This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

March 16, 2023

Markets saw a big risk-off move on Wednesday following panic and concerns over Credit Suisse, whose stocks and bonds plummeted to fresh lows (more details below). The selloff soon spread to the broader banking sector as the STOXX Europe 600 Banks Index ended almost 7% lower and the S&P Bank Index closed 3.6% in the red. This dragged the European equity indices lower by ~3.5%. Investors and traders rushed to safety, pushing the US Treasury curve below 4% – the 2Y fell 32bp to 3.94% while the 10Y fell 18bp to 3.48%.

.png)

European government bond yields also witnessed a sharp fall – 2Y German bund yields fell 42bp to 2.38%, the largest daily decline since 1995. The peak Fed funds rate fell 10bp to 4.86%. Markets continue to price in a 25bp hike next week with a 67% probability. US retail sales for February declined by 0.4%, more than Reuters’ estimate of a 0.3% decline. January’s number on the other hand was revised up from 3.0% to 3.2%. Credit spreads in the US rose – US IG and HY CDS spreads widened 3.2bp and 19.0bp respectively. The S&P and Nasdaq ended mixed.

European equity markets fell sharply on the back of the selloff in banking stocks. European main and Crossover CDS spreads spiked 12.8bp and 55.5bp respectively. Asia ex-Japan CDS spreads widened a further 5bp. Asian equity markets have opened with a negative bias led by the Hang Seng down 1.5%.

New Course on Bonds for Individual Investors | 13 and 27 April 2023

.png)

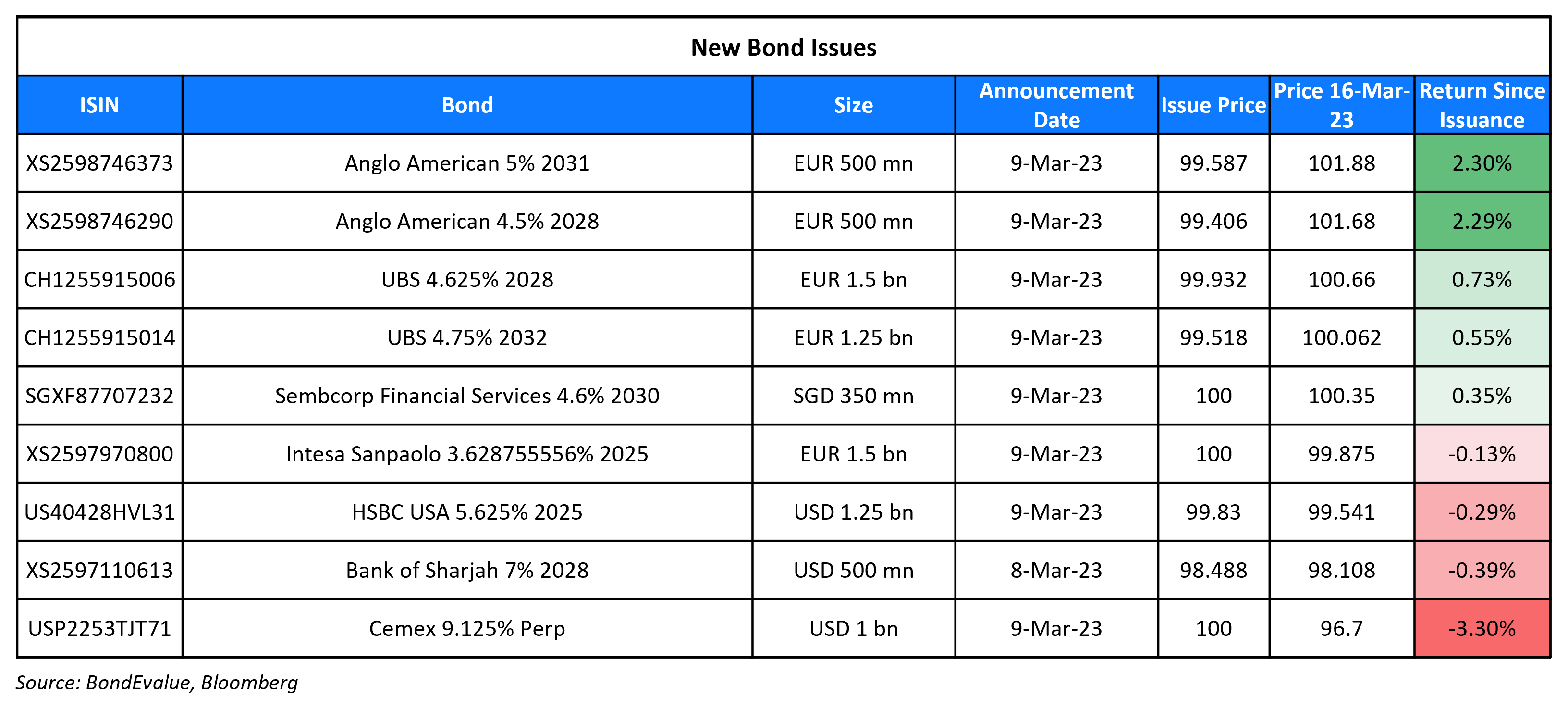

New Bond Issues

New Bonds Pipeline

- Shinhan Bank hires for $ senior bond

- REC hires for $ Long 5Y Green bond

- Qatar plans for $ bond

Rating Changes

- Gol Linhas Aereas Inteligentes S.A. Upgraded To ‘CCC+’ From ‘SD’ On New Capital Structure, Outlook Positive

- Moody’s downgrades BRF S.A. ratings to Ba3; outlook is stable

- Diamond Sports Group Debt Ratings Lowered To ‘D’ On Chapter 11 Bankruptcy Filing; All Ratings Subsequently Withdrawn

- Fitch Revises Pfizer’s Outlook to Stable; Affirms IDR at ‘A’

- Bolivia Long-Term Ratings Placed On CreditWatch Negative On International Reserves Pressure; Short-Term Ratings Affirmed

Term of the Day: Tender Offer

A tender offer is an offer made by an issuer to bondholders to buyback their bonds. In return, the bondholders could get either cash or new bonds of equivalent value at a specified price. The issuer does this to retire some of its old debt and can use retained earnings to fund the purchases without affecting the liquidity position of the company. Tender offers have a deadline date before which holders must tender their bonds back.

Talking Heads

Jose Mosquera, Chief Investment Officer at hedge funds Rho Investments and Quadriga Credit Opportunities

“Short-term CDS in Credit Suisse is almost impossible to source and bids for senior bonds are very limited, whilst we are seeing extensive supply of subordinated bonds at distressed levels … leads me to think that the market is pricing a very high chance of a bank resolution involving full share burden by sub debt holders.”

Credit Suisse erupts into crisis

Mark Heppenstall, president of Penn Mutual Asset Management.

“The trading levels have become somewhat a crisis in confidence in Credit Suisse … People are looking for any way possible to get protection.”

Scott Kimball, managing director of fixed income at Loop Capital Asset Management

“Credit Suisse is a global systemically important banking institution … The persistent problems at Credit Suisse carry bigger problems for the credit markets … They can’t seem to get the ship right.”

Alison Williams and Ravi Chelluri, Bloomberg Intelligence

“CDS and stock prices can drive a negative feedback loop, especially in volatile markets … Credit Suisse’ risk-management issues have evolved over the past couple of years, and we think that big banks have managed counterparty-risk exposures accordingly.”

On challenges to trade in big bond markets after bank rout

Jon Jonsson, senior fixed income portfolio manager at Neuberger Bergman

“Liquidity is poor pretty much across … most fixed income asset classes … (trades) that should take seconds took minutes”

Nils Kostense, head of government bond trading at ABN AMRO in Amsterdam

“Definitely, compared to yesterday afternoon, liquidity has been drying up … These fierce moves on the curve make it rather difficult getting liquidity. Small inquiries are no issue, these are still taken care of, but it’s bigger-size trades where there won’t be any liquidity. Traders are definitely not keen to get risk on the books … We don’t have these big buying forces in the background like we had in the past years”

Zhiwei Ren, portfolio manager at Penn Mutual Asset Management

“The ability to trade in and out of positions is definitely worse than the Ukraine war. The bid-ask is three to four times wider than normal, that was my experience (on Monday)”

Kaspar Hense, BlueBay Asset Management senior fund manager

“Because there have been a lot of others, namely these hedge funds, which had been on the one side and needed to stop out, that’s why liquidity was good,”

BlackRock CEO Fink on financial risks and persistent inflation

Laurence Fink, Chief Executive at BlackRock

“Bond markets were down 15% last year, but it still seemed, as they say in those old Western movies, ‘quiet, too quiet,’ … Something else had to give as the fastest pace of rate hikes since the 1980s exposed cracks in the financial system … (inflation) more likely to stay closer to 3.5% or 4% in the next few years … The monetary and fiscal tools available to policymakers and regulators to address the current crisis are limited, especially with a divided government in the United States”

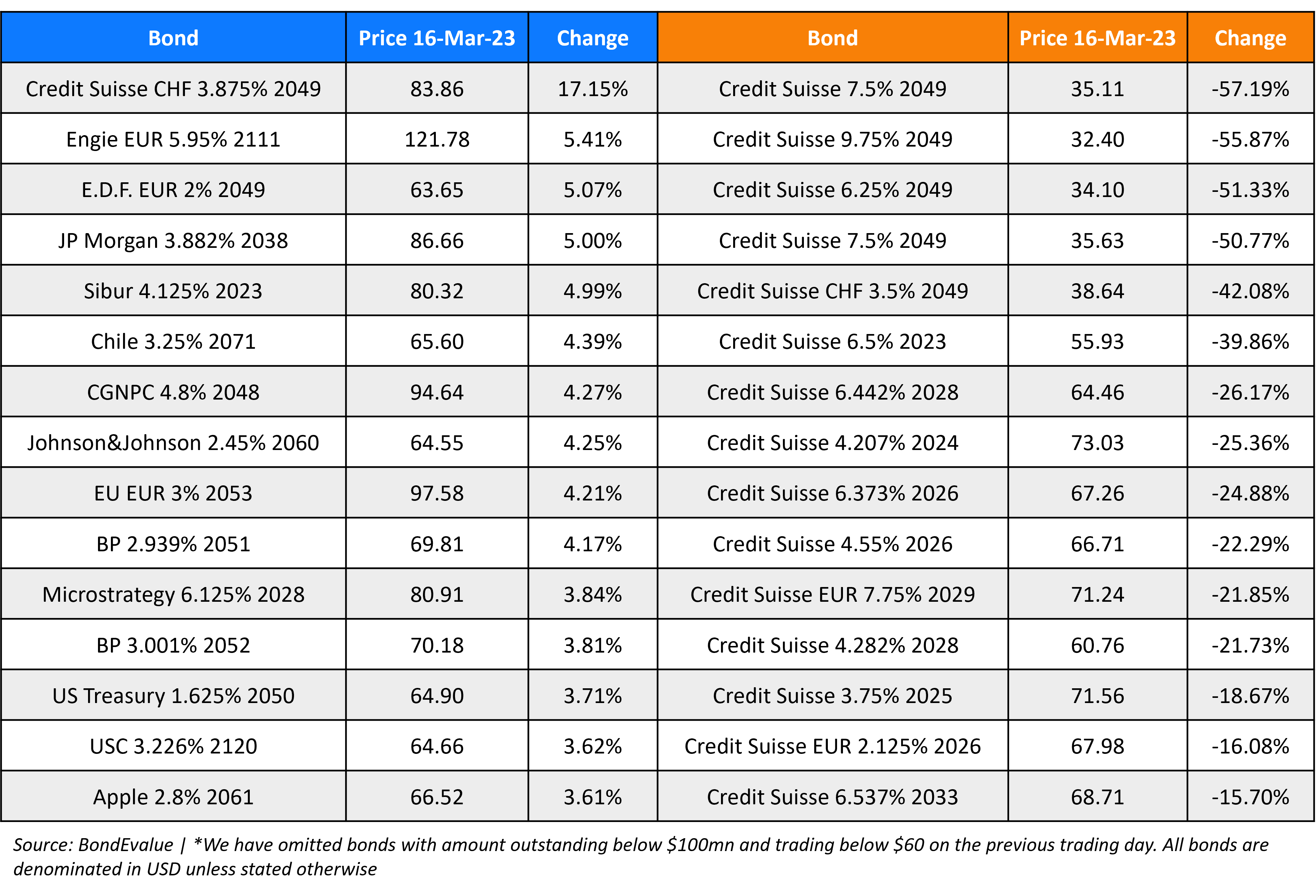

Top Gainers & Losers – 16-March-23*

Go back to Latest bond Market News

Related Posts:

NWD’s China Unit Planning $732mn Project in Guangzhou

August 26, 2021

SBI Reports 62% Quarterly Profit Jump

February 7, 2022

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.