ~40 cents after they were hit by concerns over an audit report with the company coming out yesterday clarifying the issue. China Huarong continued to stay in the losers list for another month as investor concerns continue to weigh on the company – despite the company showing that they are willing and able to keep good on their bonds. On the gainers side, Yestar’s bonds due 2021 rallied even as Moody’s lowered their credit rating and warned of the company defaulting in April. Other large gainers included Chinese SOEs like Chongqing Energy, Yunnan Metro/Energy. Sri Lanka’s bonds saw another positive month with their 5.75% 2023s up ~11%.

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.