This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers & Losers

March 21, 2023

US Treasury yields inched higher late on Monday after a slight reversal in the risk-off sentiment. The 2Y yield rose 5bp to 3.98% (up 37bp from intraday lows) while the 10Y rose 3bp to 3.50%. The peak Fed funds rate climbed 2bp to 4.87% as markets continue to price in a 25bp hike at tomorrow’s FOMC meeting (72% probability). Goldman Sachs on the other hand expects the Fed to hold rates, contrary to most other street estimates. Bank stocks recouped some of the losses with the S&P 500 Banks Equity Index up 0.58% and most banks’ AT1s also trading higher following Monday’s sell-off (more details below). US IG and HY CDS spreads rose ~1bp each. US equity markets inched higher with the S&P and Nasdaq up 0.9% and 0.4% respectively.

European equity markets too staged a recovery. European main CDS spreads eased 1.8bp while Crossover spreads rose 7bp. Asia ex-Japan CDS spreads rose sharply by 7.3bp while Asian equity markets have opened in the green, led by the STI up 1.3%.

.png)

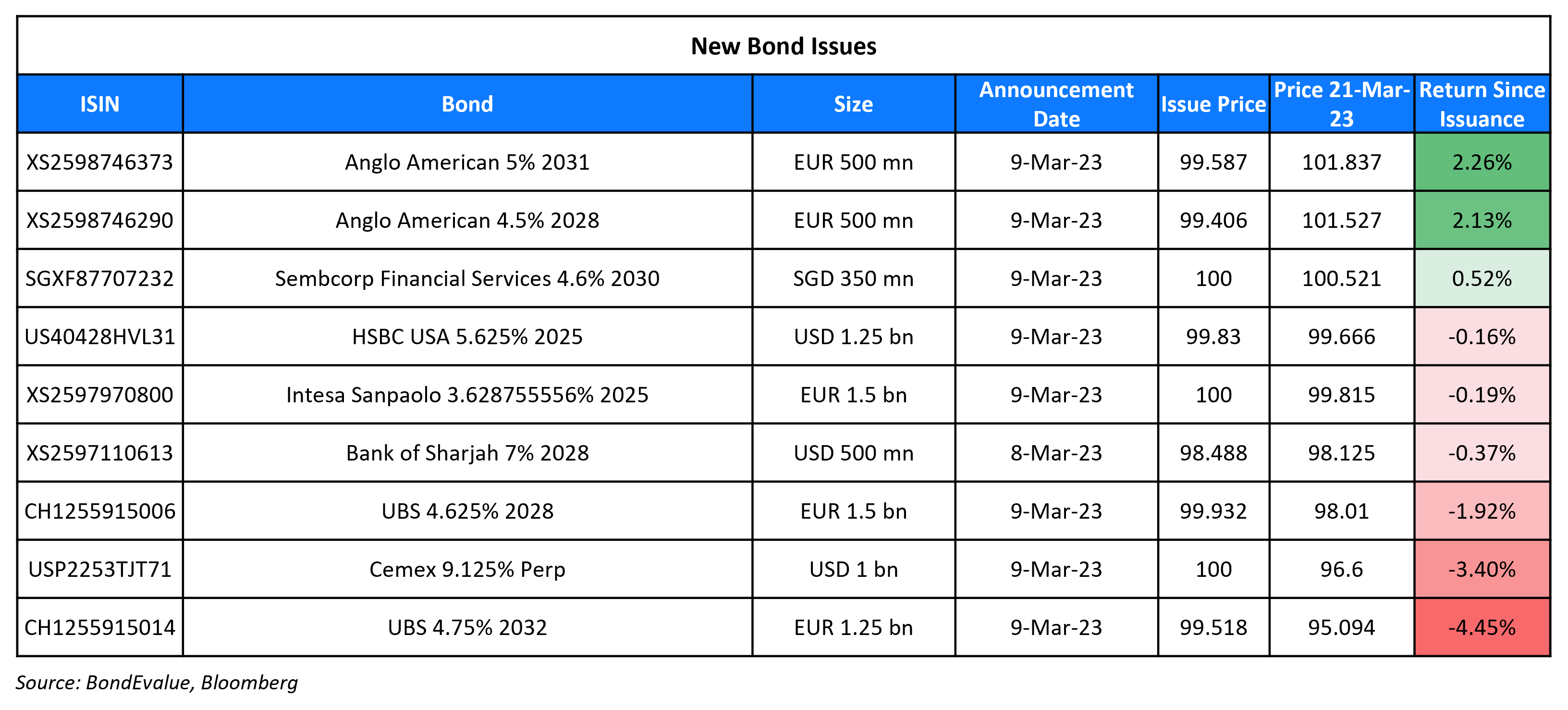

New Bond Issues

New Bonds Pipeline

- Shinhan Bank hires for $ senior bond

- REC hires for $ Long 5Y Green bond

- Qatar plans for $ bond

Rating Changes

- Moody’s affirms the ratings of UBS Group AG (A3 Senior Unsecured) and changes outlook to negative

- Outlook On UBS Group Revised To Negative On Execution Risk From Credit Suisse Acquisition; Ratings Affirmed

-

Moody’s places Credit Suisse Group ratings on review for upgrade

- Credit Suisse Placed On CreditWatch Positive On Acquisition By UBS; Tier 1 Hybrids Downgraded To ‘C’

- Fitch Upgrades PG&E Corp.’s and Pacific Gas and Electric’s IDRs to ‘BB+’; Outlook Stable

Term of the Day: Tier 2 Bonds

Tier 2 bonds are debt instruments issued by banks to meet their regulatory tier 2 capital requirements. Tier 2 capital (and thus tier 2 bonds) rank senior to tier 1 capital, which consists of common equity tier 1 (CET1) and additional tier 1 (AT1) capital. CET1 consists of a bank’s common shareholders’ equity while AT1 consists of preferred shares and hybrid securities or perpetual bonds. Tier 2 capital consists of upper tier 2 and lower tier 2 wherein the former is considered riskier to the latter. From a bond investor’s perspective, tier 2 bonds are senior, and therefore less risky compared to AT1 bonds as AT1s would be the first to absorb losses in the event of a deterioration in bank capital, as was the case with Credit Suisse.

Talking Heads

BlackRock Investment Institute strategists

“We stay risk-off: underweight developed market (DM) stocks and trim credit to neutral. But we are ready to seize opportunities as macro damage gets priced in. We overweight very short-term government paper for income and prefer emerging markets”

Lotfi Karoui, chief credit strategist at Goldman Sachs

“(The sell-off) was a knee jerk reaction to an outcome that took a lot of people by surprise … In the long term, we are a little concerned about the potential permanent destruction in demand … investors will have to re-assess how the risk-reward looks like in those instruments, particularly at times of rising financial distress.”

Esther Perez Ruiz, the IMF’s resident representative for Pakistan

“Ensuring there is sufficient financing to support the authorities in the implementation of their policy agenda is the paramount priority … Fund staff are seeking greater details on the scheme in terms of its operation, cost, targeting, protections against fraud and abuse, and offsetting measures, and will carefully discuss these elements with the authorities”

“The banking crisis has already had the effect of a meaningful tightening of financial conditions … We don’t yet know where the losses are for investors in these institutions and what the contagion effects may be … This is not an environment into which the @federalreserve should be raising rates and adding additional pressure on the system as financial stability is the Fed’s first responsibility.”

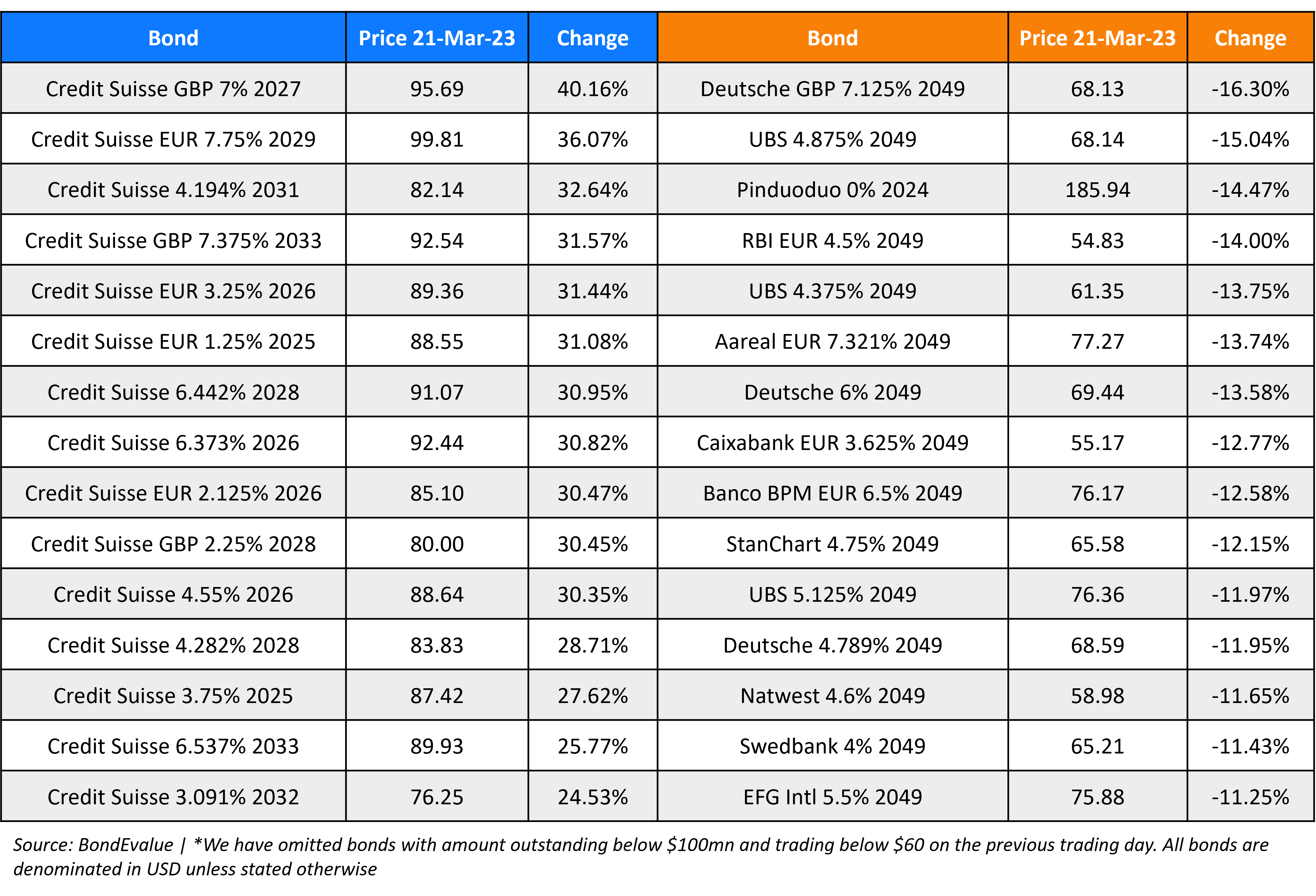

Top Gainers & Losers – 21-March-23*

Go back to Latest bond Market News

Related Posts:

1, 2, 3, 4th Fed Hike!

June 14, 2017

Fed Survey Results Supportive of Funds Flow into Bonds

September 10, 2017

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.