This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

March 31, 2023

US Treasury yields were largely flat yesterday across the curve and the peak fed funds rate moved 3bp higher to 4.96% for the May meeting. CME maximum probabilities are now slightly skewed towards a 52% probability of a 25bp rate hike in May vs. a 40% chance a day earlier. The probabilities are almost evenly poised for either a status quo or a 25bp rate cut in the subsequent meetings thus offering no clarity of the path of policy interest rates. US IG and HY CDS spreads tightened 1.7bp and 9.2bp respectively as the broad risk-off sentiment eased. The S&P and Nasdaq ended higher on Thursday, up by over 0.6% and 0.7% respectively.

European equity markets ended higher too. European main CDS spreads tightened by 1.9bp and Crossover spreads were 8.6bp tighter. Egypt’s central bank hiked policy rates by 200bp to 18.25% on the back of increasing inflation. Egypt’s inflation print in February came at 32.9%, up from 26.5% in January. Asia ex-Japan CDS spreads tightened by 5.8bp. Mexico’s central bank hiked policy rates by 25bp to 11.25% on expected lines and removed reference in its statement regarding the possibility of future upward adjustments to the key rate.

Asian equity markets have also opened in the green this morning following cues from global bourses.

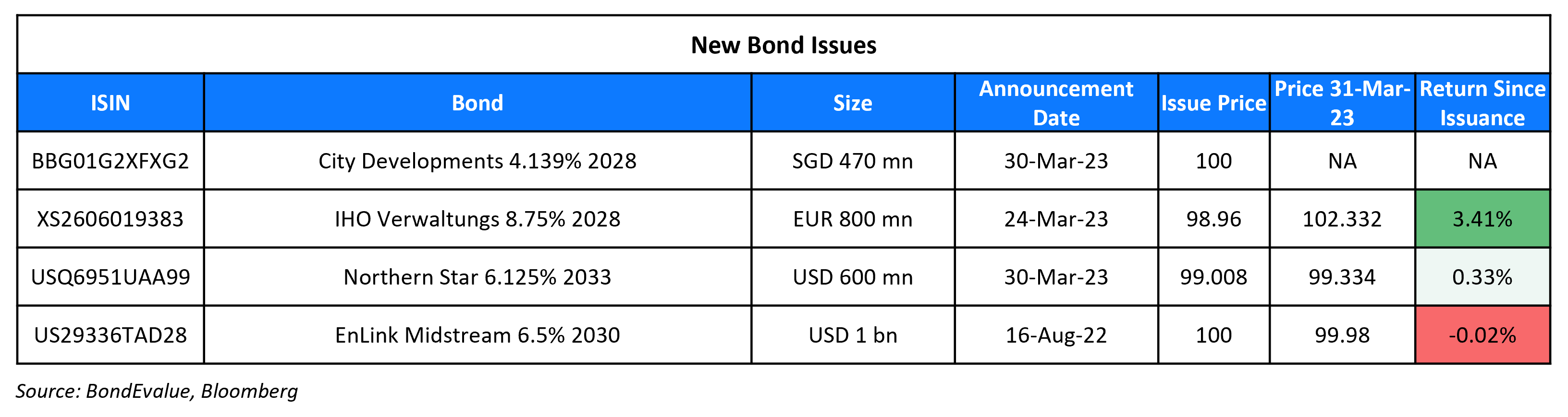

New Bond Issues

City Developments Ltd (CDL) raised S$470mn via a 5Y bond at a yield of 4.139%, a spread of SORA+120bp, unchanged from final guidance. Proceeds from the senior unsecured notes will be used to finance general working capital requirements and corporate funding of the issuer and its subsidiaries, and/or to refinance existing borrowings. CDL last tapped the SGD market in 2021 with a S$235m issuance of 2.3% 2026s.

Northern Star Resources raised $600mn in its debut 10Y dollar bond at a yield of 6.26%, 30bp inside initial guidance of T+300bp area. The senior unsecured bonds have expected ratings of Baa3/BBB–/BBB–. Proceeds will be used for general corporate purposes and capital expenditures. The bonds are issued by Northern Star Resources Ltd and guaranteed by its subsidiaries. CreditSights analysts had estimated the fair value at 265bp by referencing AngloGold Ashanti’s 3.75% 2030s and Gold Fields’ 6.125% 2029s, which currently yield 5.98% and 5.98% respectively.

New Bonds Pipeline

- Cyprus hires for first ever sustainable bond

- REC hires for $ Long 5Y Green bond

- Shinhan Bank hires for $ senior bond

Rating Changes

- Grupo Idesa S.A. de C.V. Downgraded To ‘CC’ From ‘CCC-‘ On Proposed Distressed Debt Exchange, Outlook Negative

- Moody’s revises Meituan’s outlook to stable, affirms Baa3 ratings

Term of the Day

Restricted Group/Subsidiaries

Restricted Group or restricted subsidiaries refer to a parent or holding company’s subsidiaries that are tied to the debt covenants of the parent issuer. Restricted groups may have covenants that restrict cash upstreaming to shareholders, additional indebtedness, liens, dividend payments, making new investments etc. Unrestricted subsidiaries on the other hand are not bound by the parent or holdco’s bond covenants and are thus not required to support repayment of the debt securities.

Take the case of a parent company that has various subsidiaries, and that the debt is issued at the parent’s or holdco’s level. Here, a restricted subsidiary’s assets are ringfenced such that during normal operations, the parent company is not able to use the cash of these units via transactions like inter-company loans etc. simply because it is a holding company. Therefore, in the event of distress, given that restricted subsidiaries are bound by restrictive debt covenants, bondholders’ credit risk is reduced as they have access to assets of the restricted subsidiary.

Talking Heads

On Banking Chaos Creates ‘Once-in-a-Decade’ Bond Buying Opportunity

Samuel Wilson, portfolio manager at Voya

“If you are willing to buy into the fear, there is definitely an opportunity. There is still room for spreads to heal”

Jesse Rosenthal and Peter Simon, strategists at research firm CreditSights

“It’s not a stretch to describe the current market as a once-in-a-decade buying opportunity for bank paper, especially the high-quality regional and custody banks that have blown out amid the panic”

Anastasia Amoroso, chief investment strategist at iCapital

“Some sense of stability has been returning to the banking sector… I would be careful with AT1. We can’t rule out any more bank failures — and you probably don’t want to be in the highest risk tier of preferred”

On Janet Yellen saying bank deregulation may have gone too far

“These events remind us of the urgent need to complete unfinished business: to finalise post-crisis reforms, consider whether deregulation may have gone too far and repair the cracks in the regulatory perimeter that the recent shocks have revealed”

On Fed Officials Seeing More Work on Inflation Despite Bank Strains

Boston Fed President Susan Collins

“Inflation remains too high, and recent indicators reinforce my view that there is more work to do, to bring inflation down to the 2% target associated with price stability”

Richmond Fed President Thomas Barkin

“It is possible that tightening credit conditions, along with the lagged effect of our rate moves, will bring inflation down relatively quickly”

On post-extraordinary rally, bonds’ now depend on bank stability and inflation

Mike Riddell, senior fixed income portfolio manager at Allianz Global

“That is not a normal move. You’re seeing 100 bps (yield) swings, one way and then the other in the space of six weeks…which is the kind of volatility that you normally only ever see in the middle of a massive crisis”

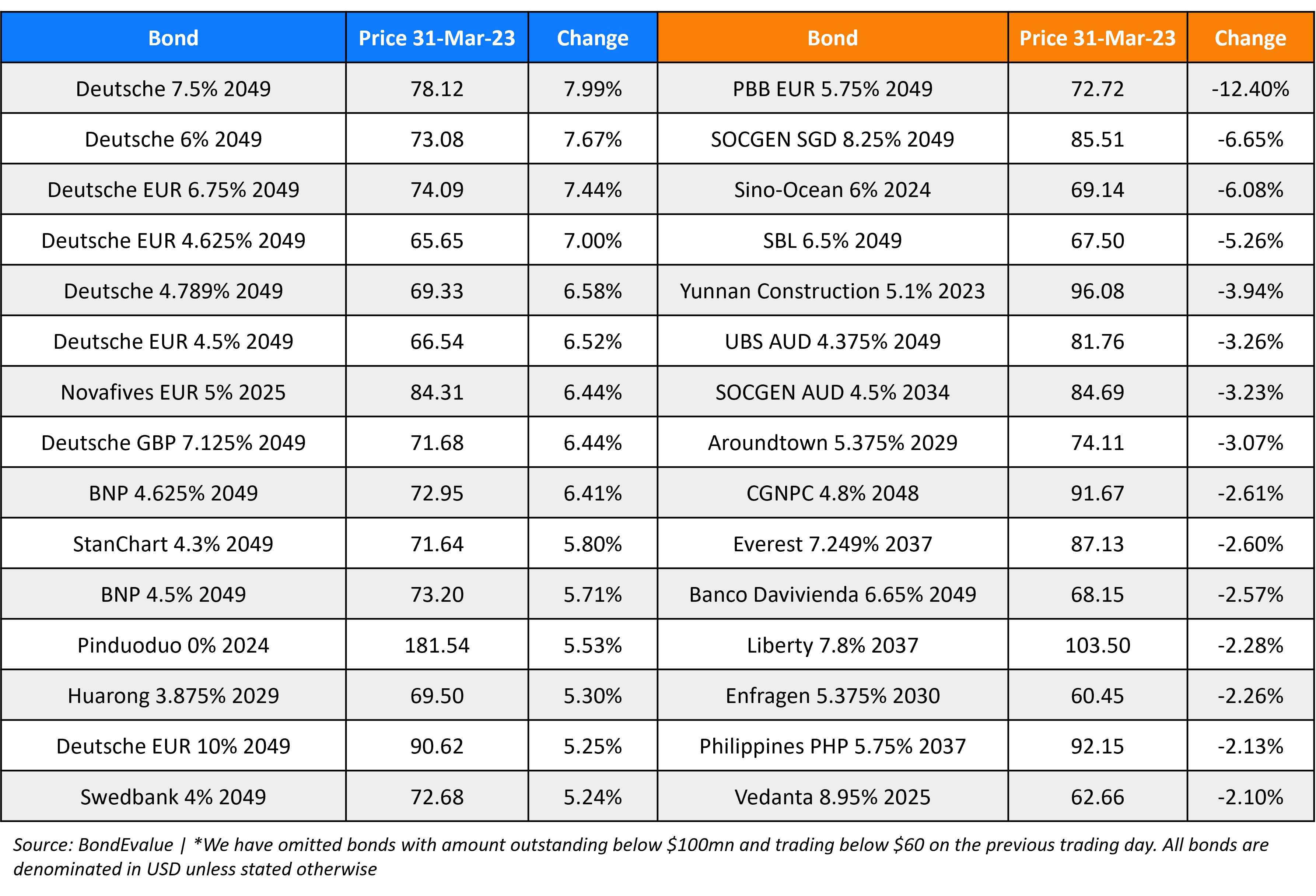

Top Gainers & Losers – 31-March-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.