This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

March 7, 2023

US Treasury yields were marginally higher across the mid-to-long end, while the 2Y was up 5bp on Monday. The peak Fed Funds rate was 3bp higher at 5.48% for the September 2023 meeting. Markets continue to price in three hikes of 25bp each at the next three FOMC meetings in March, May, June, based on the CME’s maximum probability calculations. The focus now shifts to Fed Chairman Jerome Powell’s Congressional Testimony hearing later today for clues on the path of interest rates. US IG and HY CDS spreads tightened by 0.3bp and 2.1bp respectively. The S&P and Nasdaq were near flat, with the former up 0.1% and the latter down 0.1%.

European equity markets ended mixed. European main CDS spreads tightened 2.5bp while crossover CDS spread tightened 11.4bp. Asian equity markets have opened in the green. Asia ex-Japan CDS spreads tightened by 0.6bp.

Dollar bonds of Turkey rallied by over 2% across the curve on reports that the opposition party could endorse popular Ankara and Istanbul mayors Mansur Yavas and Ekrem Imamoglu as vice presidents. This was considered a welcome move as it would break an impasse over a joint candidate in May’s election to oust Erdogan.

.png)

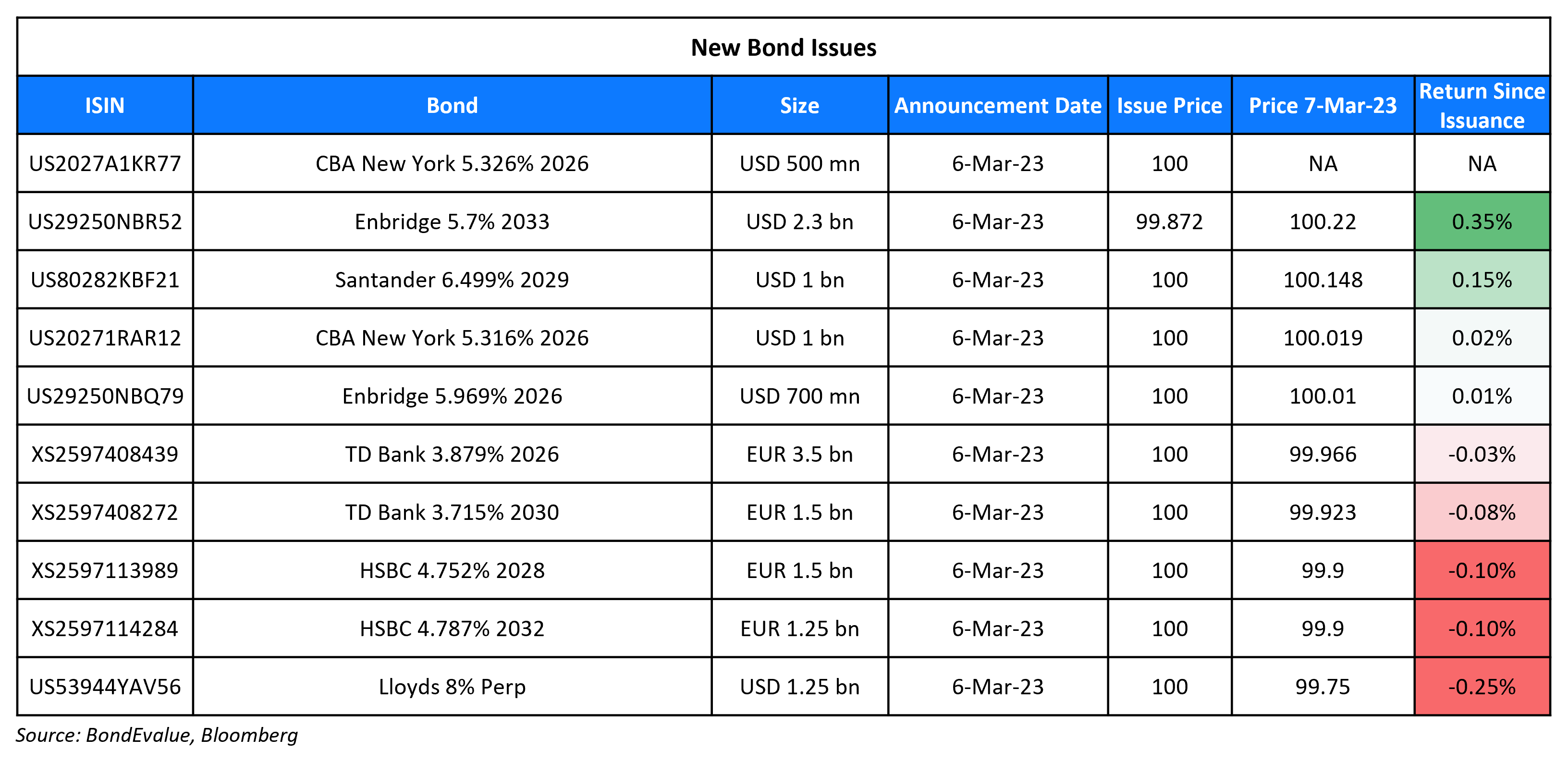

New Bond Issues

- HSBC S$ 10NC5 Tier 2 at 5.625% area

HSBC raised €2.75bn via a two-tranche deal. It raised

- €1.5bn via a 5NC4 bond at a yield of 4.752%, 25bp inside initial guidance of MS+145bp area. The senior unsecured bonds received orders over €3.1bn, 2.1x issue size. If not called by the coupon reset date (10 March 2027), the current fixed coupon of 4.752% will be reset to 3M Euribor+129bp quarterly.

- €1.25bn via a 9NC8 bond at a yield of 4.787%, 25bp inside initial guidance of MS+175bp area. The senior unsecured bonds received orders over €3bn, 2.4x issue size. If not called by the coupon reset date (10 March 2031), the current fixed coupon of 4.787% will be reset to 3M Euribor+155bp quarterly.

The new senior unsecured notes have expected ratings of A3/A-/A+. Proceeds will be used for general corporate purposes. With this deal, together with the issuer’s S$ 10NC5 Tier 2 offering announced this morning, HSBC will have issued a total of 8 notes across 3 currencies in a single week, with the total amount raised having already reached ~$13bn.

Lloyds Bank raised $1.25bn via a PerpNC7 AT1 bond at a yield of 8%, 37.5bp inside initial guidance of 8.375% area. The subordinated notes have expected ratings of Baa3/BB-/BBB-. Proceeds will be used for general corporate purposes, including the repurchase or refinancing of existing debt and/or capital securities. A capital adequacy trigger event will occur if the issuer’s CET1 ratio falls below 7%. If not called by the coupon reset date (27 March 2030), the current fixed coupon of 8% will be reset to 5Y Treasury+391.3bp every 5 years. The new bonds offer a yield pick-up of 119bp to PNC Financial’s BBB rated rated 6.25% Perps (callable in March 2030) that yield 6.81%.

Santander raised $1bn via a 6NC5 bond at a yield of 6.499%, 27bp inside initial guidance of T+250bp area. The senior unsecured bonds have expected ratings of Baa3/BBB+/BBB+. Proceeds will be used for general corporate purposes. The new bonds are priced at a new issue premium of 19.9bp to its existing 6.534% 2029s that yield 6.3%

New Bonds Pipeline

- Shinhan Bank hires for $ senior bond

- NatWest hires for 500 mn WNG 5NC4 Social bond

- AFDB hires for $ 5Y bond

- Bank of East Asia hires for $ 4NC3 bond

- REC hires for $ Long 5Y Green bond

- Qatar plans for $ bond

Rating Changes

- Fitch Upgrades Instituto Costarricense de Electricidad to ‘BB-‘; Outlook Stable

- Bed Bath & Beyond Inc. Upgraded To ‘CCC-‘ From ‘D’ Following Completed Interest Payment; Outlook Negative

- NagaCorp Ltd. Downgraded To ‘B’ From ‘B+’ On Refinancing Risk; Outlook Negative

- Fitch Revises Allwyn’s Outlook to Positive; Affirms Ratings

- Moody’s affirms CAR Inc.’s B3 ratings; revises outlook to negative

Term of the Day: Yankee Bonds

These are a type of Eurobond issued and traded in the US and are denominated in USD. In essence, if a foreign company (a non-US based company) issues a USD bond which is traded in the US, the bond is considered a Yankee Bond. This is in comparison to a Eurodollar bond that is issued by a foreign entity denominated in USD, but the bonds are issued and trade outside of the US.

Talking Heads

On Vedanta’s Agarwal Asking Government to Divest Entire Stake

“Government has agreed that they will sell 100% share 20 years back. So how much will you hold our leg and not allow us to run? They have to take a decision to disinvest this 29%. The company has to be run by the board and not by the government”

On Turkish Bonds Rallying as Opposition Nears Deal on Candidate

Piotr Matys, a senior analyst at ITCM

“At least some market participants may anticipate that if the opposition comes to power, market-friendly reforms would be implemented to address structural issues, including chronically high inflation”

Cristian Maggio, head of portfolio and ESG strategy at TD Securities

“I don’t think anyone in financial markets reasonably want to see Erdogan running the show for another five years”

On Europe Bond Sales Top Half-a-Trillion Mark in Record Time

David Zahn, head of European fixed income at Franklin Templeton

“If we are going to have another volatile year, it’s better to get it done early than wait. You don’t know what the rest of the year will be like

Matthew Bailey, ED of European credit strategy at JPMorgan Chase

“Some issuance has been front-loaded this year into a window of strong market conditions. But we think there is still plenty more supply to come”

On Pakistan required to give assurance on financing balance of payments gap – IMF

“All IMF programme reviews require firm and credible assurances that there is sufficient financing to ensure that the borrowing member’s balance of payments is fully financed… Pakistan is no exception”

On ECB’s Holzmann calling for four more 50bps rate hikes- Handelsblatt

“I expect it to take a very long time for inflation to come down. My hope is that within the next 12 months we will have reached the peak of interest rates”. The ECB should raise interest rates by 50 basis points at each of its next four meetings.

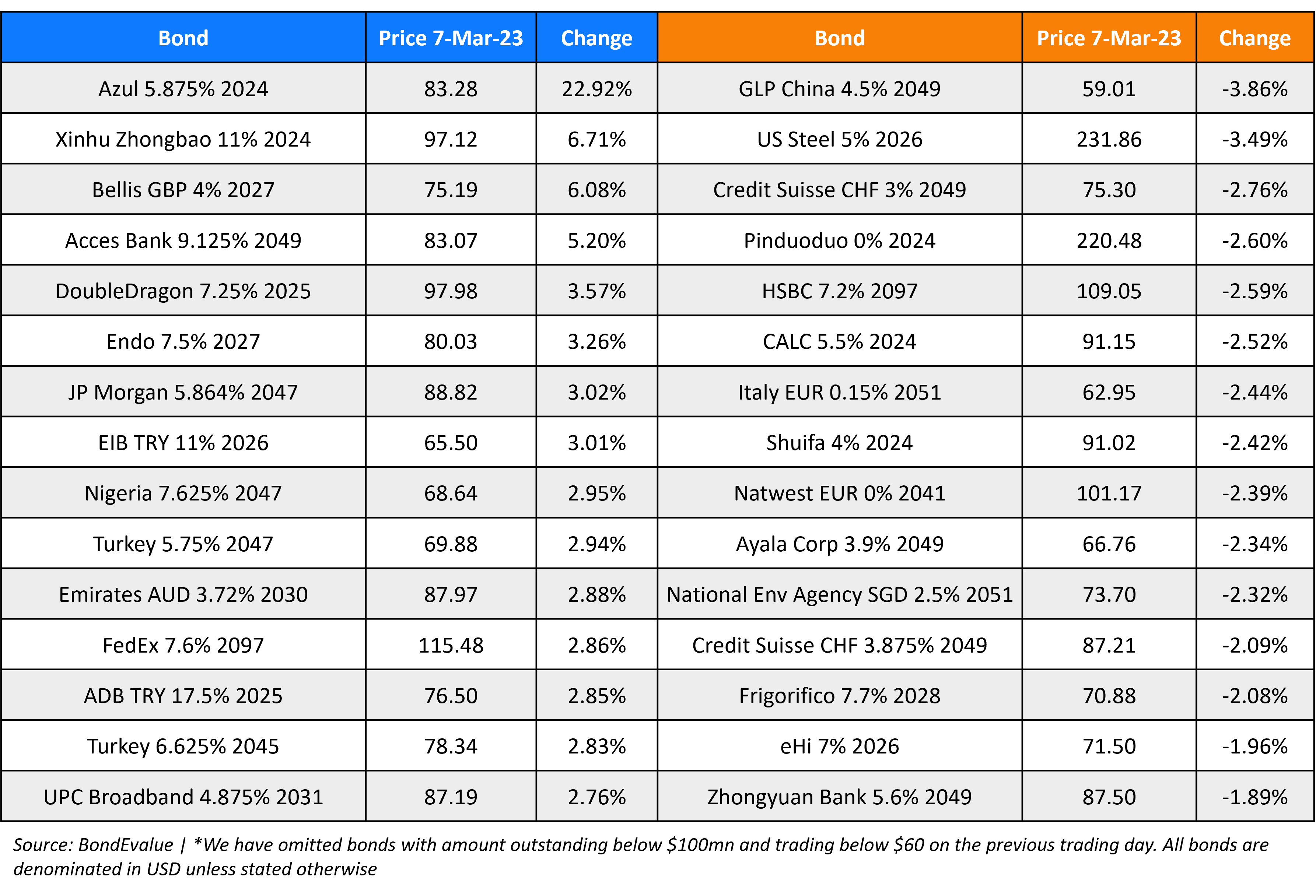

Top Gainers & Losers – 07-March-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.