This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

March 13, 2023

US Treasury curve shifted lower for a second straight day on Friday – the 2Y yield dropped a solid 43bp to 4.36% while the 10Y yield dropped 18bp to 3.67% (see chart in The Week That Was). The flight to safety move comes after the February NFP print and the collapse and subsequent bailout of Silicon Valley Bank (SVB).

US Non-Farm Payrolls came at 311k for February, higher than the surveyed 225k and lower than last month’s 517k print. Unemployment was at 3.6%, higher than the surveyed 3.4%. Average Hourly Earnings YoY was at 4.6%, lower than the surveyed 4.7%, but higher than last month’s 4.4% print. The repercussions of the SVB impact continued to wreak havoc across markets after the bank went into FDIC receivership and was shut down by regulators after a failed capital raise, marking the biggest failure of a US bank since the GFC. In the latest update, US regulators announced emergency measures on Sunday to instill confidence in the banking system. The Fed announced a new funding facility, the Bank Term Funding Program (BTFP), under which it will offer loans of up to 1Y to banks against collateral including US Treasuries, agency debt, MBS and other “qualifying assets”. The Fed said that the collateral will be valued at par and that the BTFP will “eliminate an institution’s need to quickly sell those securities in times of stress”. The regulators added that depositors of SVB and Signature Bank, which was closed by the New York authorities for similar reasons, will have access to their money on Monday.

This led the peak Fed Funds rate to drop by another 41bp to 5.04% for the June 2023 meeting. Looking at current futures-implied probabilities, markets are now pricing in a 96% probability of a 25bp hike on 22 March and 4% probability of no hike, vs. a 79% probability of a 50bp hike last Thursday. Credit markets are seeing spreads widen across the board – US IG and HY CDS spreads widened by 4.1bp and 19.7bp respectively. The S&P and Nasdaq dropped sharply again for a second day, down 1.5% and 1.8% respectively on Friday.

European equity markets too ended the week in the red. European main CDS spreads widened 5.8bp while Crossover widened by a massive 29.6bp. Asian equity markets have opened in the red today, taking cues from global equities. Asia ex-Japan CDS spreads widened by 7.2bp.

-1.png)

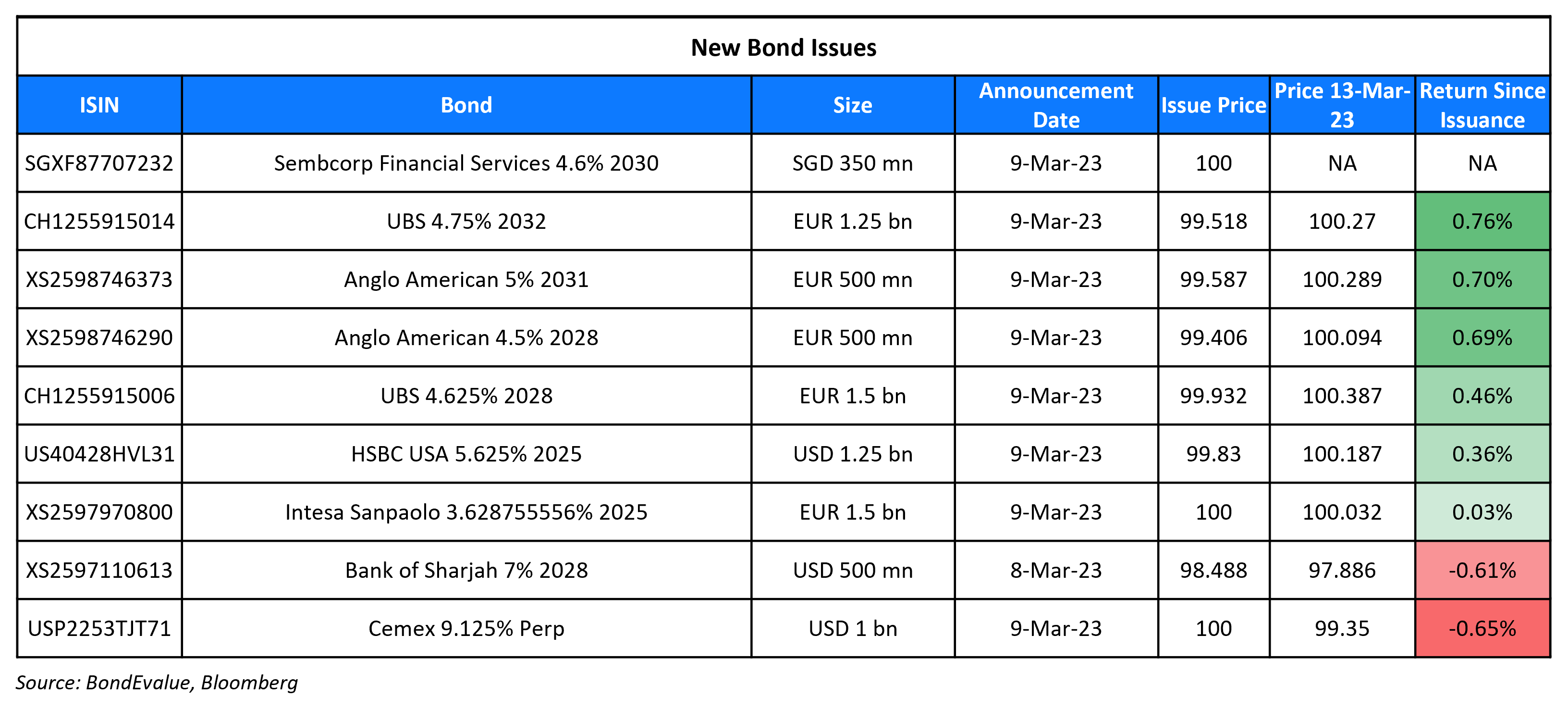

New Bond Issues

New Bonds Pipeline

- Shinhan Bank hires for $ senior bond

- REC hires for $ Long 5Y Green bond

- Qatar plans for $ bond

Rating Changes

- Moody’s upgrades Barclays PLC’s senior unsecured debt rating to Baa1 from Baa2; outlook stable

- Moody’s downgrades Vedanta Resources’ CFR to Caa1; outlook remains negative

- Moody’s affirms Yanlord’s Ba2/Ba3 ratings; changes outlook to negative

Term of the Day: Available-for-sale Securities

Available-for-sale (AFS) securities is the default classification for equity and debt assets that a company has on its balance sheet that it neither intends to actively trade, nor hold till maturity. From an accounting perspective, AFS need to be marked-to-market, requiring the company to recognize gains/losses based on the current price of the asset. These are different from held-to-maturity (HTM) securities in that HTM securities do not need to be marked-to-market – they are typically recorded at the original purchase cost.

HTM and AFS securities have come into focus since SVB’s collapse. With an increase in withdrawals from depositors, SVB reported to have sold $21bn worth of its AFS holdings and it recorded an after-tax loss of $1.8bn on the sale. Further, it held $91bn of HTM securities (primarily fixed income) as at 2022-end, on which it had unrealized losses of $15.9bn given the rise in interest rates over the past year. However, given the HTM classification, SVB was not required to recognize the losses on those securities. William C. Martin, who managed a Princeton-based hedge fund called Raging Capital for 15 years before closing it and starting a family office, said, “They had bought all these mortgages at the top of the market and were sitting on a massive unrealized loss.”

Talking Heads

On the move in Treasuries and change in rate expectations following the SVB collapse

Roberto Cobo Garcia, BBVA’s head of G10 FX strategy

“The market is clearly reading that the labor report is solid but not strong enough for the Fed to re-accelerate the hiking cycle. It would probably take very significant surprises in the CPI data next week for the Fed to change course again.”

Kevin Flanagan, head of fixed-income strategy at Wisdom Tree Investments

“It is incredible to see the whipsaw action in Treasury yields and it’s likely people want to own Treasuries into the weekend.”

Andrzej Skiba, portfolio manager at Bluebay Asset Management

“The reaction in the market reflects the broader worry about US banks and investors did expect a beat in the payrolls number”

On Fed under less pressure to speed rate hikes as wage gains cool

Evercore ISI’s Krishna Guha

“We would not get too relaxed about 50… We roll on to the inflation prints next week that could now be the decider, along with whether bank stress calms quickly or not”

Omair Sharif of Inflation Insights

“This report screams soft landing and looks to be a pretty good one for the Fed. In the current environment, this is basically what the Fed is hoping to see.”

Nationwide Chief Economist Kathy Bostjancic

“The Fed can take comfort in the rise in the supply of labor and the easing of upward pressure on wages to maintain a 25bp increase…. the February CPI report will also weigh heavily in the Fed’s deliberations of whether to raise rates 25bps or 50bps. Another rapid rise in consumer inflation could tip the scales towards 50bps”

On falling bond sales from emerging market issuers in 2023

Siby Thomas, a portfolio manager specializing in emerging-market corporate debt at T. Rowe Price

“The market isn’t open to most of our issuers. You’re seeing this bifurcation in the market where the companies that want to issue can’t because it’s too expensive, and the higher-rated ones that can issue don’t want to because they can afford to wait.”

Sara Grut, an analyst at Goldman Sachs Group Inc.

“Corporates tend to pro-actively manage their upcoming maturities a couple of years in advance, and took advantage of the low yields during 2020 and 2021. On some level, the current environment is just the flip side of that issuance.”

On flagging governance risks at Adani Group – MSCI ESG Research

“On March 3, we downgraded our assessment of the Hindenburg-related controversy cases to ‘moderate’ from ‘minor’ following new developments in the relevant cases… Across various Adani Group entities, MSCI ESG Research has identified issues relating to governance, board independence, related party transactions, and controlling shareholders”

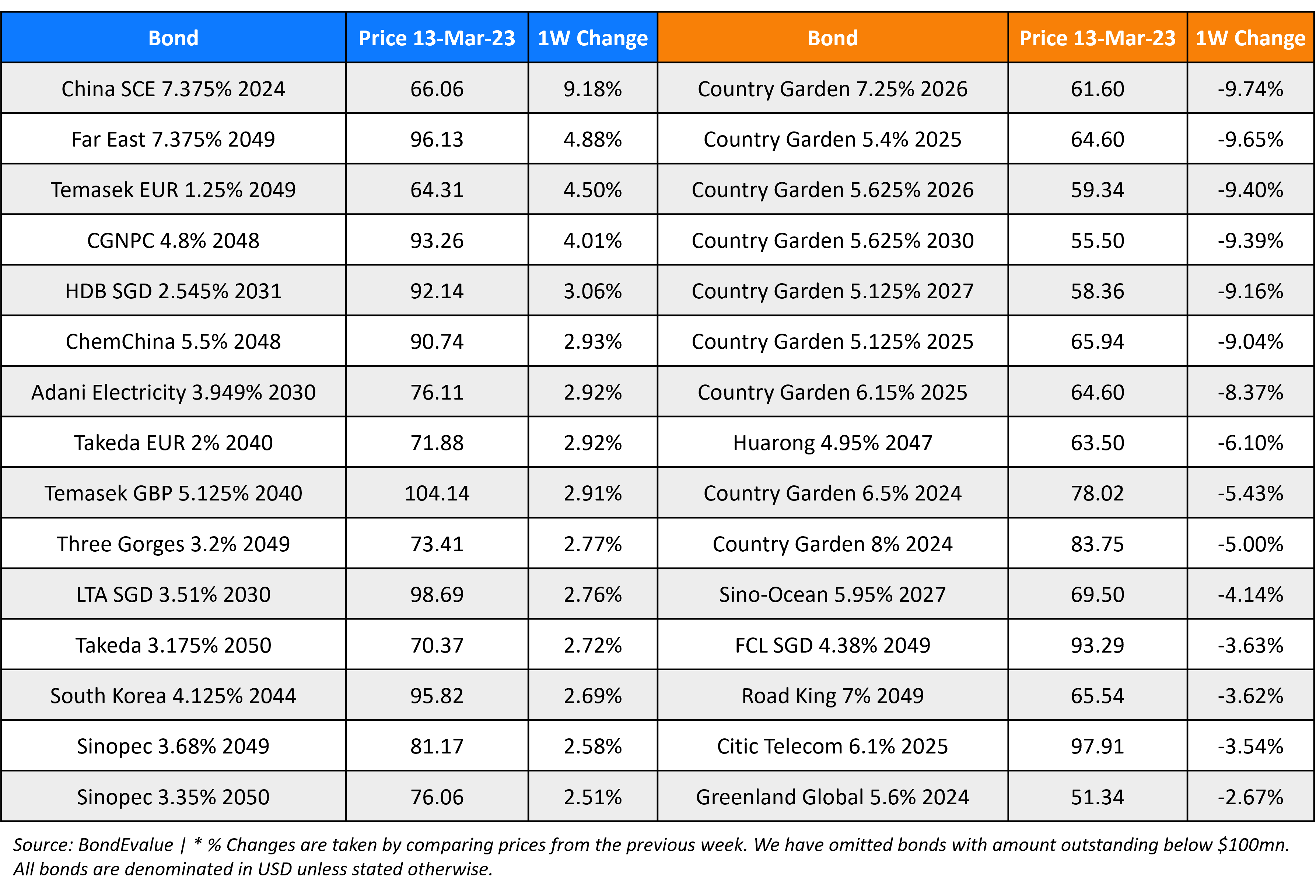

Top Gainers & Losers – 13-March-23*

Go back to Latest bond Market News

Related Posts:

NWD’s China Unit Planning $732mn Project in Guangzhou

August 26, 2021

SBI Reports 62% Quarterly Profit Jump

February 7, 2022

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.