This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

June 13, 2022

US equity markets dropped sharply on Friday again, with the S&P and Nasdaq down 2.9% and 3.5% after the US inflation release. Sectoral losses were led by Consumer Discretionary, down 4.2% followed by IT and Financials, down over 3.7% each. US 10Y Treasury yields soared by 13bp to 3.18%. European markets ended lower too with the DAX, CAC and the FTSE down 3.7%, 2.1% and 2.7% each. Brazil’s Bovespa was down 1.5%. In the Middle East, UAE’s ADX was down 0.2% and Saudi TASI closed 2.2% lower on Sunday. Asian markets have opened on a weak footing today – Shanghai, HSI, STI and Nikkei were down 1.1%, 2.8%, 0.6% and 2.7% respectively. US IG CDS spreads widened 4.1bp and HY spreads were 31bp wider. EU Main CDS spreads were 5.7bp wider and Crossover spreads were 30bp wider. Asia ex-Japan CDS spreads widened 7.6bp.

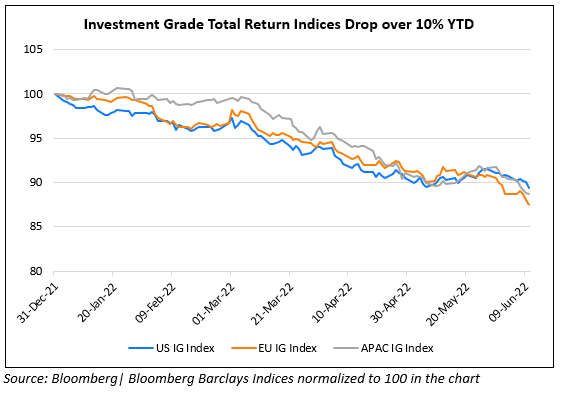

US inflation jumped to another new high with CPI at 8.6% YoY for May with some analysts now stating that a surprise 75bp hike is also possible in its meeting next week. Separately, credit markets across all currencies are down over 10% YTD, its worst fall in decades. In particular, the Bloomberg Euro high grade and aggregate bond indices have eclipsed all prior years’ worst losses.

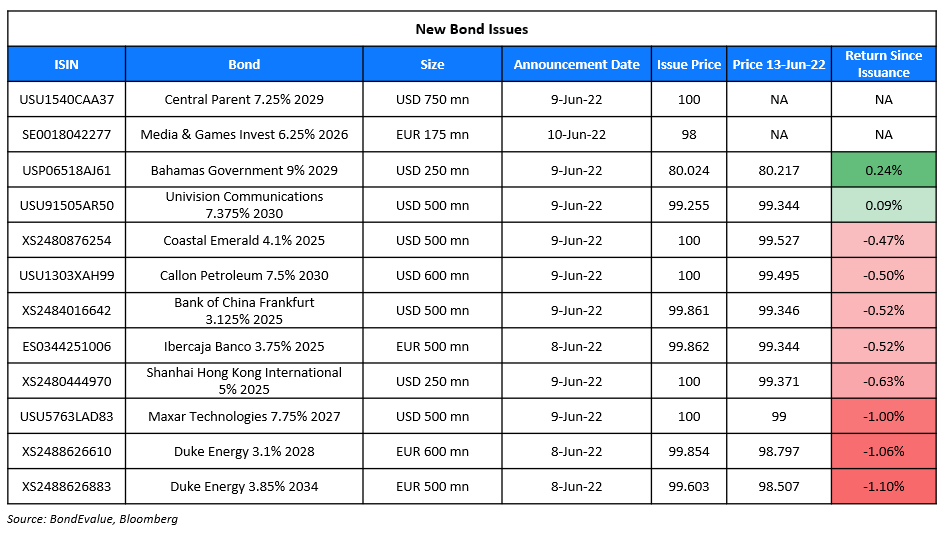

New Bond Issues

New Bonds Pipeline

- Hanwha Energy mandates for $ green bond

- Busan Bank hires for $ Social bond

- Continuum Energy Aura hires for $ Green Bond

Rating Changes

- Fitch Downgrades KWG to ‘B-‘; Maintains Rating Watch Negative

- Moody’s downgrades Zensun’s ratings to B3/Caa1; outlook remains negative

- Fitch Revises Outlook on India to Stable, Affirms at ‘BBB-‘

Term of the Day

Mezzanine Financing

Mezzanine financing is a form of hybrid financing via debt and equity. Here, the lender has the right to convert the debt to an equity stake in the company in the event of default, after senior creditors are paid. Mezzanine financing is typically in the form of unsecured debt and preferred stock and thus has higher risk than secured loans but lower risk than common stock. Mezzanine financing is generally used to fund acquisitions, business expansion etc. to achieve growth objectives.

Talking Heads

On fears of more aggressive interest rate hikes by the Federal Reserve

Jason Pride, CIO for private wealth at Glenmede

“Today’s report should extinguish any pretense that a ‘pause’ in rate hikes will likely be appropriate by the end of summer, as the Fed is clearly still behind the eight ball on bringing inflation under control”

On Investors anticipating too much tightening from the ECB – BlackRock

Michael Krautzberger, overseeing active fixed income strategies

“I would say this is a good opportunity for the ECB to end [its bond-buying programme] and negative rates. But after that I think they may need to slow down. The situation argues for going quite carefully… Hikes will have a massive impact on the property market… Inflation has increased much more than the market expected and much more than I expected.”

On Fed Task Gets Tougher, Putting 75-Basis-Point Hike Back in View

Sarah House, senior economist at Wells Fargo & Co

“Even in these fast-moving times, the Fed is likely to be reluctant to surprise markets, which keeps the chance of a 75 basis-point surprise at next week’s meeting small. However, we could see Chair Powell at the post-meeting press conference more clearly signal that 75 basis-point hikes are on the table for future meetings if we don’t see a let-up in inflation.”

Barclays economists led by Jonathan Millar

“The US central bank now has good reason to surprise markets by hiking more aggressively than expected in June. We realize it is a close call and that it could play out in either June or July. But we are changing our forecast to call for a 75 basis point hike on June 15.”

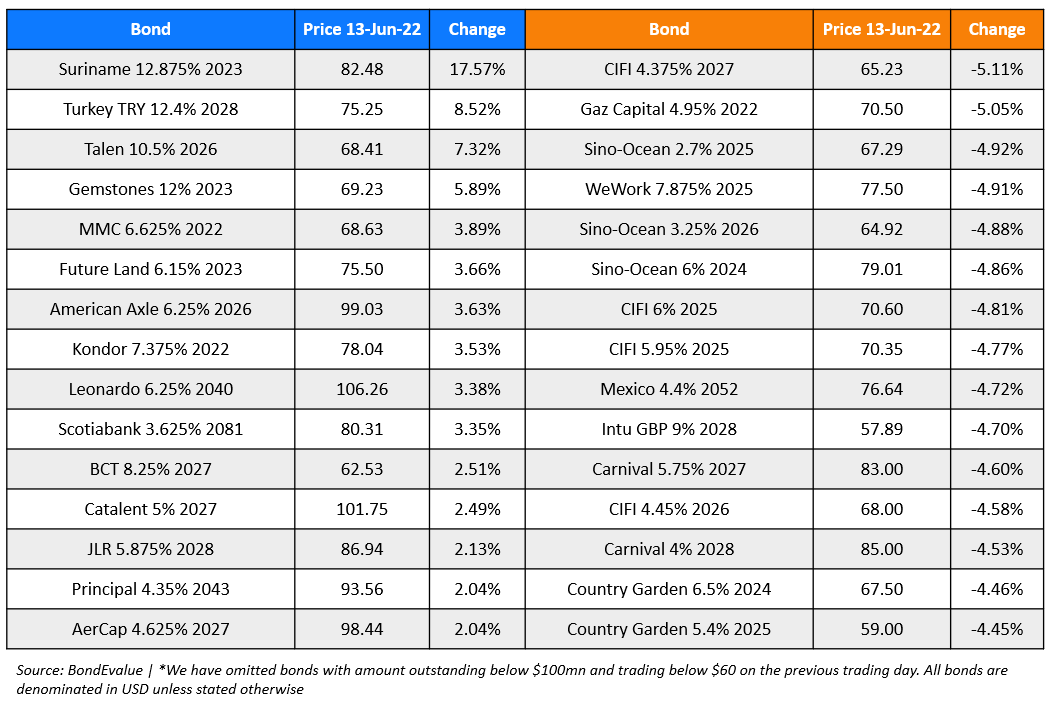

Top Gainers & Losers – 13-June-22*

Other Stories

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.