This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

January 11, 2023

US Treasury yield inched up on Tuesday with the 2Y up 2bp and the 10Y up 6bp. The peak Fed funds rate was unchanged at 4.93% for the June 2023 meeting. The probability of a 25bp hike at the FOMC’s February 2023 meeting stands at 80% unchanged from yesterday. US equity markets ended higher with the S&P up 0.7% and Nasdaq up 1%. US IG and HY CDS spreads were 0.2bp and 0.8bp wider.

European equity markets ended lower. The European main and crossover CDS spreads widened by 2.4bp and 7.4bp respectively. The European primary markets are having a record start to the year with new deals of over $150bn priced so far. Asian equity markets have opened lower today. Asia ex-Japan CDS spreads tightened by 5.6bp.

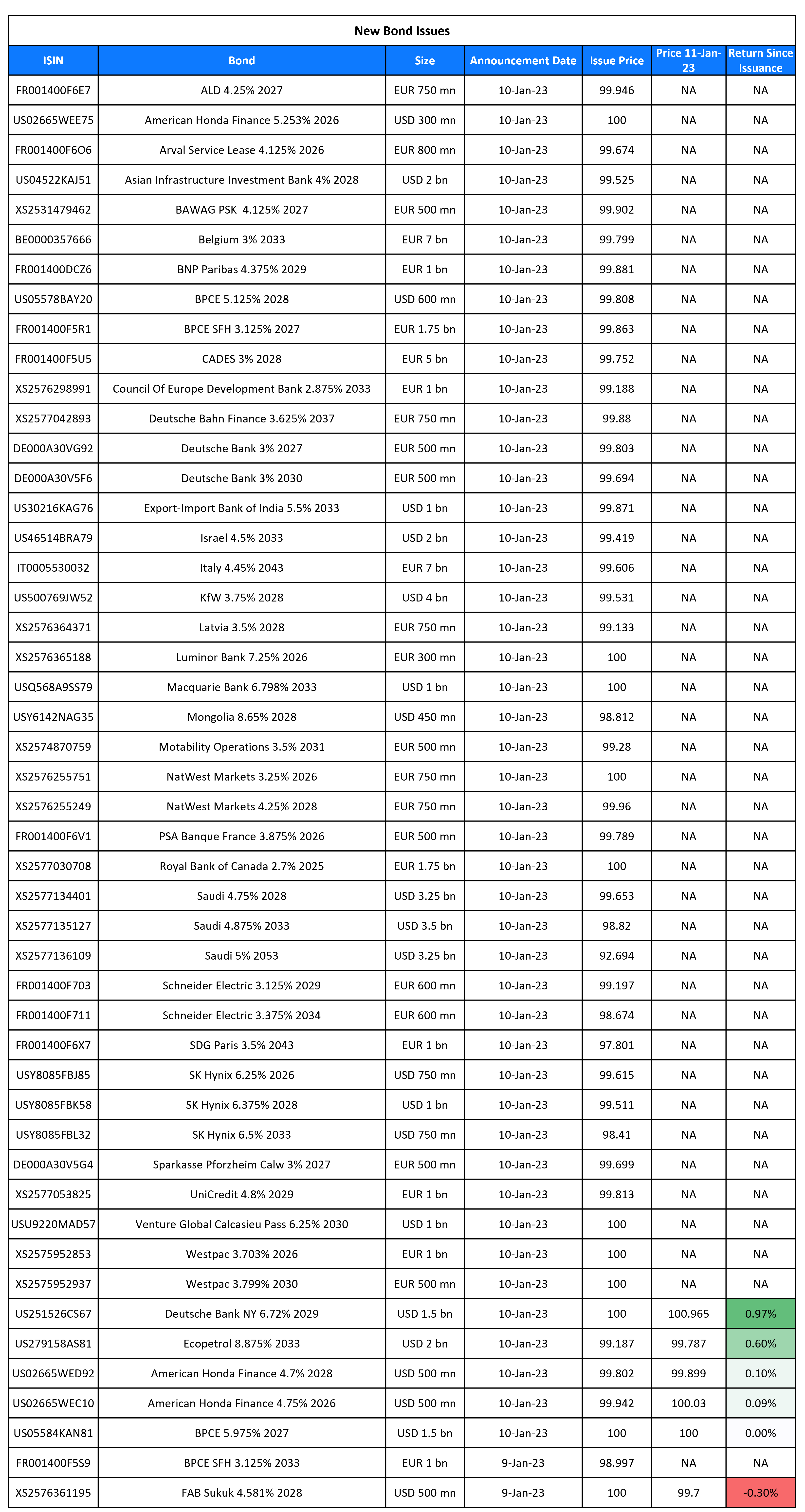

New Bond Issues

- ICBC HK $ 3Y Green @ T+110bp area

- ICBC Dubai $ 3Y FRN @ SOFR+140bp area

Exim Bank (India) raised $1bn via a 10Y sustainability bond at a yield of 5.517%, 30bp inside initial guidance of T+220bp area. The senior bonds received orders of over $3.7bn, 3.7x issue size. Proceeds will be used to finance or refinance projects that meet the issuer’s green or social project standards as outlined in its ESG framework. This was the first Indian issuer of dollar bonds since April 2022 when Greenko Wind Projects (Mauritius) raised $750mn.

Saudi Arabia raised $10bn via a three-trancher. It raised:

- $3.25bn via a 5Y bond at a yield of 4.829%, 30bp inside initial guidance of T+140 area. The new bonds were priced at a new issue premium of 16bp over its older 3.625% 2028s that yield 4.67%.

- $3.5bn via a 10.5Y bond at a yield of 5.021%, 30bp inside initial guidance of T+170bp area. The new bonds were priced at a new issue premium of 34bp over its older 2.25% 2033s that yield 4.68%

- $3.25bn via a 30Y bond at a yield of 5.5%, 30bp inside initial guidance of T+210bp area.

The bonds are rated A1/A (Moody’s/Fitch). Proceeds will be used for general domestic budgetary purposes.

Macquarie raised $1bn via a 10Y Tier 2 bond at a yield of 6.978%, 30bp inside initial guidance of T+350bp area. The bonds are rated Baa3/BBB/BBB+, and received orders of over $4.5bn, 4.5x issue size. Proceeds will be used for general corporate purposes.

Ecopetrol raised $2bn via a 10Y bond at a yield of 9%, 37.5bp inside the initial guidance of 9.375% area. The senior unsecured bonds have expected ratings of Baa3/BB+/BB+. Proceeds will be used for general corporate purposes and to prepay the remaining outstanding principal of the loan taken to fund the ISA acquisition. The new bonds are priced 65bp wider to its existing 4.625% 2031s that yield 8.35%.

Deutsche Bank raised ~$3.1bn equivalent via a multi-currency three-tranche deal. It raised:

- €500mn via a 4Y covered bond at a yield of 3.053%, 5bp inside the initial guidance of MS+10bp area.

- €500mn also via a covered 7.5Y bond at a yield of 3.048%, 4bp inside the initial guidance of MS+20bp area.

-

$1.5bn via a 6NC5 Fixed-to-FRN bond issued by its New York branch at a yield of 6.72%, 30bp inside the initial guidance of T+330bp area. The new bonds are priced 29bp wider to its existing non-callable 1.75% 2028s that yield 6.43%.

The covered EUR-denominated bonds have expected ratings of Aaa. The senior non-preferred USD-denominated bonds have expected ratings of Baa1/BBB-/BBB+. Proceeds will be used for general corporate purposes.

First Abu Dhabi Bank raised $500mn via a 5Y bond at a yield of 4.581%, 12bp inside the upper bound of initial guidance of T+100bp. The senior unsecured sukuks will be settled on 17 January 2023.

SK Hynix raised $2.5bn via a three-trancher. It raised:

- $750mn via a 3Y bond at a yield of 6.393%, 40bp inside initial guidance of T+280bp area

- $1bn via a 5Y SLB at a yield of 6.491%, 40bp inside initial guidance of T+315bp area

- $750mn via a 10Y green bond at a yield of 6.721%, 50bp inside initial guidance of T+360bp area

The bonds are rated rated Baa2/BBB- (Moody’s/S&P). Proceeds from the 3Y and 5Y notes will be used for general corporate purposes, while that from the 10Y green bond will be used to finance eligible projects in accordance with their green financing framework. If the company fails to reduce Scope 1 and Scope 2 GHG intensity by at least 57% by 2026 from a 2020 baseline, there will be a 75bp coupon step-up.

Mongolia raised $450mn via a 5Y bond at a yield of 8.95%, a strong 67.5bp inside initial guidance of 9.625% area. Proceeds from the new bonds will be used to repurchase all of its 5.625% 2023s, with the remaining proceeds to redeem its 8.75% 2024s, for which it has launched an exchange offer and tender offer. It is offering to exchange the 2023s and 2024s on a par-to-par basis including accrued interest. After considering the exchange ratio, the exchange price will amount to $1,012.023 in aggregate principal of the new notes for the two bonds plus interest, as per IFR. Bondholders can also choose to tender their bonds to be paid in cash, with the offer expiring on January 13. The new bonds were priced at a new issue premium of 47bp over its older 3.5% bonds due 2027 that yield 8.48%.

New Bonds Pipeline

- Woori Bank hires for $ 3Y Sustainability or 5Y Sustainability bond

Rating Changes

Term of the Day

Dim Sum Bonds

These are bonds denominated in offshore Renminbi (CNH) and issued outside China (mostly in Hong Kong). The first dim sum bond was issued in 2007 by China Development Bank – a 2Y offshore RMB bond in Hong Kong, with a 3% coupon and size of RMB 5bn ($750mn). These instruments get their name from dim sum, a popular delicacy in Hong Kong. Dim sum bonds are typically issued by issuers that have a need for Renminbi but do not want to go through regulatory approvals as dim sum issuance are not subject to regulatory approval from mainland China or Hong Kong, provided that they are sold to professional investors.

China Minsheng Banking (Hong Kong branch) priced a RMB 2bn ($295mn) 2Y green dim sum bond at a yield of 3.15%.

Talking Heads

Fed Chair Jerome Powell on the Fed’s independence, inflation, rates and climate change

“Restoring price stability when inflation is high can require measures that are not popular in the short term as we raise interest rates to slow the economy. The absence of direct political control over our decisions allows us to take these necessary measures without considering short-term political factors”…But “we should ‘stick to our knitting’ and not wander off to pursue perceived social benefits that are not tightly linked to our statutory goals and authorities…Taking on new goals, however worthy, without a clear statutory mandate would undermine the case for our independence.”

“Without explicit congressional legislation, it would be inappropriate for us to use our monetary policy or supervisory tools to promote a greener economy or to achieve other climate-based goals…Decisions about policies to directly address climate change should be made by the elected branches of government and thus reflect the public’s will as expressed through elections”

Goldman Sachs on Eurozone recession expectations

“We maintain our view that Euro area growth will be weak over the winter months given the energy crisis but no longer look for a technical recession…Euro zone inflation is expected to be around 3.25% at the end of 2023 compared with 4.50% forecast earlier. Core inflation for the region is also seen slowing to 3.3% by the year-end as goods prices cool, but continued upward pressure is expected on services inflation due to rising labour costs.”

Given the “sticky” nature of inflation, Goldman expects the European Central Bank to remain hawkish and deliver 50 basis points hikes in February and March before slowing to 25 bps for a terminal rate of 3.25% in May.

On new bond issues from Europe hitting over $150bn so far this year

Marco Baldini, global co-head of investment grade syndicate at Barclays Bank Plc.

“Issuers are taking this opportunity to get some funding done given there are still a lot of uncertainties out there…Right now, investors have cash and are positively disposed towards primary market investing.”

Atul Sodhi, Credit Agricole CIB’s global head of debt capital markets

“Liquidity is still strong and there are good reasons to be optimistic”…Yet he cautions that “we are not completely out of the woods yet.”

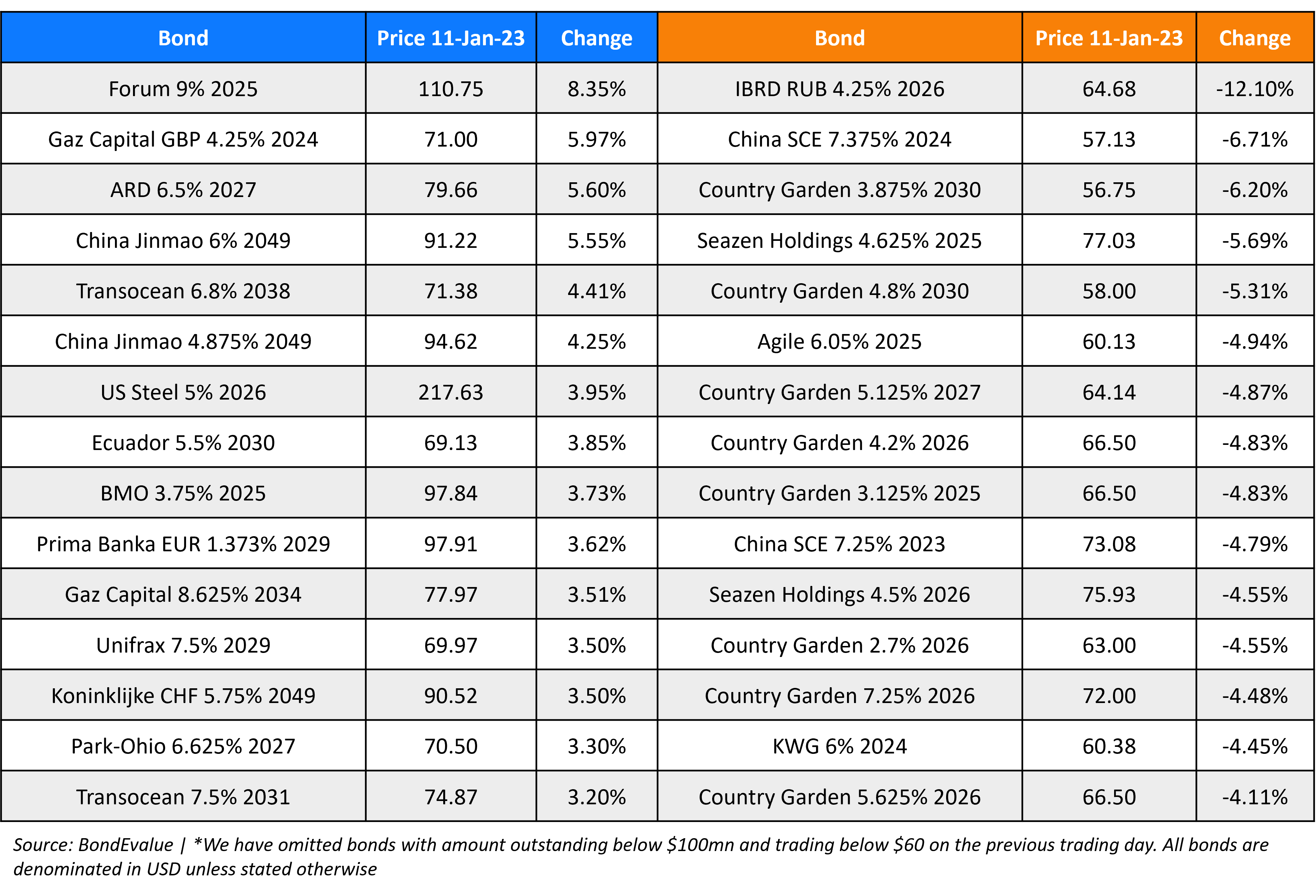

Top Gainers & Losers – 11-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.