This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

BOC Aviation Launches $ Bonds; Macro; Rating Changes; Talking Heads; New Issues; Top Gainers and Losers

May 16, 2023

US Treasury yields were marginally higher across the curve 1-4bp. US Treasury Secretary Janet Yellen reiterated that the Treasury department may run out of cash as soon as June 1 unless the Congress raises or suspends the debt limit. The peak Fed Funds Rate rose 1bp to 5.11% as markets expect no change in the Fed’s policy meeting in June. Equity indices closed higher with the S&P up 0.3% and Nasdaq up 0.7%. US IG and HY CDS spreads were almost flat.

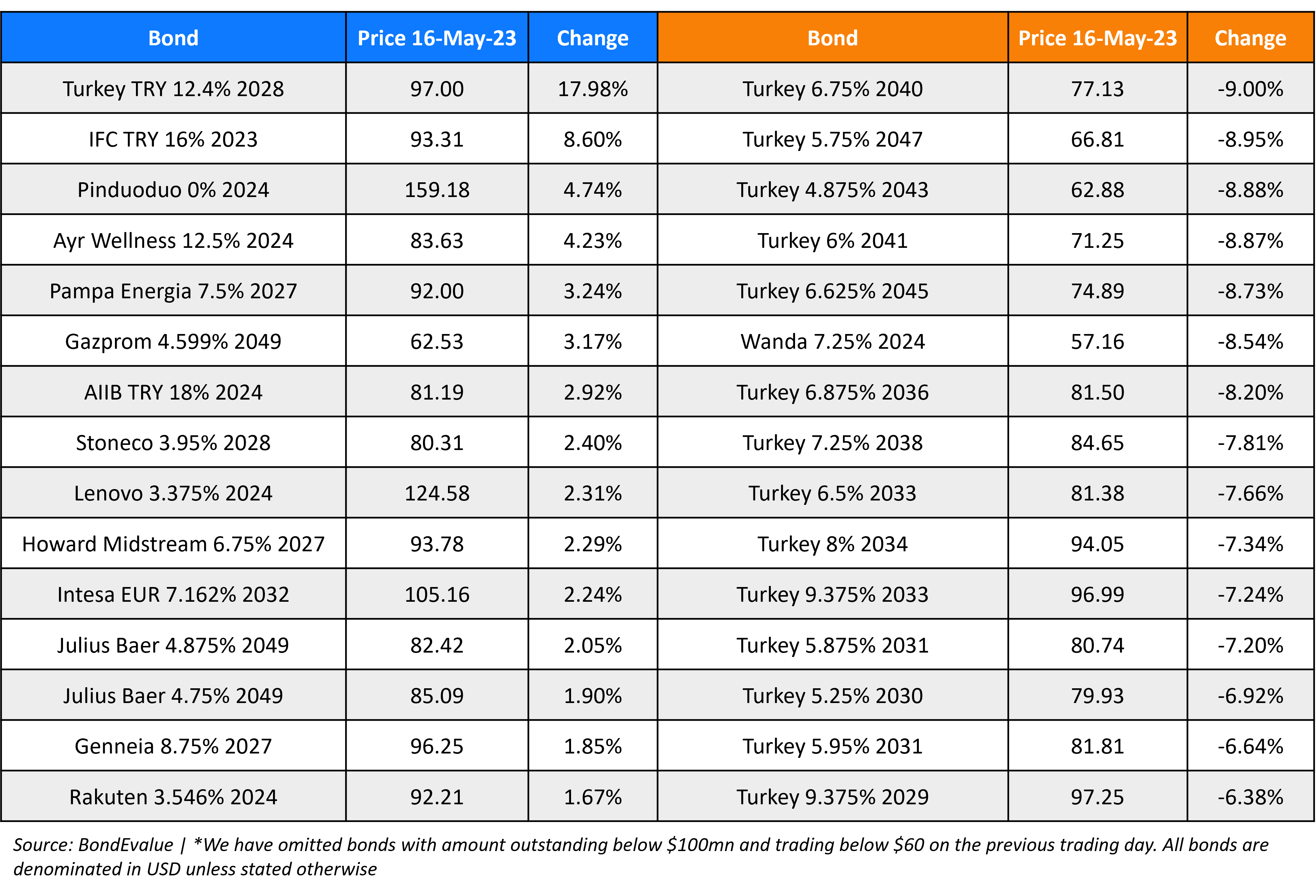

European equity markets ended flat. European main CDS spreads were 0.1bp wider and crossover CDS spreads were 0.6bp tighter. Asia ex-Japan CDS spreads tightened by 1bp. Asian equity markets have opened in the green today. Turkey’s dollar bonds dropped sharply across the curve on a stronger-than-expected support for Erdogan, boosting his chances of a re-election during the second round run-off on May 28 (scroll below for more details).

.png)

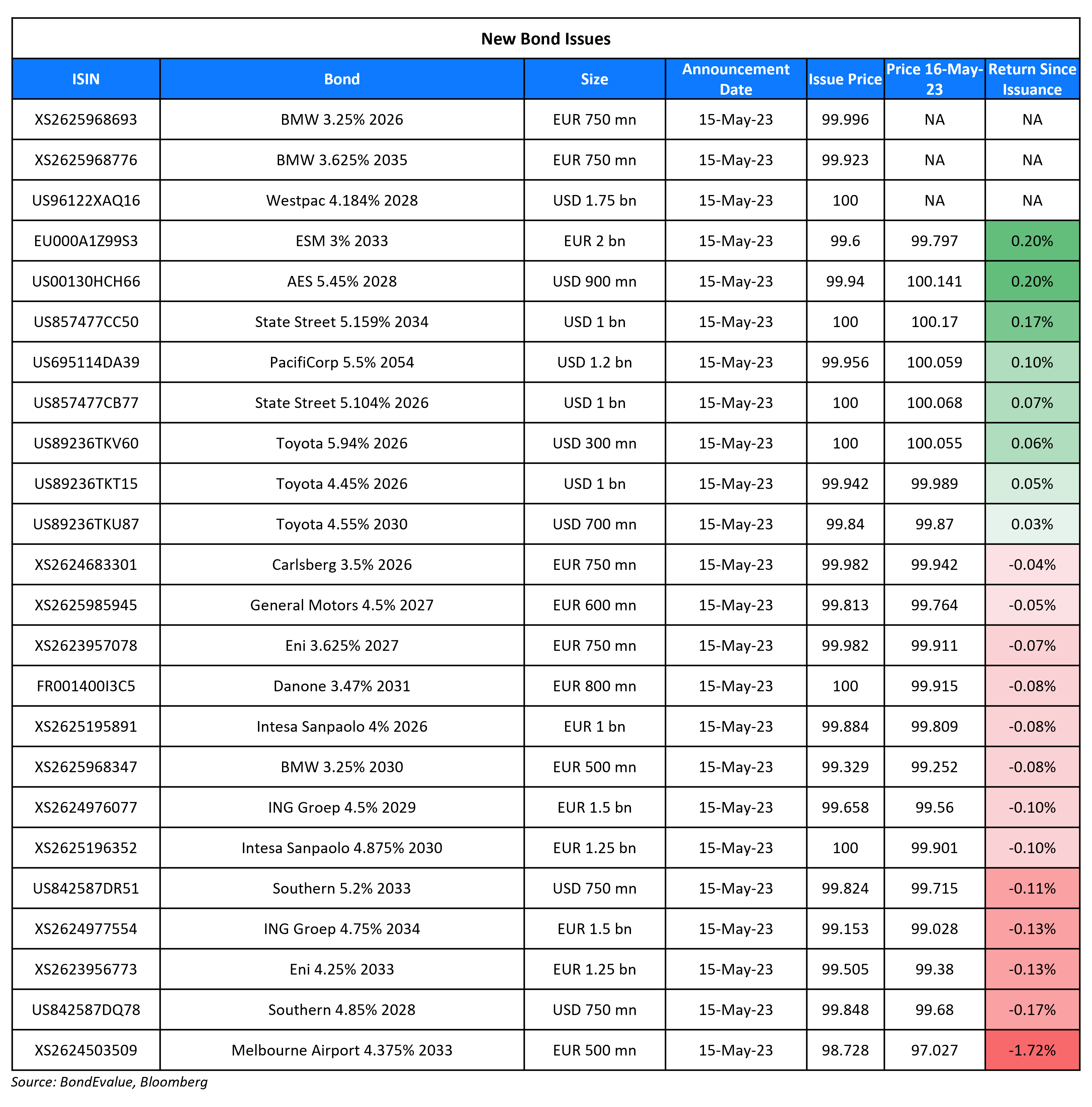

New Bond Issues

- ST Engineering $ 3Y at T+75bp area

- BOC Aviation $ 5Y at T+160bp area

- Shandong Hi-Speed $ 3Y at 5.7% area

ING raised €3bn via a two-part deal. It raised €1.5bn via a 6NC5 bond at a yield of 4.578%, 20bp inside initial guidance of MS+180bp area. It also raised €1.5bn via a 11NC10 bond at a yield of 4.859%, 20bp inside initial guidance of MS+210bp area. The 6NC5s received orders over €2.5bn, 1.7x issue size and the 11NC10s received orders over €3bn, 2x issue size. The senior unsecured bonds have expected ratings of Baa1/A-/A+.

General Motors raised €600mn via a 4.5Y bond at a yield of 4.553%, 25bp inside initial guidance of MS+180bp area. The bonds have expected ratings of Baa2/BBB/BBB-, and received orders over €1.2bn, 2x issue size. Proceeds will be used for general corporate purposes.

Intesa Sanpaolo raised €2.25bn via a two-tranche green deal. It raised €1bn via a 3Y Green bond at a yield of 4.042%, 25bp inside initial guidance of MS+115bp area. It also raised €1.25bn via a 7Y Green bond at a yield of 4.875%, 25bp inside initial guidance of MS+220bp area. The 3Y note received orders over €1.9bn, 1.9x issue size and the 7Y note received orders over €2.8bn, 2.2x issue size. The new 7Y was priced a new issue premium of 12.5bp to its existing 5.25% social bonds due 2030 that yield 4.75%. The senior preferred bonds have expected ratings of Baa1/BBB/BBB and have 75% clean-up calls. Proceeds will be allocated to finance or refinance Green Categories defined within Intesa Sanpaolo’s Green, Social & Sustainability Bond Framework dated June 2022.

Westpac raised $1.75bn via a 5Y covered bond (Term of the Day, explained below) at a yield of 4.184%, 5bp inside initial guidance of MS+97bp area. The bonds have expected ratings of Aaa/AAA (Moody’s/ Fitch). Proceeds will be used for general corporate purposes.

New Bonds Pipeline

- EDF hires for $ bond

- BGK hires for $ 10Y bond

- Korea Credit Guarantee Fund hires for $ 3Y Social bond

- GS Caltex hires for bond

Rating Changes

- Moody’s upgrades Oman to Ba2, maintains positive outlook

- Moody’s upgrades China Merchants Bank’s deposit ratings to A2; changes outlook to stable

Term of the Day

Covered Bond

Covered bonds are senior secured debt instruments that are typically issued by banks. These bonds are secured (i.e. covered) by a pool of assets referred to as the “cover pool”, which typically consists of mortgages or loans. In an event that the bank defaults, holders of covered bonds have a preferential claim to the cover pool, which ensures interest payments and repayment of principal. This makes covered bonds relatively more secure vs. other debt and therefore results in a higher credit rating. While they have similarities with Mortgage-Backed Securities (MBS) in terms of the pool of assets there is a difference – the transfer of mortgages to an Special Purpose Entity (SPE) in a MBS issue means that the issuing bank no longer bears the risk of the loans and the mortgage pool is static. This is in contrast to Covered Bonds where, because the mortgage pool is constantly adjusted to maintain the pool size, the issuing bank bears the credit risk of the mortgages.

Talking Heads

On Fed Hikes Are Done, Stocks Will Rise This Year – Paul Tudor Jones

Fed “could probably declare victory”… not rampantly bullish because I think it’ll be a slow grind”… nflation has been declining for 12 straight months and “that’s never happened before in history”.

On wanting to ‘wait and see’ on rates – Federal Reserve Bank of Atlanta President, Raphael Bostic

“The appropriate policy is really just to wait and see how much the economy slows from the policy actions that we’ve had… I think in the next several months the math is going to work in our favor, and the economy is going to work in our favor… if there is going to be a bias to action, for me there would be a bias to increase a little further, as opposed to cut”

On May rate hike was “close call’ – Chicago Federal Reserve Bank President, Austan Goolsbee

“The thing that made it a close call for me is this big question mark about what is going to be the impact of this on credit conditions”

Top Gainers & Losers – 16-May-23*

Other News

Pemex in Talks to Pay KKR $320 Million for Fuel-Import Terminal

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.