This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues, Talking Heads; Top Gainers and Losers

April 19, 2023

US Treasury yields were stable across the curve and the peak Fed funds rate was 1bp lower to 5.10% for the June meeting. The probability of a 25bp hike at the May meeting reduced slightly from 87% to 82%. US IG and HY CDS spreads widened 0.1bp and 3.3bp respectively. US equity indices were little changed – the S&P and Nasdaq broadly ended the day almost flat. BofA reported its fund manager survey results that showed investors are the most bearish on stocks vs bonds since 2009. Investors indicated that credit crunch fears had driven up bond allocation to a net 10% overweight, the highest since March 2009.

European equity markets ended mixed. European main CDS spreads tightened 1.1bp and Crossover spreads were tighter by 4.1bp. Asia ex-Japan CDS spreads widened by 0.9bp. Asian equity markets have opened slightly lower this morning.

.png)

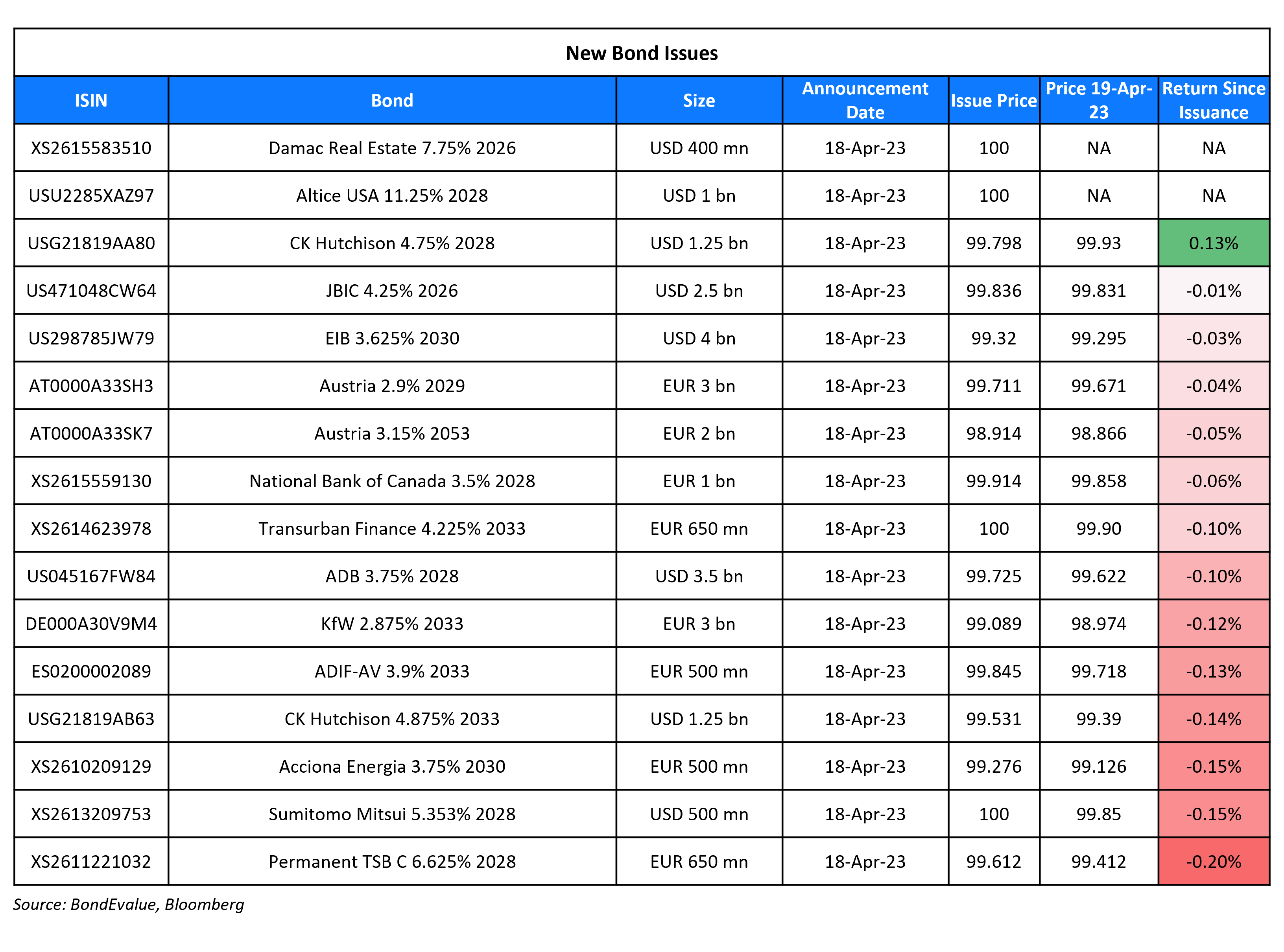

New Bond Issues

- Renew Power $400mn 3.25NC2.25 Green at 8.5% area

CK Hutchison raised $2.5bn in a 2-tranche deal. It raised:

- $1.25bn via a 5Y bond at a yield of 4.796%, 35bp inside initial guidance of T+145bp area. The new bonds are priced 7.6bp wider to its existing 2.75% 2029s that yield 4.72%.

- $1.25bn via a 10Y bond at a yield of 4.935%, 35bp inside initial guidance of T+170bp area.

The bonds have expected ratings of A2/A/A-. Proceeds will be used to refinance existing debt and for general corporate purposes.

Sumitomo Mitsui raised $500mn via a 5Y bond at a yield of 5.353%, 30bp inside initial guidance of T+200bp area. The bonds have expected ratings of A-. Proceeds will be used for general corporate purposes. The new bonds are priced at a new issue premium of 21.3bp to its existing 3.944% 2028s that yield 5.14%.

Damac Real Estate Development raised $400mn via a 3Y sukuk at a yield of 7.75%, 37.5bp inside initial guidance of 8.125% area. The bonds are rated BB-.

New Bonds Pipeline

- Banco BTG hires for $ bond

- Pertamina Geothermal hires for $ 5Y Green bond

- Mauritius Commercial Bank hires for $ 5Y bond

- Joint Laender hires for € 1 bn 7Y bond

Rating Changes

- Fitch Revises Outlook on Casino’s Ratings to Negative; Affirms Ratings

- Fitch Withdraws Sri Rejeki Isman’s Ratings

Term of the Day

Non-Call Risk

As the name suggests, this is the risk of bonds not getting called by the issuer. This is particularly significant in the case of far maturity bonds, Perpetual Bonds (Perps) and AT1s. While market participants often assume that Perps/AT1s will be called on their first call date, that is not always the case. There are a few examples in recent times. Santander and Deutsche Bank shocked the markets in 2019 and 2020 when they did not call their AT1s on the first call date. In 2022 where Allianz decided to skip the call on its $1.5bn 3.875% Perp in February, which led to a fall in its price. Investors must thus account for non-call risk when investing in such bonds.

Talking Heads

On Bonds and gold to outperform equities – StanChart

“With the increased levels of uncertainty across the globe, investors are best served by diversifying their portfolios across asset classes and geographies… at a time when income generating assets remain attractive, we believe that investors have a window to lock in an attractive yield given that the Fed is likely to approach the peak of its hiking cycle in the next few months… economic outlook for the US, Europe and China have diverged with an increased risk of a recession in the US and Europe and a turnaround in China. To capitalise on this, investors have the chance to increase their allocation to Bonds while capturing the opportunity provided by China equities”

On Goldman Changing ECB Call With a 3.75% Terminal Rate

“A half-point move is quite possible with stronger data, including limited signs of a further deterioration of bank lending conditions and a firmer April inflation print. Reasons for a more gradual speed of tightening from here include that the recent banking stresses are likely to leave some mark on bank lending”

On Fed’s Bullard Saying Recession Fears Off-Base and Urging More Hikes

“Wall Street’s very engaged in the idea there’s going to be a recession in six months or something, but that isn’t really the way you would read an expansion like this… labor market just seems very, very strong… doesn’t seem like the moment to be predicting that you have a recession in the second half of 2023”

On This Year’s Top Bond Investors Disagree on Depth of US Recession

Jason Callan of Columbia Threadneedle

“The Fed is being overly aggressive in this cycle as they try and maintain their credibility in managing inflation. There is more likelihood of a harder landing”

Reams Asset Management

There is a risk that the Fed tightens again after a pivot. “That’s definitely part of the calculus for the steps ahead… Our thesis in credit is that you want to be on the long side and we do expect the Fed to pivot and ease. We think the market scrambles for income once we get into a Fed easing cycle”

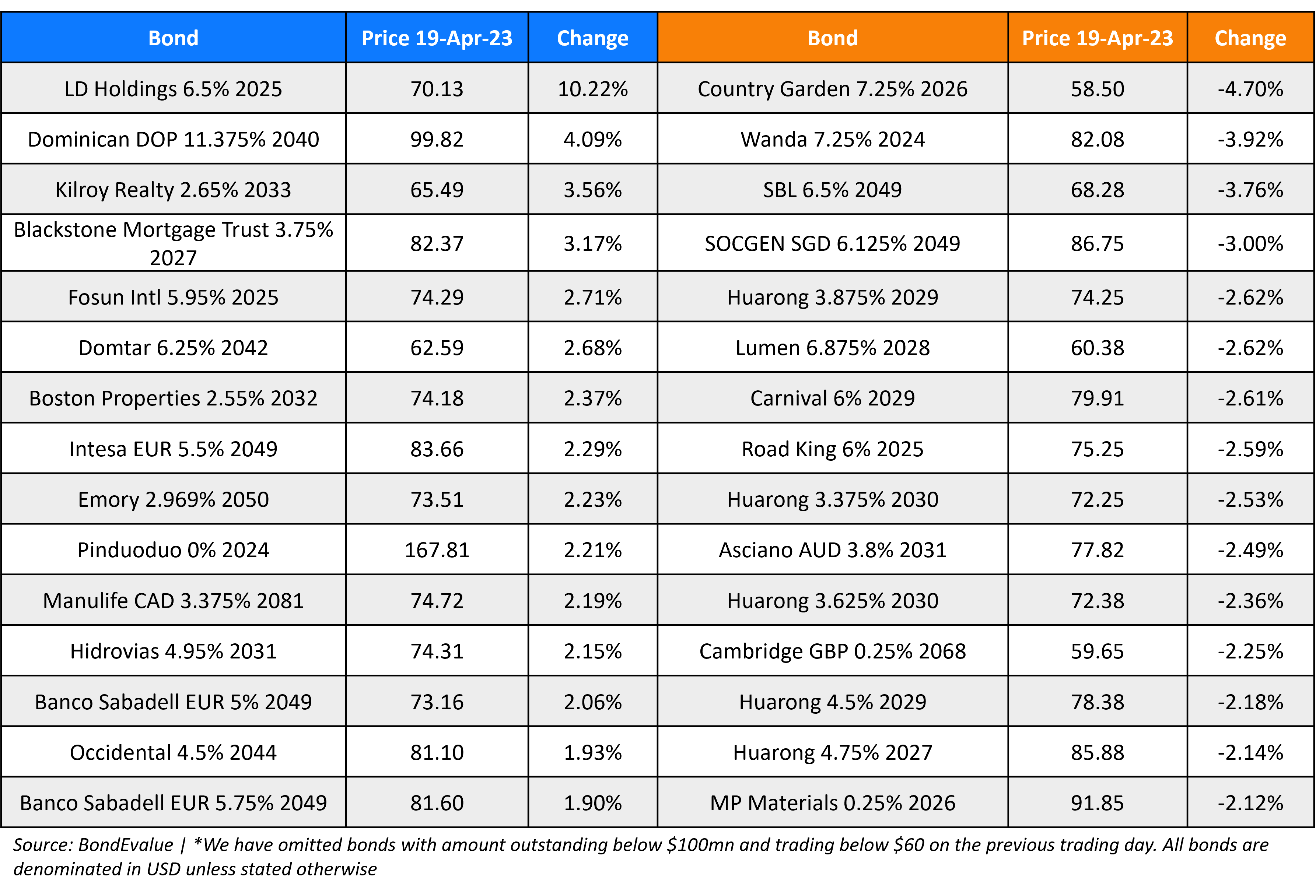

Top Gainers & Losers –19-April-23*

Other News

UBS makes changes to buyback programme following Credit Suisse takeover

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.