This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

May 9, 2023

US Treasury yields continued to move higher across the curve, rising by 7bp. The 2Y yield is again back at the 4% mark after having gone as low as 4.80% amid the banking stress last week. The Federal Reserve released its Financial Stability Report highlighting concerns over credit tightening and financial stress in the system. It said this could “drive up the cost of funding for businesses and households, potentially resulting in a slowdown in economic activity”. Regarding domestic banks, it said that there is ample liquidity.

The peak Fed Funds Rate was up 1bp to 5.09% and markets expects no change in policy rates at the Fed’s June meeting. The overall market was rangebound yesterday with the S&P and Nasdaq up 0.1% and 0.2% respectively. Also, US IG and HY CDS spreads were wider by 0.8bp and 2.7bp respectively.

European equity markets ended marginally higher with UK markets being closed. European CDS markets were closed yesterday. Asia ex-Japan CDS spreads also tightened by 0.8bp. Asian equity markets have opened broadly in the green today.

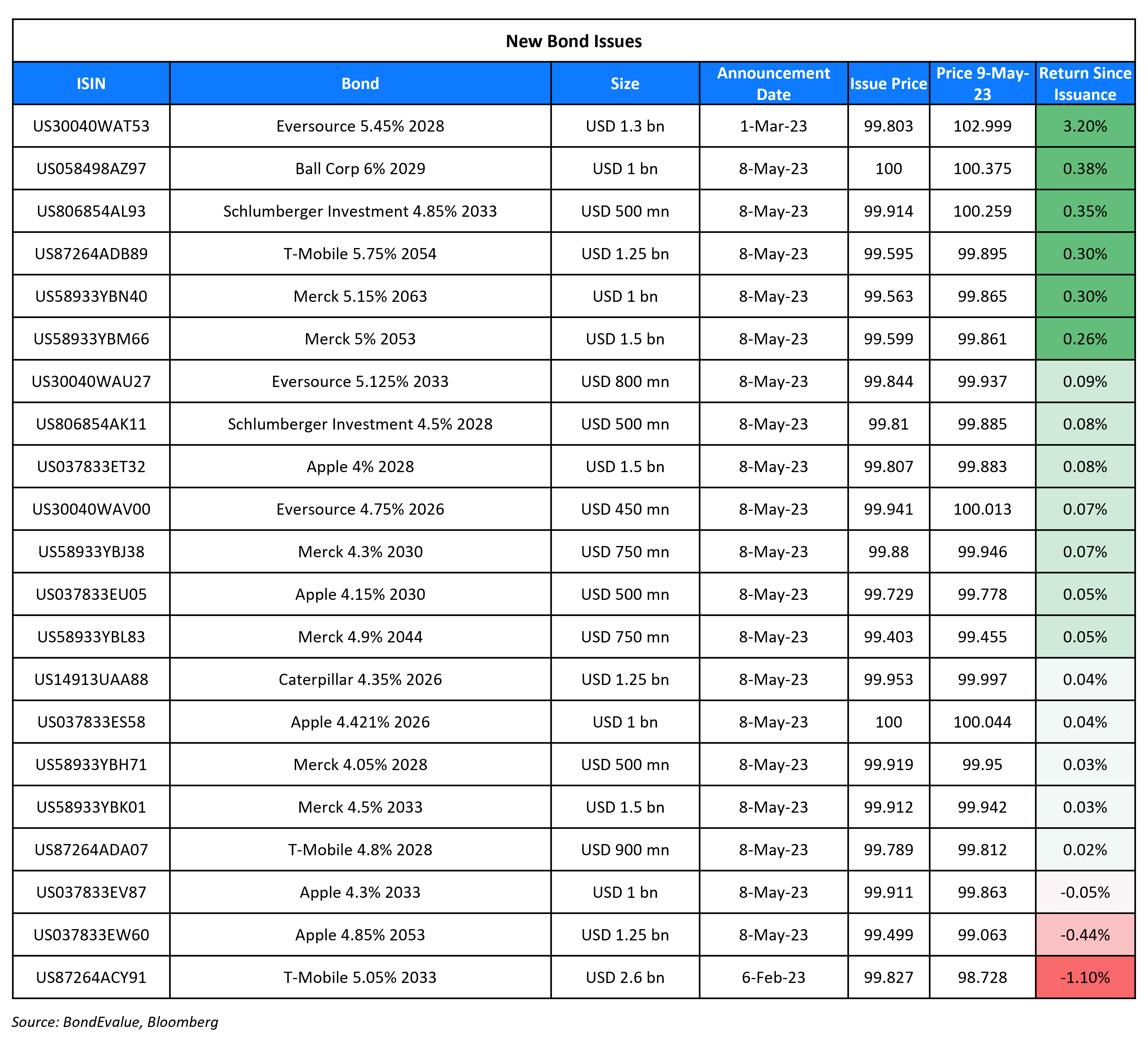

New Bond Issues

- Eximbank China $ 3Y at T+75bp area

- Bayfront Infrastructure $ 3Y at T+70bp area

T-Mobile raised $3.5bn via a three-tranche deal. It raised:

- $900mn via a 5Y bond at a yield of 4.848%, 20bp inside initial guidance of T+155bp area. The new bonds are priced 8.2bp tighter to its existing 4.75% 2028s that yield 4.93%

- $1.35bn via a tap on its 5.05% 2033s at a yield of 5.237% (computed using UST 10Y on 8 May 2023), 22bp inside initial guidance of T+195bp area.

- $1.25bn via a 30Y bond at a yield of 5.779%, 25bp inside initial guidance of T+220bp area.

The bonds have expected ratings of Baa2/BBB-/BBB+. Proceeds will be used for general corporate purposes, which may include share repurchases and refinancing of existing debt. The notes will be settled on 11 May 2023.

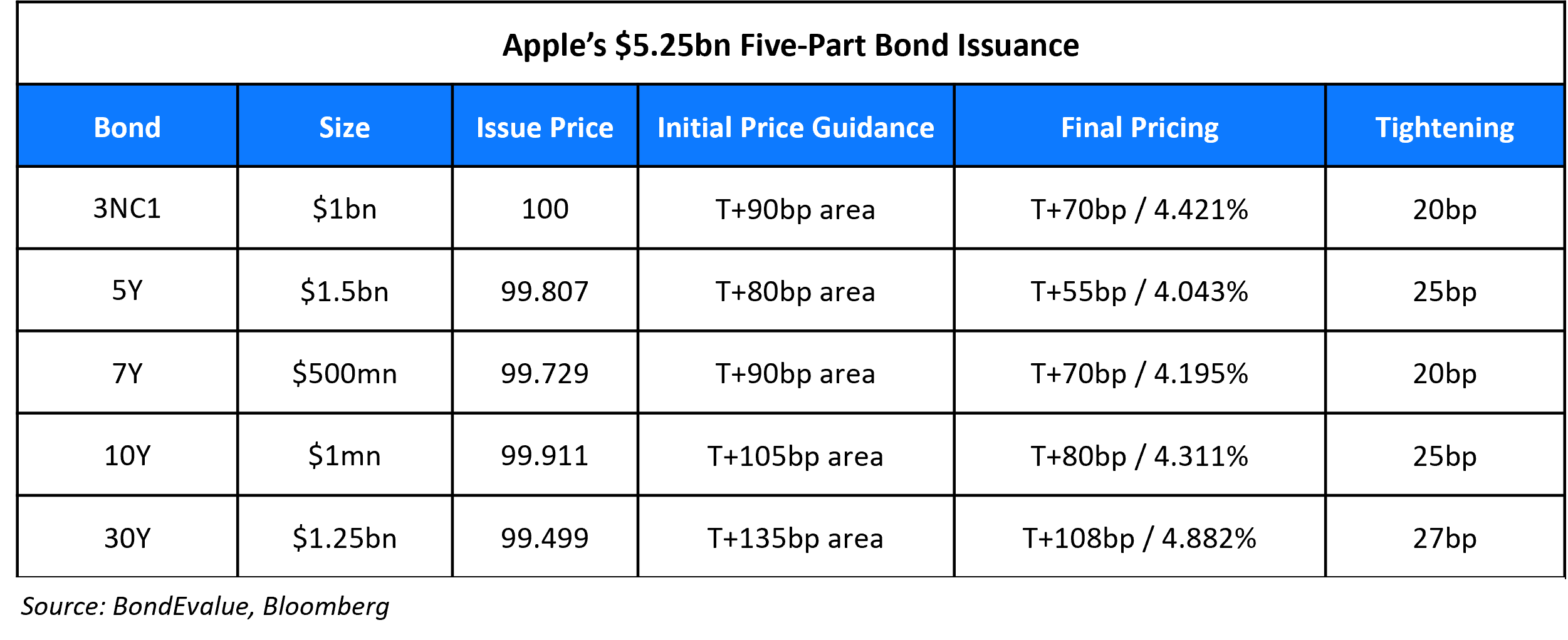

Apple raised $5.25bn via a five-trancher. Details are given in the table below:

The bonds have expected ratings of Aaa/AA+. Proceeds will be used for general corporate purposes, including stock buybacks and payment of dividends, funding for working capital, capital expenditures, acquisitions and debt repayment. The new 5Y notes were priced at a new issue premium of 7.3bp, compared to its existing 1.4% 2028s that yield 3.97%. The new 7Y notes were priced at a new issue premium of 6.5bp, compared to its existing 1.25% 2030s that yield 4.13%.

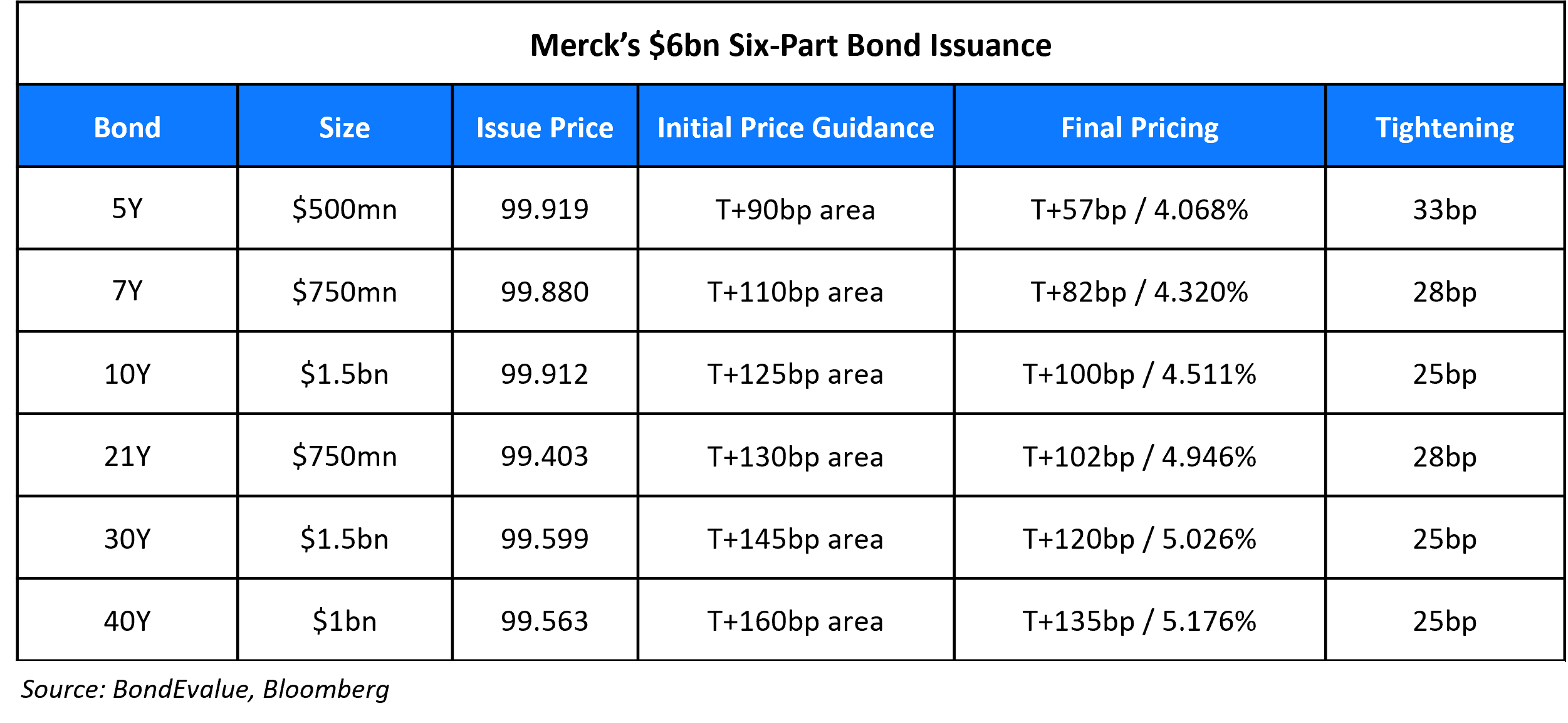

Merck raised $6bn via a six-trancher. Details are given in the table below:

The bonds have expected ratings of A1/A+. Proceeds will be used for general corporate purposes including to fund a portion of the cash consideration payable in connection with the Prometheus acquisition as well as to repay commercial paper borrowings and other upcoming maturities.

New Bonds Pipeline

- Korea Credit Guarantee Fund hires for $ 3Y Social bond

- Melbourne Airport hires for € 10Y bond

Rating Changes

- Fitch Upgrades Caterpillar to ‘A+’; Outlook Stable

- Moody’s affirms Anton’s B1 ratings; changes outlook to stable

Term of the Day

Sukuk

A Sukuk is a sharia-compliant fixed income instrument that essentially works similar to bonds. In a Sukuk, key differentiators vs. conventional bonds are: – Investors share partial ownership of an asset rather than it being a debt obligation by the issuer – The pricing is based on the underlying value of assets rather than credit worthiness – The holder receives a share of underlying profits rather than interest payments (considered ‘riba’) Sharia compliance broadly implies that any profits derived from these funding arrangements must be derived from commercial risk-taking and trading only; that interest income is prohibited on lending activities and; that the assets must be halal. To learn more about sukuk, click here

GCC bonds and sukuk issuances have dropped 22% YoY in 1Q 2023 to $28.3bn

Talking Heads

On Goldman Sachs Joining Barclays to Bet Against Fed Rate Cuts This Year

When the Fed has done a series of rate increases followed by two decisions to make no change, the most common subsequent course over the next six months “has been an on-hold Fed…. argue against the extent of easing currently priced for this year.”

On Economy Signaling Weaker Earnings – Morgan Stanley’s Michael Wilson

“Many of the leading macro data points that we focus on have fallen in recent weeks and are not pointing to a similar run rate in terms of strength looking forward over the next several months… skeptical as labor costs continue to be a headwind for corporates and our leading margin gauge points to additional margin downside “

On Preferring Fixed Income to Equities – UBS Chief Investment Office (CIO)

As credit spreads have compressed from their mid-March peaks, IG financial spreads still stand at their widest levels relative to non-financials since 2012… IG bonds can provide a better risk-adjusted return than HY in 2023. With the economy slowing, IG companies are in a stronger fundamental position and should see less downward pressure… US Big 6 bank bond spreads are about 12bps wider than their beginning-of-March levels, whereas non-US bank spreads are 25bps wider and US regional bank spreads are 86bps wider.

China Debt Restructuring at Impasse, World Bank Chief, David Malpass

“From China’s side, they are working to try to pull all their creditors together into a coordinated position, but it’s still a stalemate as far as progress being made. It’s been frustrating because of lack of progress”

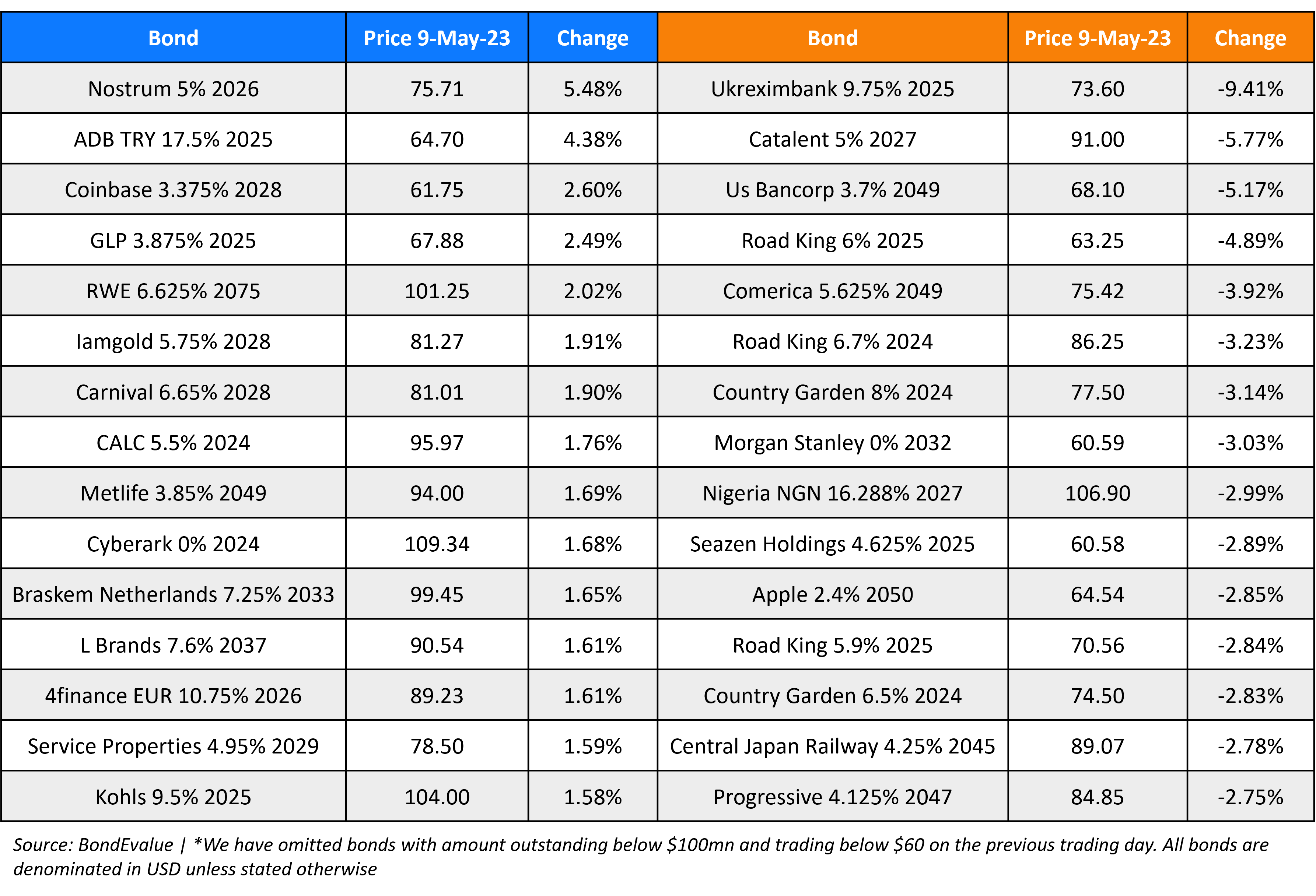

Top Gainers & Losers – 09-May-23*

Other News

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.