This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

CICC HK Launches $ Bond; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

November 15, 2022

US Treasury yields moved up ~5bp on Monday after Fed governor Waller’s comments on rates moving higher and staying higher for longer, before easing slightly. The peak Fed Funds rate eased by 1bp to 4.92% for the June 2023 meeting. Probabilities of a 50bp hike at the FOMC’s December meeting now stand at 81%. US equity markets dropped with S&P and Nasdaq down 0.89% and 1.12% respectively.

European equity markets on the other hand were broadly higher with the FTSE up 0.92% and DAX up 0.62%. EU Main CDS spreads tightened 1.6bp. Asian equity markets have opened mixed today. Asia ex-Japan CDS spreads witnessed a second consecutive day of sharp tightening, 16bp lower following the 25bp easing on Monday. Meanwhile, India’s CPI came in at 6.77% for October, in line with expectations and below September’s print of 7.4%.

%20x%20311px%20(h).jpg?upscale=true&width=1400&upscale=true&name=Tablet%20banner%20661px%20(w)%20x%20311px%20(h).jpg)

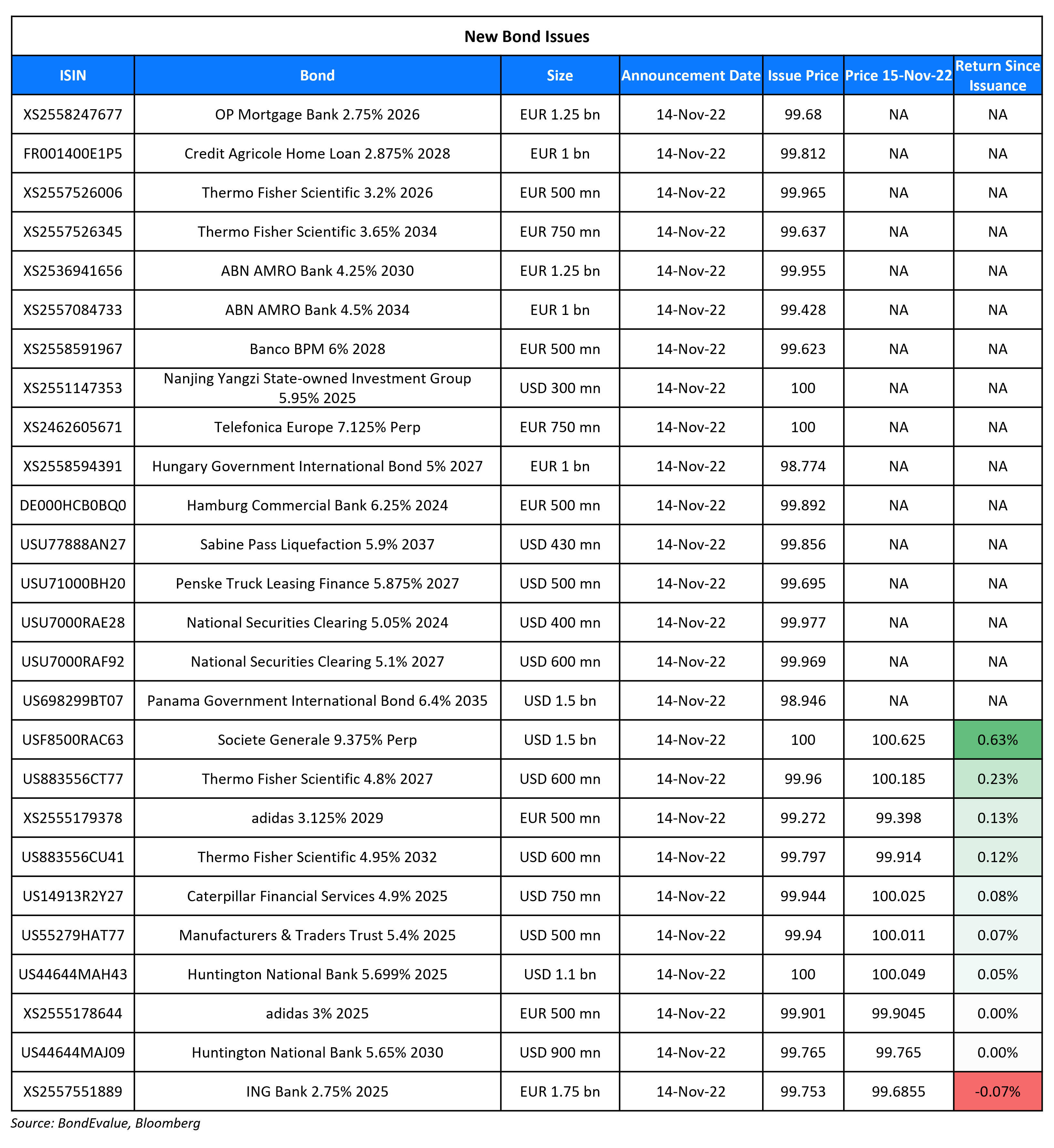

New Bond Issues

-

CICC Hong Kong Finance $ 3Y @ T+150bp area

Societe Generale raised $1.5bn via a PerpNC5.5 at a yield of 9.375%, a solid 62.5bp inside initial guidance of 10% area. The Additional Tier 1 bonds have expected ratings of Ba2/BB/BB+. If not redeemed, the coupon rate resets every five years at the 5Y UST plus a margin of 538.5bp. The new bonds are priced at a new issue premium of 10.5bp vs. its existing 5.375% 2049s that currently yield 9.27%.

The Republic of Panama raised $1.5bn via a long 12Y bond at a yield of 6.528%, 25bp inside the initial guidance of T+290bp area. The bonds have expected ratings of Baa2/BBB/BBB-. Proceeds will be used for general budgetary purposes & liability management. The new bonds are priced 50.8bp wider to its existing 3.298% 2033s that yield 6.02%.

ING Bank raised €1.75bn via a 3Y Covered bond at a yield of 2.837%, 4bp inside the initial guidance of MS+6bp area. The Dutch legislative covered bonds, guaranteed by ING Covered Bond Co BV, received orders over €2.25bn, 1.3x issue size.

New Bonds Pipeline

- Double Dragon hires for tap of $130mn 7.25% 2025s

- Korea Investment & Securities hires for $ Green bond

Rating Changes

- Fitch Upgrades Methanex Corporation’s IDR to ‘BB+’; Outlook Stable

- Vodafone Group PLC Outlook Revised To Positive Following Announced Joint Venture To Co-Control Vantage Towers

Term of the Day: Reverse-Yankee Bond

Reverse-Yankee Bond is a bond issued by a US company outside of the US and denominated in a currency other than USD. For example, a US issuer raising debt in Europe denominated in EUR would be considered to be issuing a reverse-yankee bond. In comparison, Yankee Bonds are a type of Eurobond issued and traded in the US and are denominated in USD. Thus, if a foreign non-US based company issues a USD bond which is traded in the US, the bond is considered a Yankee Bond.

American company Thermo Fisher raised €1.25bn via a two-trancher reverse-yankee bond issuance.

Talking Heads

On US Skirting Recession in 2023, But Europe Not Being So Lucky

Morgan Stanley

“Britain and the euro zone economies are likely to tip into recession next year, but the United States might make a narrow escape thanks to a resilient job market…At the same time, China’s expected reopening after almost three years of COVID-19 curbs is set to lead a recovery in its own economy and other emerging Asian markets…The U.S. economy just skirts recession in 2023, but the landing doesn’t feel so soft as job growth slows meaningfully and the unemployment rate continues to rise.”

On Beijing’s Measures to Ease Credit Crunch Being a ‘Turning Point’ for China’s Developers

Raymond Cheng, managing director of CGS-CIMB Securities

“It is the most aggressive policy so far by regulators to save the property market in China…Overall, we assess that these policies, if implemented, should be able to ease developers’ liquidity pressure markedly in the near term.”

Wang Tao, Economist at UBS

“Together with the previous 250-billion-yuan [US$35.4 billion] bond sale programme support, we view this may mark a turning point for the property sector, as the government is turning to support developers on top of supporting industry.”

Shujin Chen, Jeffries analyst

“The measures focus on providing financing support to property developers, to ensure house delivery, to help dispose of risky projects, to homebuyers with liquidity difficulties, and for home rental projects…It also extends the grace period for banks to fulfill the property/mortgage cap, a critical move to reduce banks’ concerns when increasing mortgage and property-development loans.”

On Chinese Property Bonds and Stocks Rallying on New Rescue Measures

Stephen Chang, managing director and portfolio manager at Pimco Asia Ltd.

“We are looking at this with a more favorable outlook…There are still a lot of risks but it seems like some of the tail risk has been clipped, with at least a more supportive measure and this more pragmatic thinking now.”

On Templeton’s Hasenstab Exiting Argentina Bet After Losing Billions

Diego Ferro, founder of M2M Capital

“The bet was horrendous, and on one hand, you can fault Franklin Templeton for making it because similar wagers in Argentina have always ended in tears. At the same time, people in government were saying all the right things, were credible at the time, and made a lot of promises,” adding that “of course, hindsight is 20/20”

Jared Lou, portfolio manager for EM debt at William Blair

“The country once again finds itself in a place of stagnating growth and high inflation. Although many expect regime change in next year’s elections, its unclear how many dollars will be left in the central bank when a new government takes over, raising fresh concerns about Argentina’s ability to pay its debts”

On US Envoy Saying Zambia Restructure Must Involve Haircuts – US Ambassador Michael Gonzales

“Every single one of the creditors needs to reduce the capital, the principal that is owed. Not just restructure so that the Zambian people keep paying longer and more into perpetuity, but taking what we call a haircut… There’s a lot of stinky debt. There’s a lot of shenanigans that went into the debt that the Zambian people are now saddled with for a generation”.

On Morgan Stanley seeing 150 bps in BoE rate cuts in 2024

“The BoE stops hiking as Bank Rate hits 4.0% in March 2023. With the inflation target in sight, and unemployment on the rise, we expect 150bp of cuts in 2024”

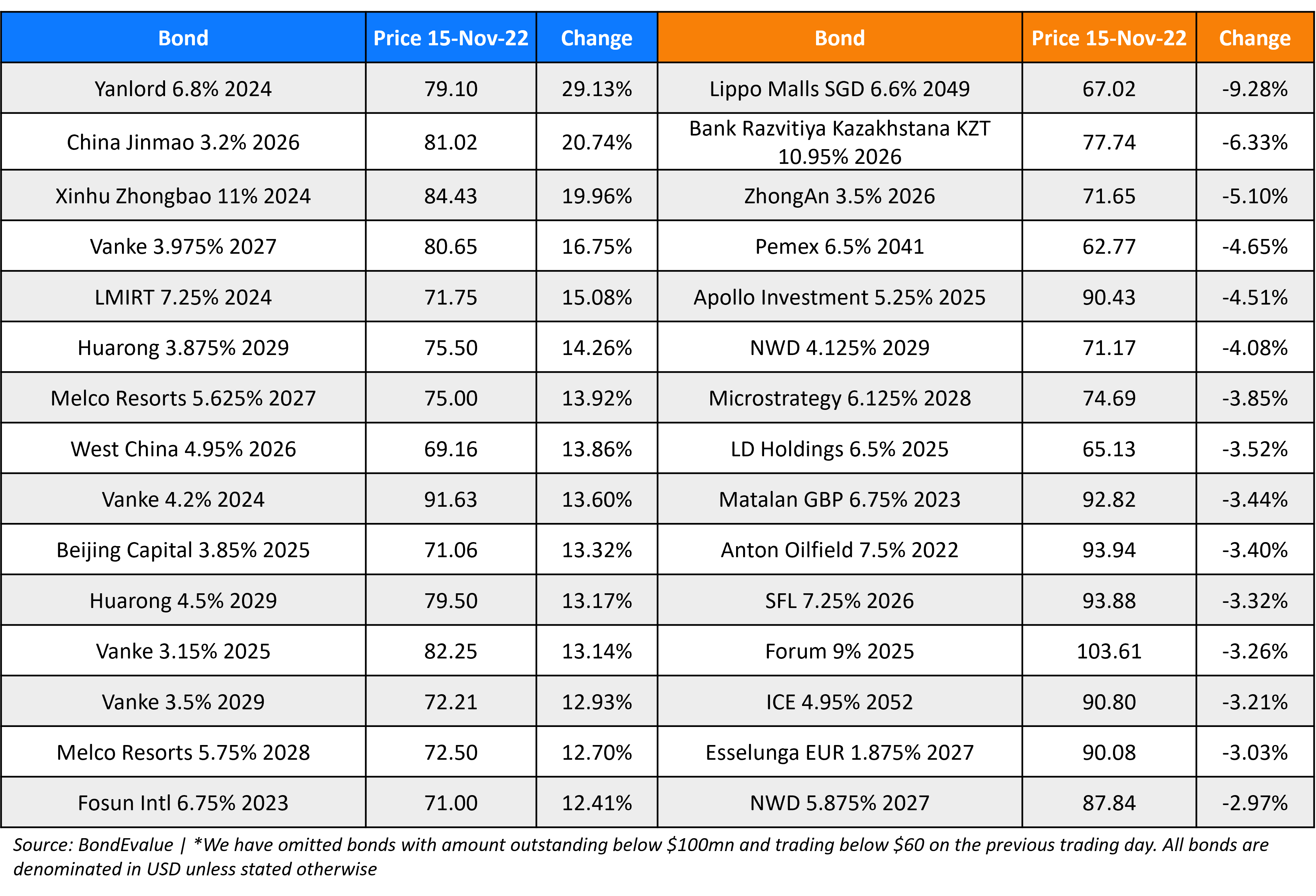

Top Gainers & Losers – 15-November-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.