This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

May 26, 2022

US equity markets rose on Wednesday, with the S&P and Nasdaq up 1% and 1.5% respectively. Sectoral gainers were led by Consumer Discretionary, up 2.8%, followed by Energy and IT, up over 1.5% each. US 10Y Treasury yields were 1bp lower to 2.76%. European markets ended higher as well with the DAX, CAC and FTSE up 0.6%, 0.7% and 0.5% respectively. Brazil’s Bovespa closed flat. In the Middle East, UAE’s ADX was up 0.9% and Saudi TASI was up 2.3%. Asian markets have opened weaker today – Shanghai, HSI and Nikkei were down 0.9%, 1.5%, 0.5% respectively while STI was up 0.2%. US IG CDS spreads tightened 4.4bp and HY spreads tightened 21bp. EU Main CDS spreads were 3.8bp tighter and Crossover spreads were 16.2bp tighter. Asia ex-Japan CDS spreads were 4.7bp tighter.

The FOMC’s May meeting minutes showed that officials agreed they need to hike rates in steps of 50bps at their next two meetings, which gives them room to alter rates later if needed.

Advanced Two-Day Course on Bonds | 7-8 June

Keen to develop a deeper understanding of bonds? Sign up for our upcoming IBF-recognized course on bonds, scheduled for 7-8 June. This course is ideal for finance professionals, with 80/90% IBF funding available to eligible company-sponsored candidates from Singapore. There will be an option to attend virtually as well. Click on the banner below for details about the course modules, instructor profiles, fees and funding.

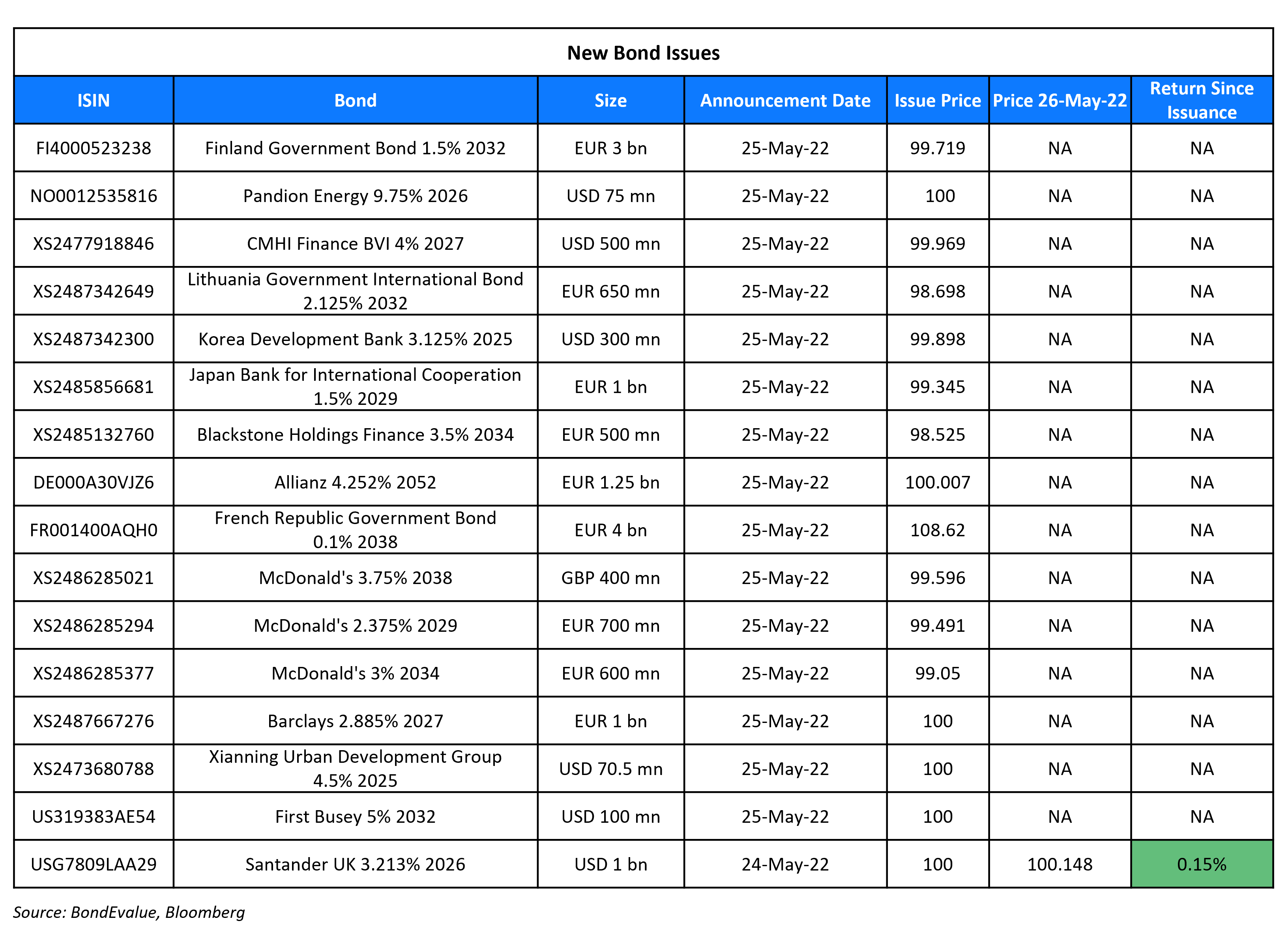

New Bond Issues

- Thai Exim Bank $ 5Y at T+160bp area

- Zhangzhou Transportation Development Group $ 3Y at 5.4% area

Barclays raised €1bn via a 4NC3 bond at a yield of 2.885%, 22bp inside initial guidance of MS+190bp area. The senior unsecured bonds have expected ratings of Baa2/BBB/A, and received orders over €2.3bn, 2.3x issue size. Proceeds will be used for general corporate purposes and may be used to strengthen further its capital base. Its 2.885% coupons will reset at 1Y MS + 168bp, if not redeemed on its optional redemption date of Jan 31, 2026.

Allianz raised €1.25bn via a 30.1NC10.1 bond at a yield of 4.252%, 15bp inside initial guidance of MS+270bp area. The subordinated Tier 2 bonds have expected ratings of A2/A+, and received orders over €1.9bn, 1.5x issue size. The proceeds will be used for general corporate purposes, including the refinancing of existing debt. Its 4.252% coupons are fixed until the first reset date of July 5, 2032, and will reset at 3m Euribor+255bp if not redeemed.

China Merchants Port raised $500mn via a 5Y bond at a yield of 4.007%, 45bp inside initial guidance of T+175bp area. The senior unsecured bonds are rated Baa1, and received orders over $3.3bn, 6.6x issue size. Banks and financial institutions took 59%, fund and asset managers 29%, corporates 10%, and insurers and private banks 2%. Asia accounted for 96% and EMEA 4%. There is a change of control (Term of the Day, explained below) event clause at 101. Proceeds will be used for general corporate needs, including debt refinancing.

New Bonds Pipeline

-

Zhangzhou Transportation Development Group hires for $ Green bond

- Busan Bank hires for $ Social bond

- Kookmin Card hires for $ Sustainability bond

- Continuum Energy Aura hires for $ Green Bond

- Jubilant Pharma hires for $ bond

- Sael Limited hires for $ 7Y Green bond

Rating Changes

- Moody’s downgrades Jiangsu Zhongnan’s ratings to Caa2/Caa3; outlook remains negative

- French Food Service Provider Elior Group Downgraded To ‘B+’ On Slower-Than-Expected Recovery; Outlook Stable

Term of the Day

Change of Control

Change of control is a covenant in bond offerings, mentioned in the bond’s prospectus where there typically is a change in ownership of the issuer. This can lead to structural changes in the bond like a coupon step-up or in the form of a ‘change of control put’ where bondholders have the option to sell the bonds back to the issuer at a pre-defined price upon the occurrence of the change of control event.

Talking Heads

On Fed’s Brainard seeing the case for central bank digital currency

“As we assess the future digital financial system, it is prudent to consider how to preserve ready public access to safe central bank money, perhaps through the digital analogue of the Federal Reserve’s issuance of physical currency… We recognize there are risks of not acting, just as there are risks of acting

On Sri Lanka’s Hopes of an IMF Loan by mid-June

Guido Chamorro, co-head of emerging-market hard-currency debt at Pictet Asset Management

“It is good news that Sri Lanka is placing a priority on talks with the IMF. The sooner the better, but I think it is difficult to put an exact date on a resolution. These negotiations typically end up taking a bit longer than initially expected.”

“If inflation goes up and nominal interest rates do not anything like as much, that effectively is a decline in real interest rates. It’s extraordinary that this should have been allowed… It’s a very, very difficult situation for the ECB — it’s harder in many ways for the ECB than it is for the Fed — because it’s much more, as Philip rightly said, a supply shock for Europe rather than for the US. Dealing with a supply shock is a great deal more difficult than dealing with a demand shock… If you’ve got inflation at 7.5% and maybe rising, that already has given a massive hit to your standards of living… Virtually all the central banks including the ECB are an awful long way behind the curve.”

On the war in Ukraine may trigger global recession – World Bank President David Malpass

“As we look at the global GDP … it’s hard right now to see how we avoid a recession… The idea of energy prices doubling is enough to trigger a recession by itself

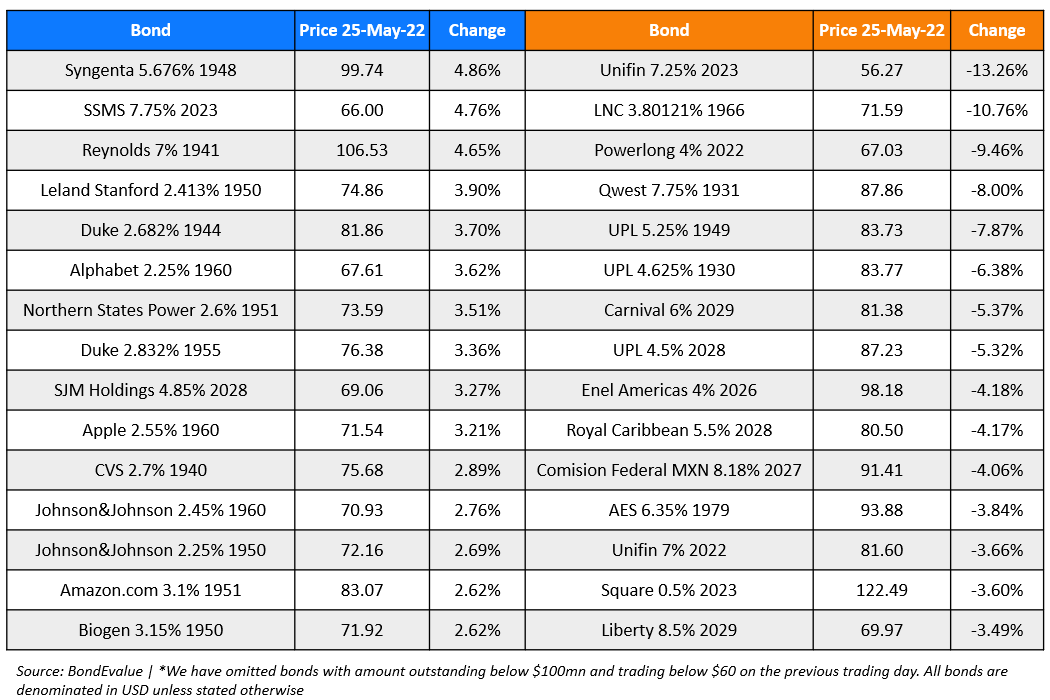

Top Gainers & Losers – 26-May-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.