This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

May 3, 2023

US Treasuries rallied across the curve as risk-off sentiment grappled markets. Benchmark yields were down sharply with the 2Y yield down by 15bp to 3.97%, below the 4%-mark once again. The 10Y yield was down by 12bp to 3.44%. The move was triggered by renewed fears of a banking contagion possibly spilling over to more regional banks. Stocks of PacWest Bancorp and Western Alliance Bancorp witnessed trading halts yesterday and ended the day lower by 28% and 15% respectively. The S&P bank index fell 2.3%. US equity indices also dropped with the S&P and Nasdaq down 1.1-1.2%.

Amid the broad risk-off sentiment and bid for haven assets, Morgan Stanley and UBS have come out with calls for holding higher-rated bonds compared to equities. They noted that bonds will weather an economic slowdown better than stocks which would suffer more if the Fed fails to navigate a soft landing.

Markets expect the FOMC to announce a 25bp rate hike in today’s meeting with the forward guidance highly anticipated. The Peak Fed funds dropped 8bp to 5.05% for the June meeting. US IG and HY CDS spreads were wider by 2.4bp and 16.8bp respectively.

European equity markets ended lower too. European main CDS spreads were wider by 4bp while Crossover spreads widened 12.8bp. Asia ex-Japan CDS spreads widened by 3.2bp. Asian equity markets have opened in the green today.

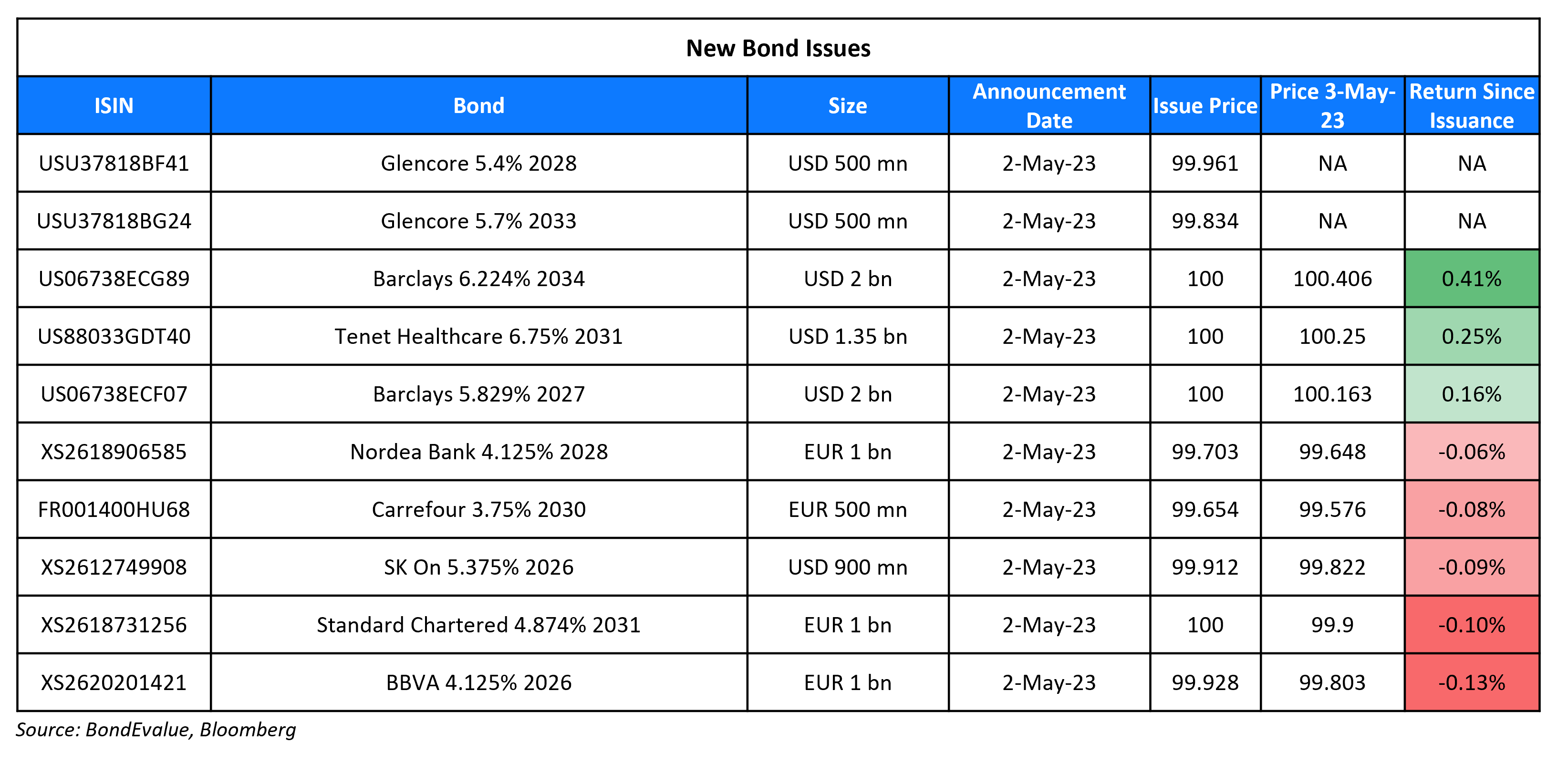

New Bond Issues

SK On raised $900mn via a 3Y green bond at a yield of 5.407%, 40bp inside initial guidance of T+195bp area. The senior unsecured bonds have expected ratings of Aa3, benefiting from a Kookmin Bank guarantee, and received orders over $5.2bn, 5.8x issue size. Asset/fund managers took 74%, bank treasuries 13%, agencies, pension funds and insurers 11%, and private banks and others 2%. APAC took up 80% and EMEA 20% of the offering. Proceeds will be used to finance or refinance, in part or in full, new and/or existing Eligible Projects (as defined in the Green Financing Framework). Notably, the issuer previously had no outstanding US dollar bonds, according to Refinitiv data.

Standard Chartered raised €1bn via a 8NC7 bond at a yield of 4.874%, 20bp inside initial guidance of MS+205bp area. The bonds have expected ratings of A3/BBB+/A, and received orders over €1.6bn, 1.6x issue size. Proceeds will be used for general corporate purposes.

BBVA raised €1bn via a 3NC2 bond at a yield of 4.163%, 23bp inside initial guidance of MS+90bp area. The senior preferred bonds have expected ratings of A3/A/A-, and received orders over €1.75bn, 1.8x issue size. It also has a 75% clean-up call (Term of the Day, explained below). The new bonds are priced 50.3bp wider to its existing 0.75% 2025s that yield 3.66%.

Barclays raised $4bn via a two-tranche deal. It raised:

- $2bn via a 4NC3 bond at a yield of 5.829%, 15bp inside initial guidance of T+230bp area. The new bonds are priced 18.9bp wider to its existing 4.375% 2026s that yield 5.64%.

- $2bn via a 11NC10 bond at a yield of 6.224%, 15bp inside initial guidance of T+295bp area.

The senior unsecured bonds have expected ratings of Baa1/BBB/A. Proceeds will be used for general corporate purposes and to further strengthen the capital base of both, the issuer and its subsidiaries and/or the group.

New Bonds Pipeline

- Banco BTG hires for $ bond

Rating Changes

- WeWork Cos. LLC Downgraded To ‘SD’ From ‘CC’ Following Completion Of Distressed Exchange

- Moody’s downgrades First Republic Bank and will withdraw the ratings

Term of the Day

Clean-Up Call

A clean-up call refers to a call provision, whereby once a stated percentage of a security is retired, the issuer is obliged to call the remainder of the tranche. While clean-up calls are generally more commonly observed in mortgage-backed securities (MBS), they may also be present as a feature in some bonds. This is different from a normal call option in a bond where the issuer has an option to redeem their bond fully during the specified call date./period.

For example, BBVA yesterday priced a €1bn 3NC2 bond with a 75% clean-up call. This indicates that once 75% of the bond is called back, the issuer is obligated to immediately redeem the remaining 25%.

Talking Heads

On Morgan Stanley, UBS Pick Bonds Over Stocks on Recession Risk

Tai Hui, JPMorgan Asset Management’s chief Asia market strategist

“I do think the opportunity overall still favors fixed income at this point. For equities, valuation for the US is still not particularly cheap and I think earnings expectations are still too optimistic”

Hartmut Issel, head of APAC equity and credit at UBS Global Wealth Management

“Investors should lock in yield in investment-grade, high-grade and emerging markets sovereign bonds, and consider more selective equity exposure in emerging markets… High-grade and investment-grade bonds still provide some protection against recession risks “

Lisa Shalett, CIO at Morgan Stanley Wealth Management

“Stock investors have to cope with the fact that multiples may contract at the same time that earnings begin to fall. That’s a very kind of dangerous combination.”

On Traders Zeroing In on June US Default Risk, Pushing Yields Above 5%

TD Securities strategist Gennadiy Goldberg

“The move in bills is a repositioning for the new X-date with the aid of morning market liquidity. The news yesterday came out a bit too late for the market to properly reprice… given the early-June warning by both Yellen and the CBO, markets have to take notice”

Wrightson ICAP economist Lou Crandall

“We suspect that the June X-date outlook will remain fluid at least until after the middle of this month,” Crandall wrote in a note to clients”

On Fed in stride to pole-vault 5% policy rate, then perhaps catch its breath

Matthew Luzzetti, chief US economist at Deutsche Bank

“Our base case remains that the May hike will be the last of this cycle as the economy responds to the tightening to date… we see risks tilted toward another increase in June. (Fed) Chair (Jerome) Powell is likely to emphasize the continued need for a hawkish bias to tame inflation, but not commit to any decision at the June meeting”

Torsten Slok, chief economist with Apollo Global Management

“”It usually takes 12 to 18 months for the Fed to soften the labor market and today is no different”

On Most Bank Trauma Over, More Worried About Debt Limit – Former US Treasury Secy, Larry Summers

“We are probably over the vast majority of the banking traumas. I’m not highly alarmed by what’s happening in the banking sector… more alarmed by what’s happening in the political sector.

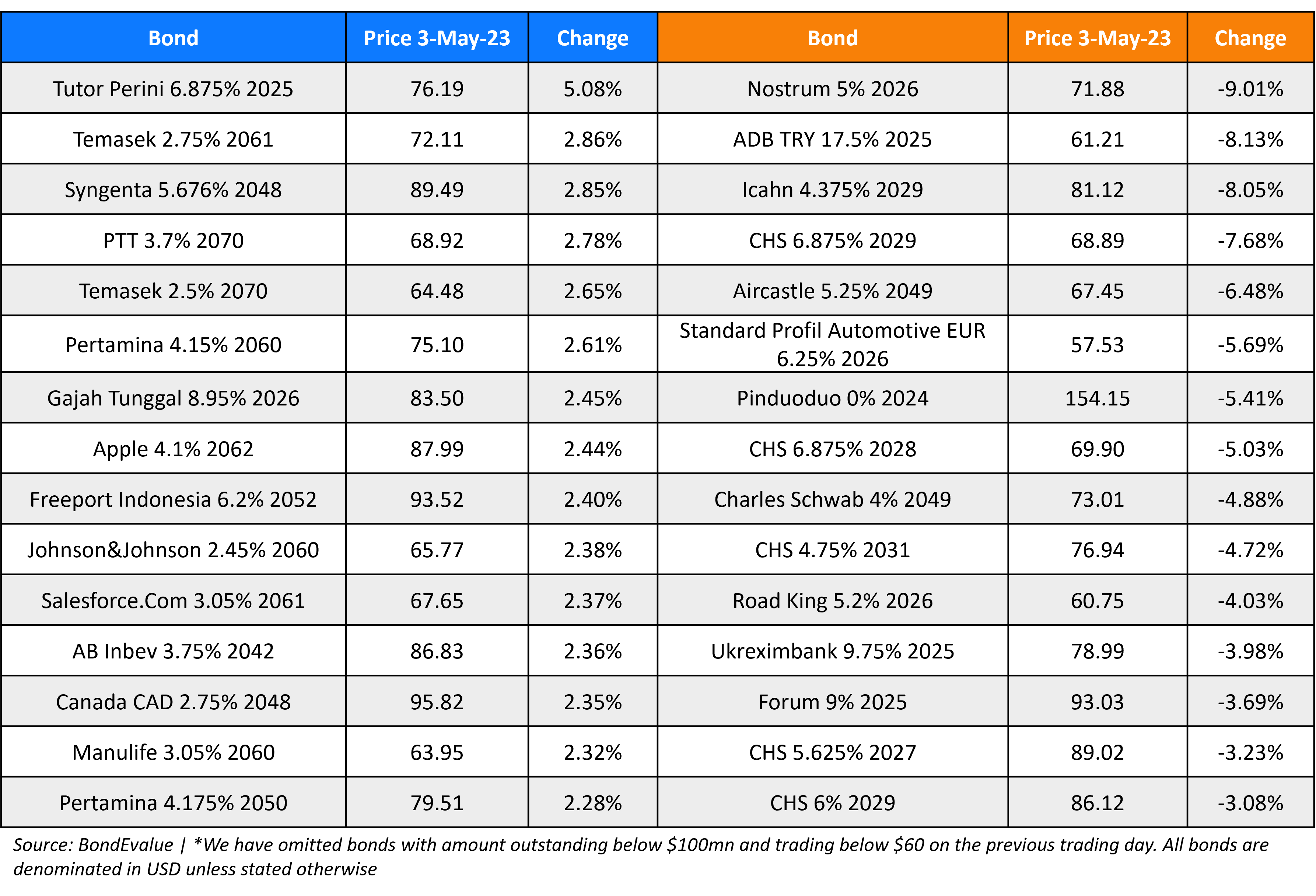

Top Gainers & Losers – 03-May-23*

Other News

China Builder Jiayuan Gets Court Order to Liquidate Assets

Icahn Enterprises’ Dollar Bonds Drop Over 7% on Hindenburg’s Short Selling Report

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.