This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

September 14, 2022

The US 2Y Treasury yield jumped 26bp to 3.79% with the 2s10s yield curve again inverting. US 10Y Treasury yields were 8bp higher at 3.43%. The jump on the short-end occurred after the US inflation data release, which came in higher than forecasts. CPI in August accelerated by 8.3% YoY vs. forecasts of 8.1%. Similarly, Core CPI also came in higher at 6.3% YoY vs. 6.1% expected. Prior to the CPI release, markets were pricing in a 91% probability of a 75bp hike at next week’s FOMC meeting (September 21) and there were no expectations of a move larger than that. However, post yesterday’s inflation data, the probability of a 100bp hike now stands at 38% as per CME data. Equity markets took a beating with the S&P and Nasdaq tanking 4.3% and 5.1% respectively – its biggest single day loss since June 2020. US IG CDS spreads widened 6.6bp and US HY spreads widened 9.6bp.

European markets slid with the DAX, CAC and FTSE down by 1.6%, 1.4% and 1.2% respectively. EU Main CDS spreads widened 5bp and Crossover spreads were 21.9bp wider. Brazil’s Bovespa ended lower 2.3%. In the Middle East, UAE’s ADX and Saudi TASI ended up 0.6% and 0.5% respectively. Asian equity markets have opened broadly negative, echoing the bleak sentiment globally, down ~1% today. Asia ex-Japan CDS spreads were wider by 6.4bp.

IBF-STS Course on Digital Assets | 29 Sep 2022 (In-person in Singapore)| 70/90% Funding

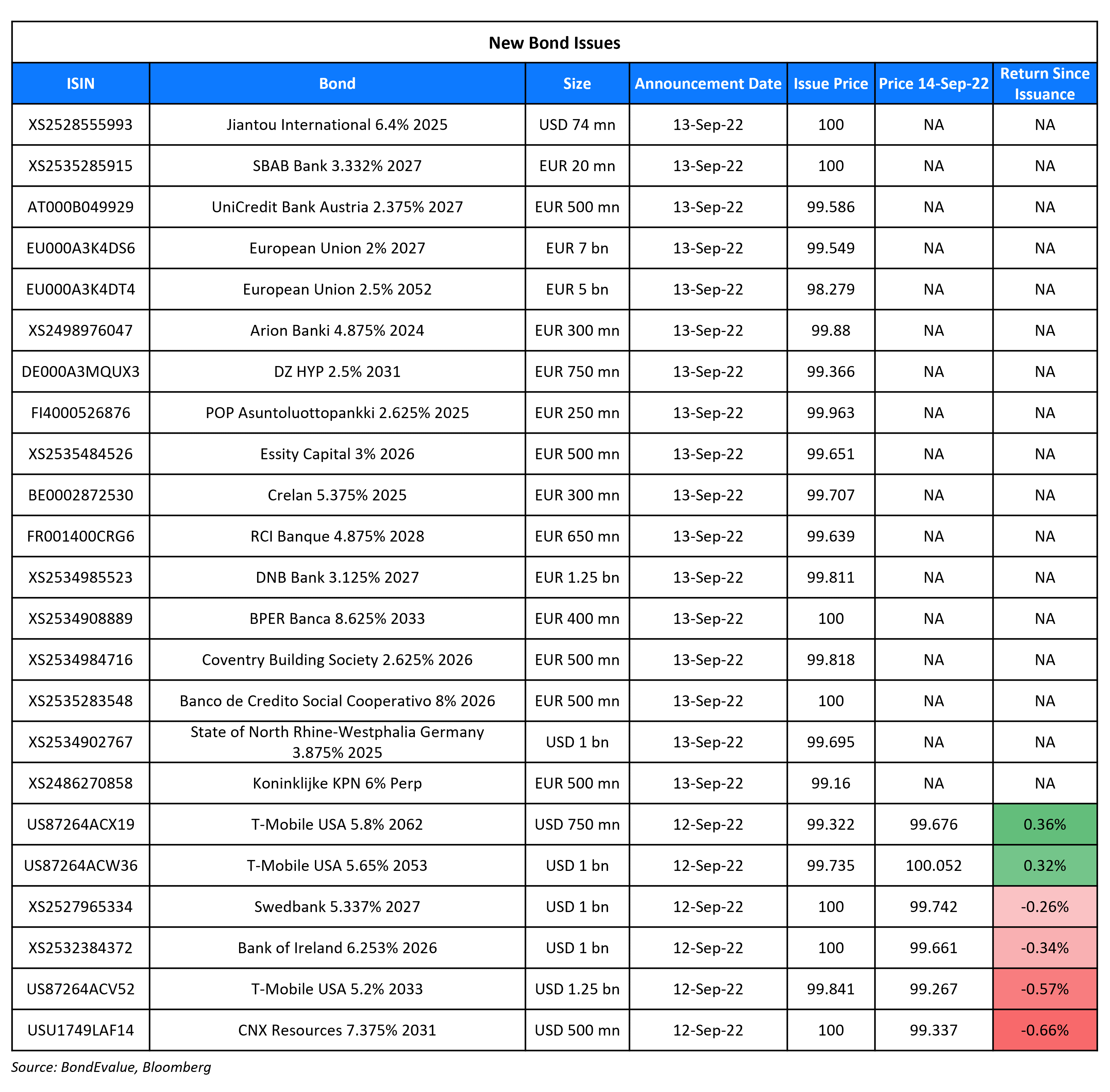

New Bond Issues

New Bonds Pipeline

- Ganzhou Urban Investment Holding Group hires for $ bond

- Aozora Bank hires for $ 3Y Green bond

- NH Investment hires for $ 3Y and/or 5Y Green bond

Rating Changes

Term of the Day

Consent Solicitation

Consent solicitation is an offer by the issuer to change the terms of the security agreement. These are applicable for changes to bonds or shares issued and can range from distribution payment changes and covenant changes in bonds to changes in the board of directors with regard to equities.

Talking Heads

On 100 bps Fed hike in September as speculation rises – Nomura Analysts

“The Federal Open Market Committee, the Federal Reserve’s policy-setting committee, is likely to raise its short-term interest rate target by a full percentage point at its policy meeting next week, because of the emergence of upside inflation risks… With the latest data, we believe those risks are starting to materialize via higher measured inflation across a broad range of goods and services.”

Vincent Mortier, CIO of Amundi Group

“Bonds had been hit by a perfect storm of rising inflation and interest rates that had pushed yields higher, but that the outlook was shifting as recession risks mount…Markets are not totally pricing in recession risks, which are looming, in particular in Europe…We believe that when the recession risks start to materialise, central banks will act to make sure long term rates are not drifting up too much.”

Ken Taubes, CIO of Amundi U.S

“U.S. Treasuries do not have much more downside…Long-rates are near a peak and that is one reason why we have turned more positive.”

On Bond Traders Relishing the Idea of Fed Rates Above 4% as a Chance to Get Yield

Mohit Mittal, a fund manager at PIMCO

“It has definitely been a tough year across fixed income…it’s best to wait until the Fed gets to 4% and then add shorter maturity exposure in high-quality credit and floating-rate notes.”

Gargi Chaudhuri, head of iShares investment strategy for the Americas at BlackRock

”The recent surge in Treasury yields has created lucrative trading opportunities…[my] highest conviction trades through the end of the year are to be in front-end, high-quality credit.”

Kerrie Debbs, CFP at Main Street Financial Solutions

“[People] shouldn’t expect the lofty equity average returns that persisted before the pandemic. …previously boring choices like certificate of deposits are again worth a look and… [it is worth] thinking about adding more short-term bonds — and holding them to maturity… People over past years had become overly anchored in equities given the high returns, but now in this era of higher rates — for longer — they are going to be less satisfied.”

On Wall Street Debating the Fed’s Next Rate Move

Tom Di Galoma, MD at Seaport Global.

“The Fed will want to follow what the market expects and the market is really expecting a 75 basis points move – so that’s what the Fed will do.”

Ian Shepherdson, Chief Economist at Pantheon Macroeconomics

“Eleven Fed officials have made it very clear that they will not slow the pace of rate hikes until they see convincing evidence that core inflation pressure is easing on a sequential basis. These data mean that the chance of a 50bp hike next week has gone…But the 20% chance of a 100bp hike now priced-in looks over the top.”

Andrew Lekas, head of FICC trading at Old Mission Capital

“Oddly enough, I think the market might rally…They want to see the Fed take things seriously on the inflation front, and the sooner we get to the end of these hikes the better…The knee-jerk reaction is probably lower in all risk assets, and there’s the obvious funding impact on anyone who is using leverage, but for the medium term health of the market I think 100 might make sense.”

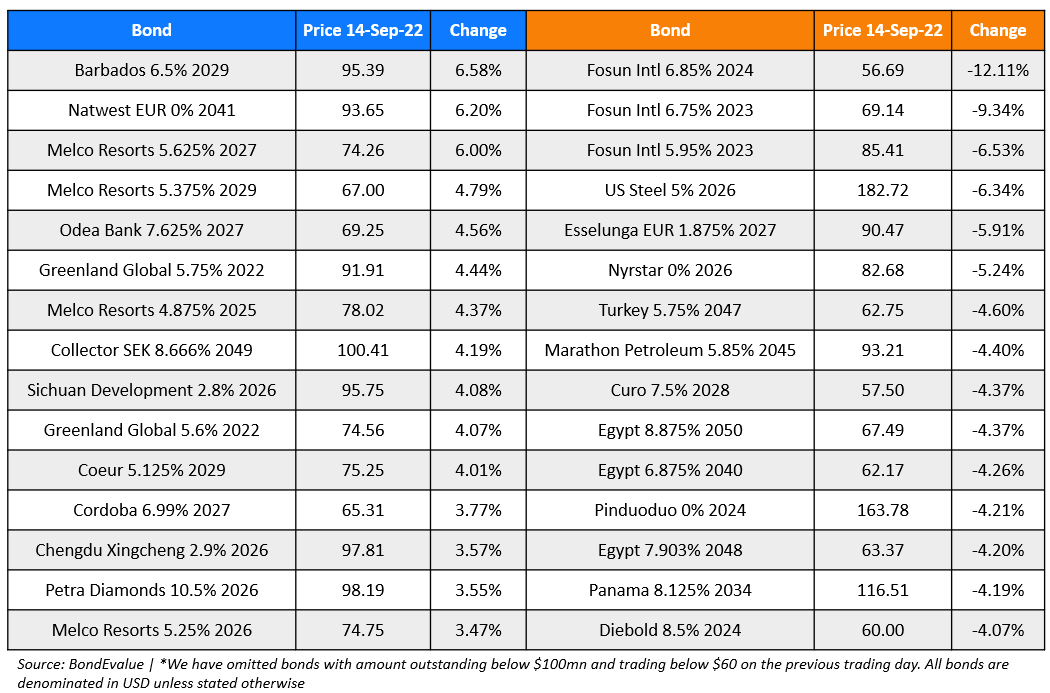

Top Gainers & Losers – 14-September-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.