This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Bonds Rally After a Lower-Than-Expected CPI of 7.1%

December 14, 2022

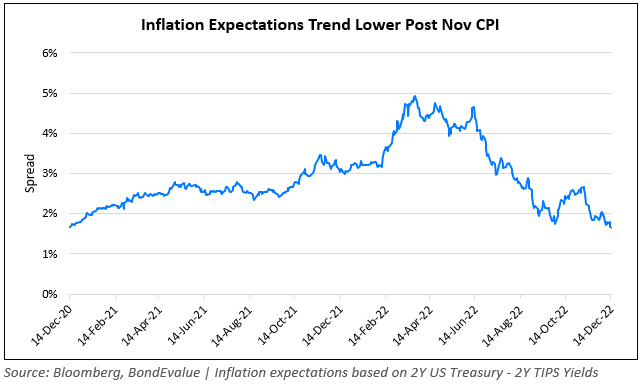

US Treasuries rallied sharply with yields lower by 15bp on the 2Y and by 10bp on the 10Y after the US CPI inflation print for November came at 7.1%, lower than expectations for a 7.3% print. Core CPI was also softer at 6% vs. expectations of 6.1%. The peak Fed Funds rate subsequently fell by 13bp to 4.85% for the May 2023 meeting. Inflation expectations measured by the difference between the nominal 2Y Treasury yield and that of similar maturity TIPS (Term of the Day, explained below) has now fallen to 1.65% (165bp), levels last seen at end-2020.

The probability of a 50bp hike at the FOMC’s meeting today remains unchanged at 75%. However, the probability of a 25bp hike at the February 2023 is now at 56% vs. 35% before the inflation print while the probability of a 50bp hike at the same meeting has fallen to 38% from 51% earlier. US IG and HY CDS spreads tightened 2.1bp and 24.9bp respectively. US equity markets jumped with the S&P and Nasdaq up 0.7% and 1% respectively on Tuesday.

European equity markets ended higher too. EU Main CDS spreads tightened 4.9bp and Crossover spreads tightened by 16.8bp. Asian equity markets have opened higher today by over 0.5%. Asia ex-Japan CDS spreads tightened by 8.9bp.

New Bond Issues

- Jiangyin State-owned Assets € 3Y at 5.35% area

New Bonds Pipeline

- Korea Investment & Securities hires for $ Green bond

- Zhongrong International Trust hires for $367mn Short 1Y bond

- TSMC Arizona hires for $ bond

Rating Changes

Term of the Day

TIPS

TIPS or Treasury Inflation-Protected Securities are fixed income securities issued by the US Treasury whose returns are linked to the inflation rate. TIPS provide investors protection against inflation by adjusting the principal higher with inflation and lower with deflation, as measured by the Consumer Price Index (CPI). At maturity, investors are paid the higher of the adjusted principal or the original principal. Interest on TIPS is fixed, paid out twice a year and is applied to the adjusted principal. As investors expect inflation in the US to climb higher, demand for TIPS is likely to increase.

Talking Heads

On Bond Traders Betting on Rates Downshift Have Fed Hurdle to Clear

Gene Tannuzzo, global head of fixed income at Columbia Threadneedle

“The Fed has ample room to decelerate the pace of hikes. It gives them room to stop hiking early next year but they are still going to want to send the message that they are going to want to hold rates — as opposed to signaling cuts that the market’s got priced in”

John Madziyire, a fund manager at Vanguard Group

“Our bias is to fade this rally and look to how people position in early January… The return of inflows for bond funds means there has been more comfort in adding duration”

On Investors seeing returns in depressed Asian dollar bonds, but risks too

Amy Kam, senior PM at Aviva Investors

“Because of the prolonged distress, I think there is a lot of mispricing. And you can afford to have your (risk) threshold high and get involved… you need some guts and understanding of companies’ operations and liabilities. You can pick and choose, just because everything is really, still, quite cheap”

T Rowe Price’s Kwan

“While we have participated in the rally (because of existing positions), we haven’t increased. Investors who have invested a large amount in South Asia, in India or Indonesia may now reallocate to North Asia with China opening up”

Morgan Stanley strategists

“We believe 2023 will be the year for Asia IG, given its once-in-a-decade yield, cheap spread valuation, lower US Treasury yield and supportive fund inflows”

On China Dollar Bonds Showing Least Stress Since Evergrande Meltdown

Chang Wei Liang, a macro strategist at DBS Bank

“Risks of defaults have receded in the short term, and we still see scope for credit of quality developers to outperform”

Fidelity International fixed-income portfolio manager Belinda Liao

“The winners in the space will be those that are the direct beneficiaries of the policy support”

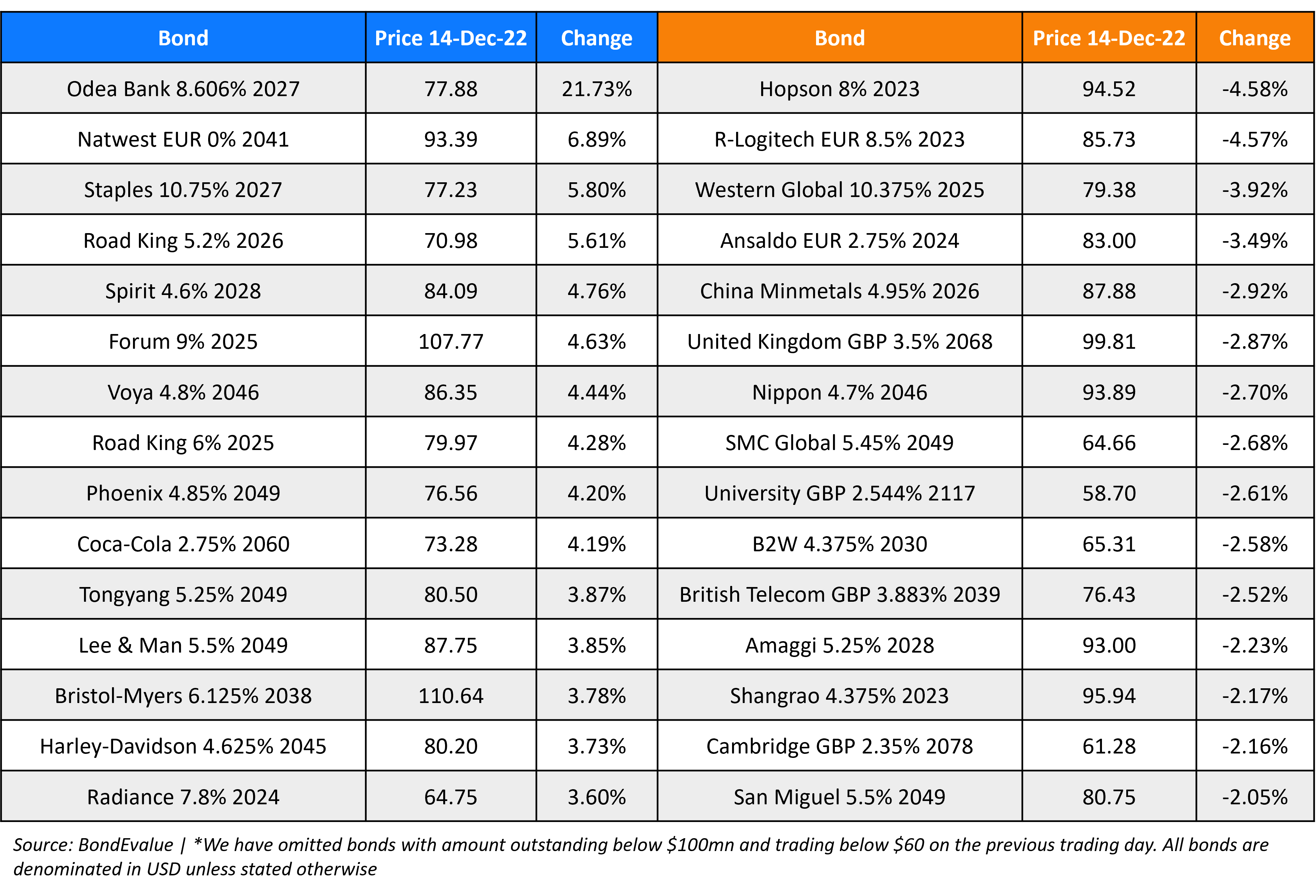

Top Gainers & Losers – 14-December-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.