This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

February 8, 2023

US Treasuries were near flat across the curve after Fed Chair Jerome Powell reiterated, “We think we are going to need to do further rate increases… The labor market is extraordinarily strong”. The peak Fed funds rate rose 2bp to 5.14% for the July 2023 meeting. Currently, the probability of a 25bp hike at the FOMC’s March meeting stands at 94%. The focus now shifts to the CPI inflation report on February 14. US IG CDS spreads tightened by 1.4bp while HY spreads were 2.5bp wider. Equity indices were higher with the S&P and Nasdaq up 1.3% and 1.9% respectively.

European equity markets also ended higher. The European main tightened widened 0.5bp while crossover CDS spreads tightened 10.1bp. Asian equity markets have opened broadly mixed today. Asia ex-Japan CDS spreads were 1.2bp tighter.

.png)

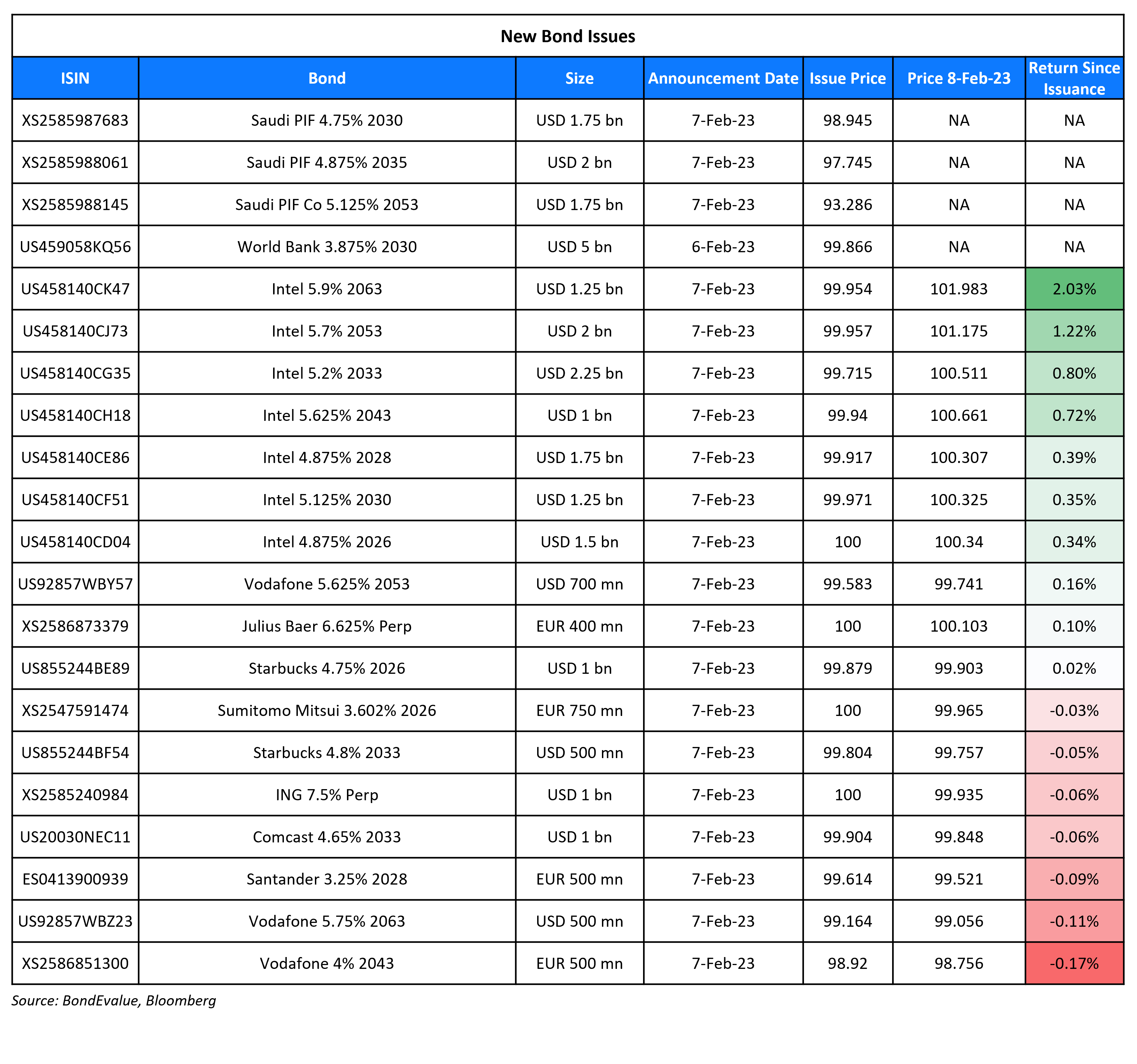

New Bond Issues

-

KDB $ 5Y/10Y at T+105/120bp area

Intel raised $11bn via a jumbo seven-part deal. Details are given in the table below:

The senior unsecured bonds have expected ratings of A2/A. Proceeds will be used for general corporate purposes, including refinancing of outstanding debt, funding for working capital, and capital expenditures.

ING Groep raised $1bn via a PerpNC5.75 AT1 bond at a yield of 7.504%, 49.6bp inside initial guidance of 8% area. The subordinated AT1 notes have expected ratings of Ba1/BBB, and received orders over $3.9bn, 3.9x issue size. Proceeds will be used for bail-in purposes. The initial coupon of 7.5% will be fixed until the first reset date on 16 November 2028. If not redeemed, coupons reset every five years at the 5Y US Treasury yield plus 371.1bp. The bonds are callable from 16 May 2028 to the first reset date and any interest payment date thereafter. A write-down trigger event may occur at any time if the issuer has determined that the Group CET1 Ratio is less than 7% The new bonds are priced 22.6bp tighter to its existing 4.875% Perps callable in November 2029 that yield 7.73%.

Santander raised €500mn via a 5Y covered bond (Term of the Day, explained below) at a yield of 3.335%, 7bp inside initial guidance of MS+45bp area. The bonds have expected ratings of Aa1, and received orders over €2.4bn, 4.8x issue size. The new bonds are priced 42.5bp tighter to its existing 3.875% 2028s that yield 3.76%.

Julius Baer raised €400mn via a PerpNC7 AT1 bond at a yield of 6.625%, 50bp inside initial guidance of 7.125% area. The junior subordinated AT1 notes have expected ratings of Baa3, and received orders over €4.45bn, 11.1x issue size. Proceeds will be used for general corporate purposes. The initial coupon of 6.625% will be fixed until the first reset date on 15 February 2030. If not called, the coupon will reset every five years at 5Y MS+384.7bp. The bonds are callable on 15 August 2028 and any interest payment date thereafter. A write-down trigger event may occur if the CET1 Ratio of the issuer is less than 5.125%.

Vodafone raised ~$1.7bn via a three-tranche deal. It raised

- €500mn via a 20Y bond at a yield of 4.08%, 40bp inside initial guidance of MS+175bp area.

- $700mn via a 30Y bond at a yield of 5.654%, 25bp inside initial guidance of T+220bp area.

- $500mn via a 40Y bond at a yield of 5.804%, 30bp inside initial guidance of T+240bp area.

The senior unsecured bonds have expected ratings of Baa2/BBB/BBB. Proceeds will be used for general corporate purposes.

Saudi Arabia’s Public Investment Fund raised $5.5bn via a three-tranche green deal. It raised

- $1.75bn via a 7Y bond at a yield of 4.752%, 30bp inside initial guidance of T+145bp area. The bonds received orders over $15.2bn, 8.7x issue size.

- $2bn via a 12Y bond at a yield of 4.876%, 30bp inside initial guidance of T+175bp area. The bonds received orders over $9.8bn, 4.9x issue size.

- $1.75bn via a 30Y bond at a yield of 5.126%, 30bp inside initial guidance of T+215bp area. The bonds received orders over $7.5bn, 4.3x issue size.

The senior unsecured green bonds will be issued by Gaci First Investment Co, and have expected ratings of A1/A. Proceeds will be used for general corporate purposes and to (re)finance and/or invest in Eligible Green Projects.

New Bonds Pipeline

- Khazanah Nasional Bhd hires for $ bond

- SMBC hires for € 3Y Covered bond

Rating Changes

Term of the Day

Covered Bonds

Covered bonds are senior secured debt instruments that are typically issued by banks. These bonds are secured (i.e. covered) by a pool of assets referred to as the “cover pool”, which typically consists of mortgages or loans. In an event that the bank defaults, holders of covered bonds have a preferential claim to the cover pool, which ensures interest payments and repayment of principal. This makes covered bonds relatively more secure vs. other debt and therefore results in a higher credit rating. While they have similarities with Mortgage-Backed Securities (MBS) in terms of the pool of assets there is a difference – the transfer of mortgages to an Special Purpose Entity (SPE) in a MBS issue means that the issuing bank no longer bears the risk of the loans and the mortgage pool is static. This is in contrast to Covered Bonds where, because the mortgage pool is constantly adjusted to maintain the pool size, the issuing bank bears the credit risk of the mortgages.

Talking Heads

On Distressed Funds Including Oaktree Scooping Up Adani Bonds

Sanford C. Bernstein analysts

“The dichotomy between equity markets and bond markets seems to re-emerge, with bond markets stabilizing, highlighting a reduced risk of default on debt. We would think debt market should ideally be a leading indicator here if debt is the concern.”

Adani Green CEO, Vneet S. Jaain

Have a “robust capital management program with leverage well aligned with the business model. In the last few days, this has been further reaffirmed by the ratings agencies, equity and credit research analysts and various banks, financial institutions, long term investors and other key stakeholders”

On Green Bonds Making Fewer and Fewer Promises to Investors – Academic Researchers

“The market has evolved away from, not towards, enforceability. Increasingly, investors receive detailed disclaimers making clear that issuers are not obliged to use proceeds in any particular way and that investors have no enforcement rights if the issuer does not use proceeds as expected… Even when the bond includes promissory language regarding the use of proceeds, the promise is effectively unenforceable”

On Ecuador Debt Sinks as Voters Spurn Lasso’s Constitution Changes

Barclays Capital economist

“The president has called for a dialog, but the initial response from the Correista opposition has been that any agreement would need to include calling an early election”

Citigroup Global

“The Lasso administration will face a harder political context following Sunday’s elections. Its governability, which was already weak, will likely deteriorate further.”

Santander US Capital Markets

“For bondholders, the political setback represents latent policy risk and still high repayment uncertainty of back-loaded bond payments. It’s difficult to commit to a high conviction view on the evolving risks over the next three years”

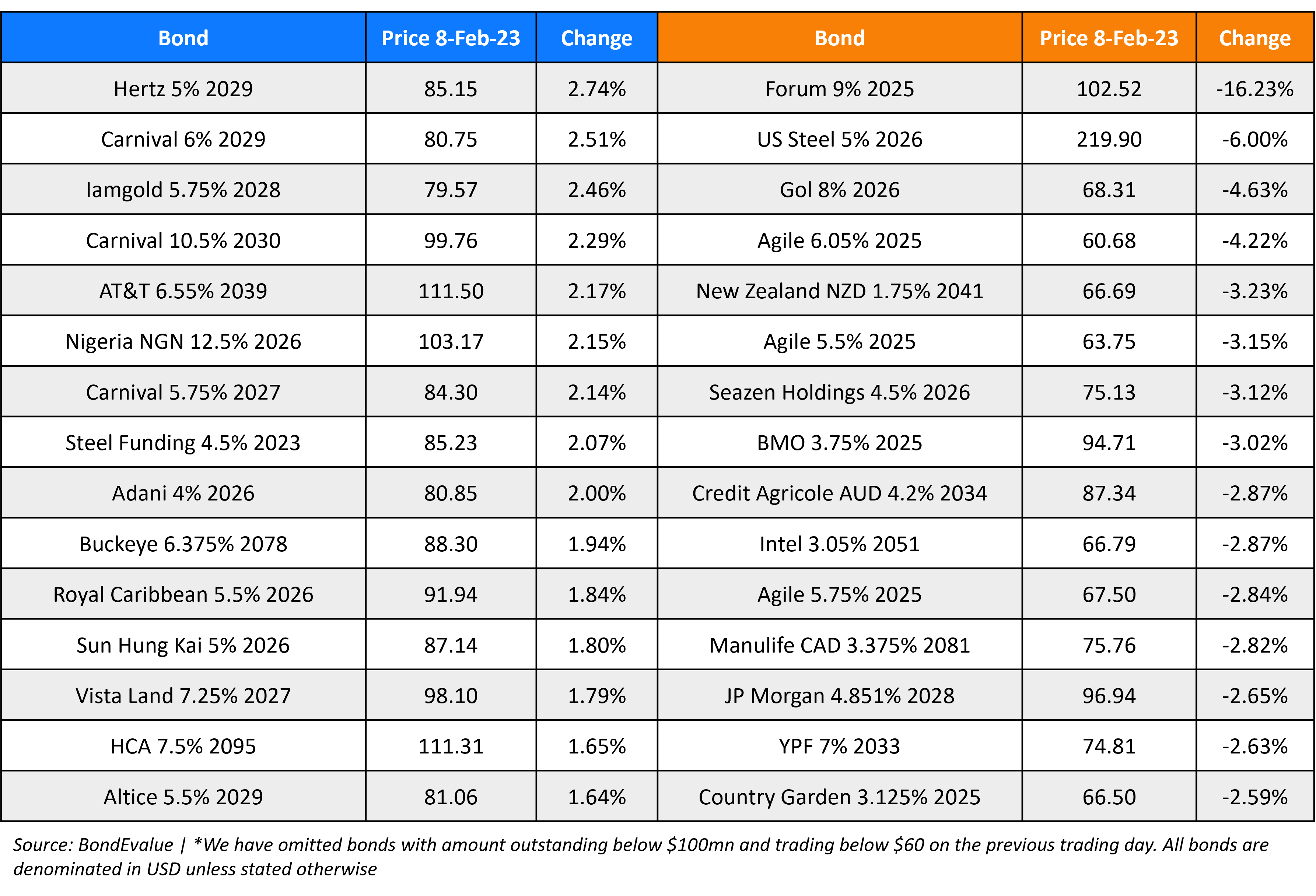

Top Gainers & Losers – 08-February-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.