This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

January 20, 2023

US Treasuries sold-off by 3-6bp across the curve after having eased sharply the day before. The peak Fed funds rate moved 5bp higher to 4.90% for the June 2023 meeting. The probability of a 25bp hike at the FOMC’s February 2023 meeting stands at 94%, almost unchanged. US equity markets ended lower with the S&P and Nasdaq down 0.8% and 1%. US IG CDS spreads widened 2.5bp and HY spreads were 13.7bp wider. Moody’s expects junk bond defaults to jump to 5.1% in 2023 vs. 2.8% in 2022 reflecting their “assumption of a worsening economic path”.

European equity markets ended lower by 1.9%. The European main and crossover CDS (Term of the Day, explained below) spreads widened by 3.7bp and 17.3bp respectively. Asian equity markets have opened mixed today. Asia ex-Japan CDS spreads tightened by 0.5bp.

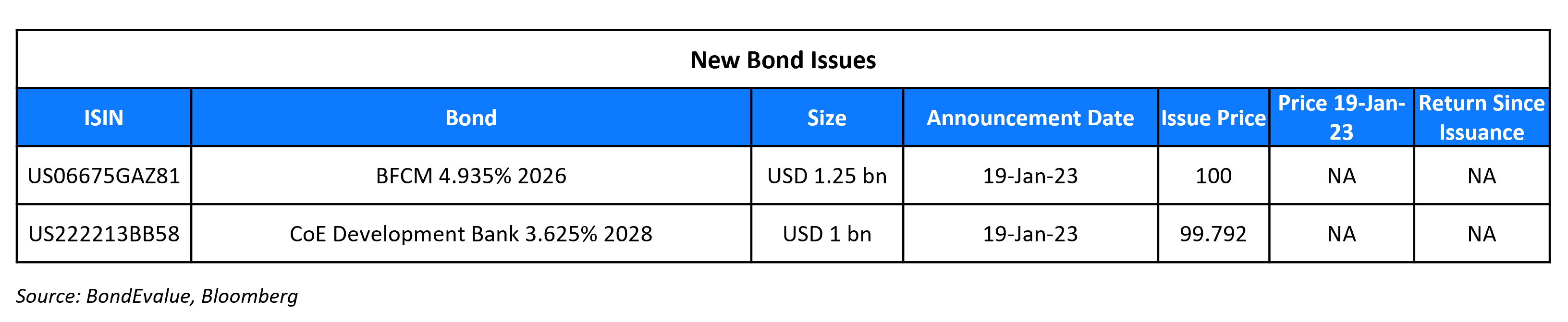

New Bond Issues

EDF raised ~€3bn via a four-tranche deal. It raised:

- €1bn via a 9Y bond at a yield of 4.26%, 30bp inside initial guidance of MS+195bp area

- €1bn via a 20Y bond at a yield of 4.729%, 20bp inside initial guidance of MS+250bp area

- £450mn via a 12Y bond at a yield of 5.686%, 15bp inside initial guidance of UKT+225bp area

- £500mn via a 30Y bond at a yield of 5.829%, 15bp inside initial guidance of UKT+230bp area

The senior unsecured bonds have expected ratings of Baa1/BBB/BBB+. Proceeds will be used for general corporate purposes.

BFCM raised $1.25bn via a 3Y bond at a yield of 4.935%, 22bp inside initial guidance of T+140bp area. The senior preferred bonds have expected ratings of Aa3/A+/AA-. Proceeds will be used for general corporate purposes.

New Bonds Pipeline

- Khazanah Nasional Bhd hires for $ bond

Rating Changes

- Fitch Downgrades Americanas’ IDRs to ‘D’

- Moody’s changes VNET Group, Inc.’s outlook to negative; affirms B2 corporate family rating

Term of the Day

Crossover CDS Index

The iTraxx Crossover Index is a credit default swap (CDS) based index compiled by IHS Markit (now part of S&P Global) which consists of the 75 most liquid sub-investment grade entities in Europe. The index helps track credit risk in the European high yield market, akin to the Markit HY CDS Index in the US. Performance is tracked in terms of the index’s value and the move in the spreads of the index. A tightening (a move lower) in its CDS spreads implies an easing of credit conditions in the European junk-bond markets which leads to an increase in the value of the index. On the other hand, a widening in its spread (a move higher) implies a worsening in credit conditions, which would lead to a fall in the index’s value. While the iTraxx Crossover Index helps track European high yield spreads, the iTraxx Main index helps track European investment grade spreads. The iTraxx Main index consists of 125 of the most liquid European entities with IG-ratings as published by Markit from time to time.

Talking Heads

On Fed needing more rate rises to cool inflation – Fed’s Williams

“With inflation still high and indications of continued supply-demand imbalances, it is clear that monetary policy still has more work to do to bring inflation down to our 2% goal on a sustained basis… restoring price stability is essential to achieving maximum employment and stable prices over the longer term”

On Argentina’s $1bn Bond Buyback Baffling Investors

Pablo Waldman, a senior strategist at Inviu

“There are very limited resources, and this is a very risky way of deploying them. If they don’t follow through with other measures, the very limited scope of this plan likely won’t cause bonds to rally further.”

Alejo Costa, chief Argentina strategist at BTG Pactual

“The government may think they’re improving market sentiment,” Costa said. “All Massa knows is politics and rhetoric, and he may believe this rhetoric improves the context ahead of the elections this year”

On UBS Bracing for Hard Landing in US Credit, Favoring European Debt

“We acknowledge US high yield is better positioned — mainly on the shift in credit quality. However, we still believe credit is heading for a hard landing… Overall we think refinancing capacity remains constrained with leveraged loan 2024-2025 maturities on the horizon”

On Global Property Market Facing $175 Billion Debt Spiral

Ian Guthrie, a senior MD at at Jones Lang LaSalle

“What we have in this downturn is a fairly unique set of economic circumstances. Interest rates are tightening instead of softening the blow for real estate and other corporates. You have a pipeline of potentially defaulting loans”

Nicole Lux, real estate credit at Bayes Business School

“We expect to see some casualties” among UK developers. There will be fire sales”

“The run-up in bond prices has legs in our view, particularly when it comes to the investment-grade markets. Corporate fundamentals continue to be broadly solid… the sharp U-turn we’re seeing in Chinese policies will provide a much-needed boost to global growth”

Giulio Baratta, BNP Paribas head of IG debt capital markets EMEA

“This is a very good window. Investors are anticipating that inflation is calming down and seeing this as a good entry point into the market”

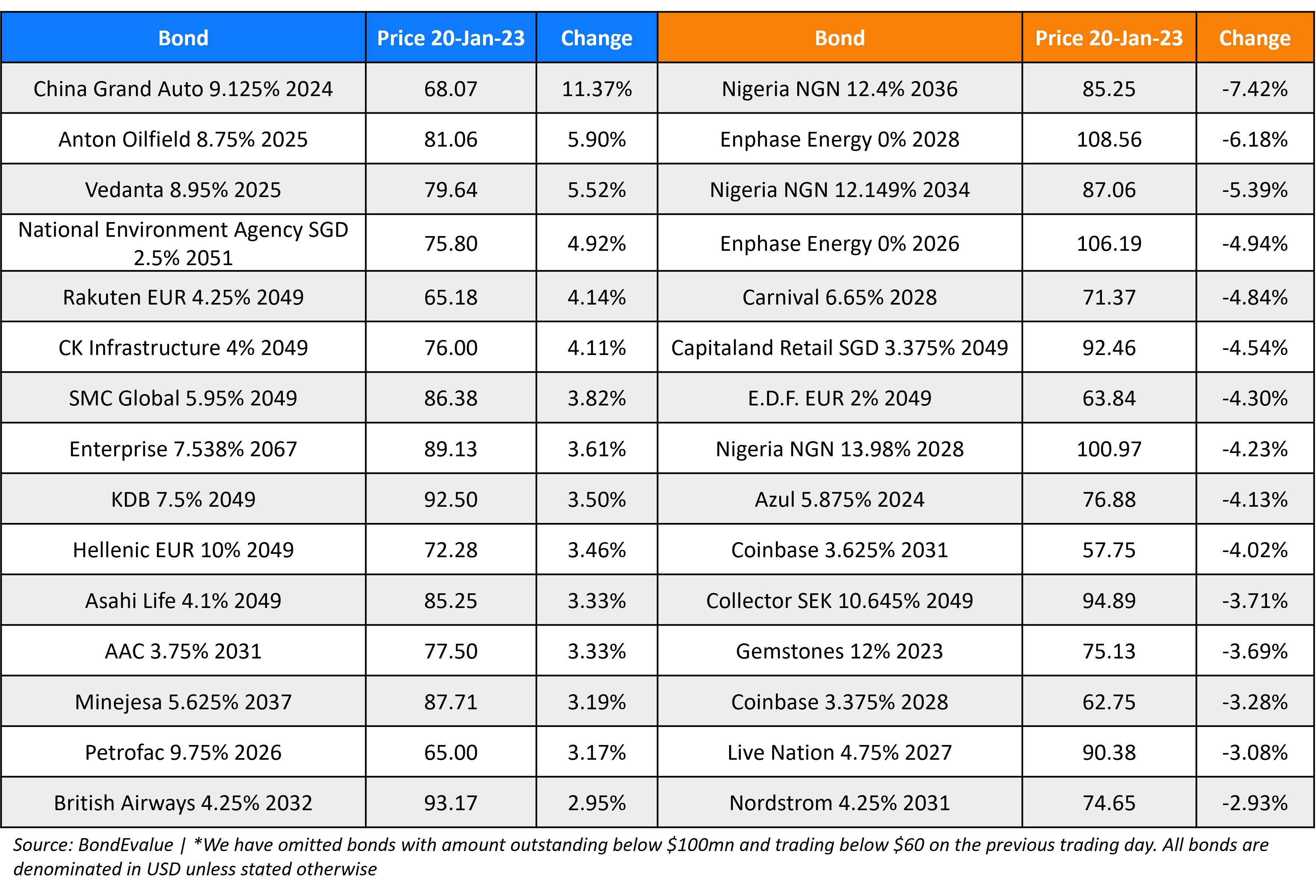

Top Gainers & Losers – 20-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.