This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Barclays Launches S$ Perp; Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

March 1, 2023

US Treasury yields were 2-4bp higher across most of the curve. The peak Fed funds rate grinded another 1bp higher to 5.42% for the September 2023 meeting. Despite the stronger data, markets continue to price in a 25bp hike at each of the Fed’s next three meetings in March, May and June, based on the CME’s maximum probability calculations. US IG and HY CDS spreads widened by 0.9bp and 4.2bp respectively. The S&P and Nasdaq ended lower on Tuesday, down by 0.3% and 0.1%.

European equity markets ended lower. European main CDS spread tightened by 1.7bp and the crossover CDS spread widened 3.1bp. French inflation jumped by 7.2%, higher than the 7% forecasted. Spain’s inflation came at 6.1% higher than the 5.7% forecasted. With this, the German short-end Schatz yields rose 7bp. Asian equity markets have opened in the green for a second straight day. Asia ex-Japan CDS spreads tightened by 0.9bp.

February saw a reversal in fortunes for bond investors after a stellar performance in January. 85% of the dollar bonds in our universe delivered a negative price return (ex-coupon) vs. 92% showing positive returns in January. For more details on the performance of IG and HY bonds, issuance volumes and top gainers and losers in February, watch out for our monthly roundup that will be sent later today.

.png)

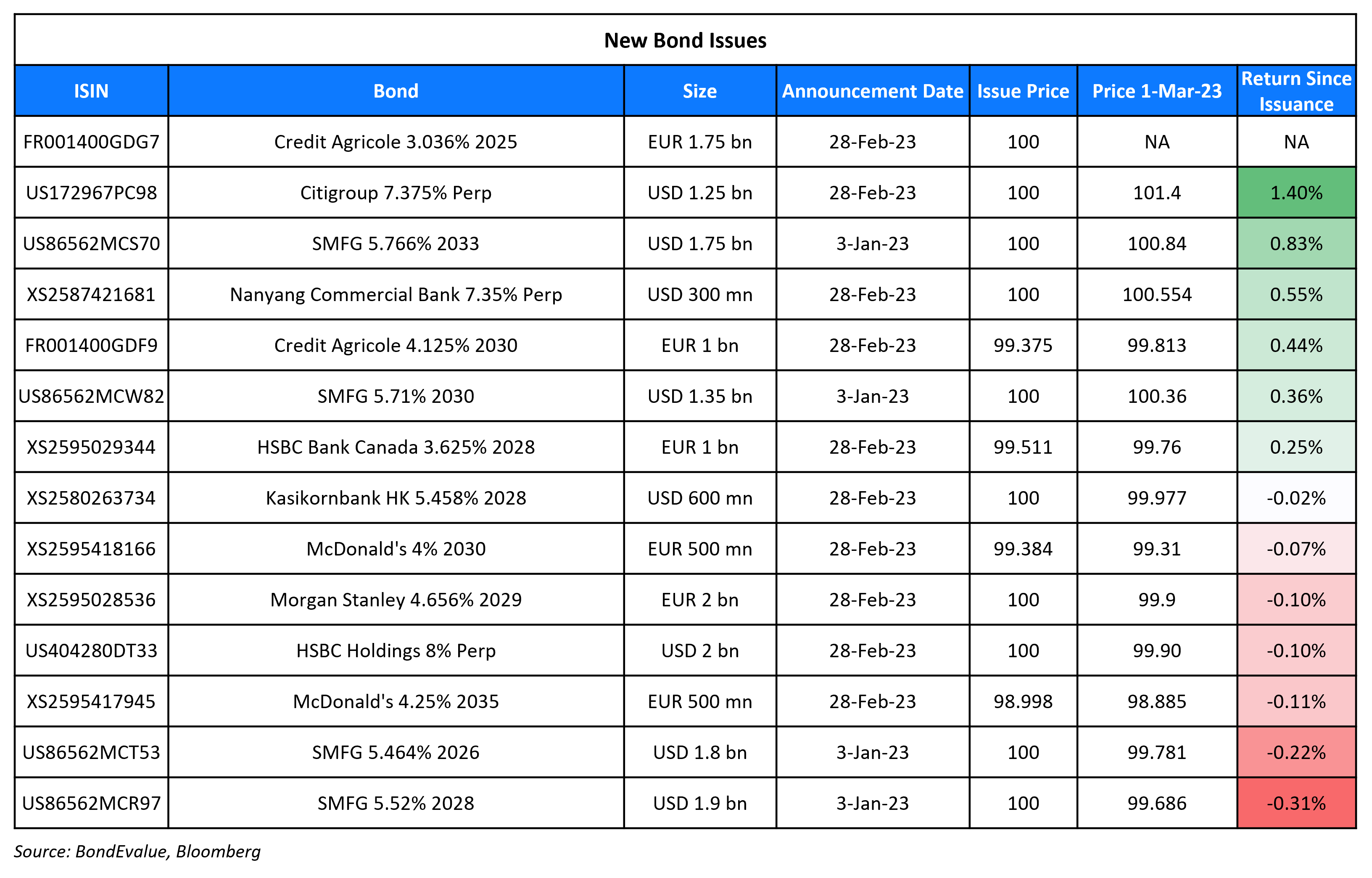

New Bond Issues

- Barclays S$ PrepNC15June2028 at 7.65% area

- Teva Pharmaceutical $500/500mn 6.5Y/8.5Y at 8.125/8.375% areas & €500/500mn 6.5Y/8.5Y at 7.75/8.25% areas

New Bonds Pipeline

- Sumitomo hires for $ 5Y bond

- REC hires for $ Long 5Y Green bond

- Morocco hires for $ bond

- Qatar plans for $ bond

Rating Changes

- Moody’s downgrades Pakistan’s rating to Caa3; changes outlook to stable from negative

- Adler Real Estate AG Downgraded To ‘CC’ From ‘CCC-‘ On Proposed Amendment Of Bond Terms; Outlook Negative

Term of the Day

Credit Default Swap (CDS)

A Credit Default Swap (CDS) is a financial contract between two counterparties that allows an investor to “swap” or offset the credit risk with another investor. CDS acts like an insurance policy wherein the buyer makes regular payments to the seller to protect itself from an issuer default. In the event of a default, the buyer receives a payout, typically the face value of the bond or loan, from the seller of the CDS as per the agreement. CDS spreads are a commonly used metric to track the market-priced creditworthiness of an issuer. A widening (increase) in CDS spreads indicates a deterioration in creditworthiness and vice-versa.

Talking Heads

On Euro-Area Bonds Slide as Traders Lift Peak ECB Rate Bets to 4%

Piet Christiansen, chief strategist at Danske Bank

“Markets have not fully priced in the peak… It can push higher, in particular the May meeting pricing, which is still ‘only’ pricing a coin toss probability between 25bp and 50bp”

Francesco Maria di Bella, a strategist at UniCredit

“Investors perceive a very sticky inflation. This would keep the ECB very hawkish.”

On Fed might raise policy rates to 6% – BofA

“Aggregate demand needs to weaken significantly for inflation to return to the Fed’s target. Further supply-chain normalization and a slowdown in the labor market will help, but only to a degree… Moreover, these processes are taking longer than we and markets were expecting”

On Regulator censures Credit Suisse for Greensill blunders

Gerhard Andrey, a Swiss lawmaker

“We don’t need more box ticking. We don’t need more box ticking”

Credit Suisse CEO Ulrich Koerner

The announcement “underlines the importance of the actions we have taken in recent years to strengthen our risk and compliance culture”

On Barclays, NatWest seeing Fed upping rate hike pace in March

NatWest Markets chief US economist Kevin Cummins

“Given (Friday’s) inflation backdrop, and the fact our monthly core inflation profile now shows the Fed’s preferred core PCE deflator holds above 4% YoY through July, we are raising our Fed funds terminal rate forecast to 5.75%.

Barclays

The bond market has moved to “higher for longer,” feeding negative reactions in credit”

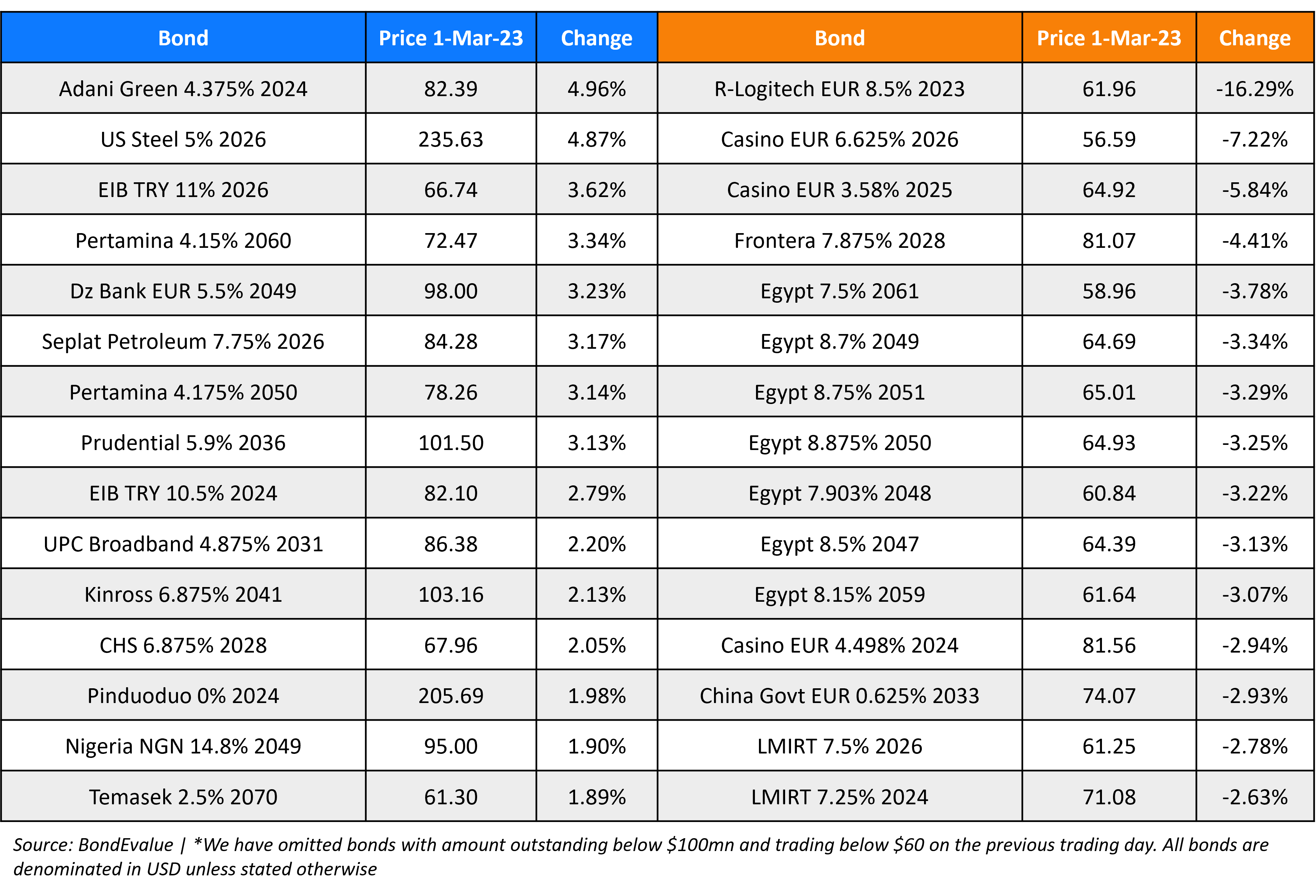

Top Gainers & Losers – 01-March-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.