This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

September 16, 2022

US 10Y Treasury yields were 5bp higher at 3.45%. The 5Y benchmark yield rose 7bp to 3.67%. The curve bear flattened with the 5s30s yield curve inverting by the most since 2000 to -20bp. With the spike in short-term rates, US 3m LIBOR was up 19bp. US equity markets moved lower on Thursday with S&P and Nasdaq down 1.1% and 1.4% respectively, suggesting a likely dead cat bounce on Wednesday. US IG CDS spreads widened by 3.9bp and US HY spreads were 26.3bp wider. US retail sales rose by 0.3% in August against estimates ranging from a -0.5% decline to a 0.5% increase. Analysts note that the print reflected a moderation in demand for goods, especially discretionary goods. July’s data was revised lower to -0.4%. Weekly jobless claims also fell by 5k to 213k.

European equity markets were mixed and the credit markets saw EU Main CDS spreads widen 1.8bp and Crossover spreads move 13.8bp higher. Asian credit markets echoed global sentiment with the Asia ex-Japan CDS spreads widening 2bp. Asian equity markets have opened broadly negative today, down ~0.5%. China posted strong economic numbers – Industrial output rose 4.2% in August, the fastest since March vs. an estimate of 3.8%. Retail sales increased 5.4% YoY, the highest in six-months and more than expectations of 3.5%. For the period from January-August, fixed asset investments rose by 5.8% vs. estimates of 5.5%. Meanwhile, Sri Lanka’s economy contracted by 8.4% in Q2 as the island nation continues to face a severe financial crisis including fuels, fertilizers and forex shortages.

IBF-STS Course on Digital Assets | 29 Sep 2022 (In-person in Singapore)| 70/90% Funding

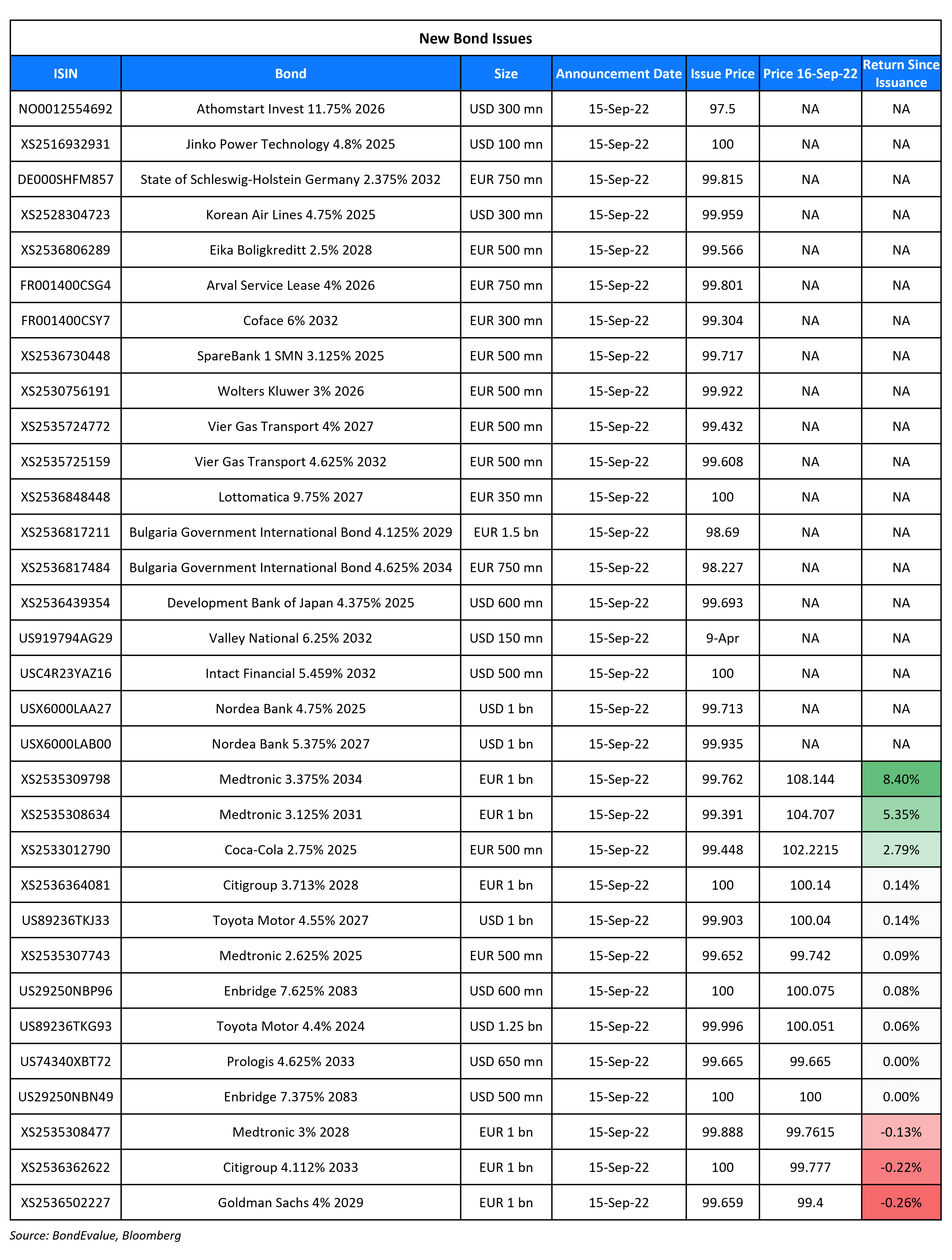

New Bond Issues

- Shaoxing Shangyu State-owned Capital Investment and Operation $ 3Y at 5.6% area

- XMXYG $ 3Y at 6.1% area

Citigroup raised €2bn via a two-tranche deal. It raised

- €1bn via a 6NC5 green bond at a yield of 3.713%, 20bp inside initial guidance of MS+145bp area. The bonds received orders over €2.2bn, 2.2x issue size. Proceeds will be used to finance assets or projects that meet the issuer’s Green Bond Eligibility Criteria. The new bonds are priced at a new issue premium of 16.3bp vs. its existing 1.625% 2028s that yield 3.55%. If not called by the optional redemption date of 22 September 2027, the coupon resets to the 3M Euribor plus a margin of 125bp.

- €1bn via a 11NC10 bond at a yield of 4.112%, 15bp inside initial guidance of MS+175bp area. The bonds received orders over €1.95bn, ~2x issue size. If not called by the optional redemption date of 22 September 2032, the coupon resets to 3M Euribor plus a margin of 160bp.

The senior unsecured bonds have expected ratings of A3/BBB+/A.

Goldman Sachs raised €1bn via a 7Y bond at a yield of 4.057%, 20bp inside initial guidance of MS+180bp area. The senior unsecured bonds have expected ratings of A2/BBB+/A, and received orders over €2.1bn, 2.1x issue size. Proceeds will be used for general corporate purposes.

Private Department of Sheikh Mohamed Bin Khalid al-Nahyan (PD) raised $300mn via a 3Y sukuk at a yield of 8.75%, 12.5bp inside initial guidance of 8.875% area. The bonds have expected ratings of B+, and received orders over $660mn, 2.2x issue size.

Korean Air raised $300mn via a 3Y bond at a yield of 4.765%, 40bp inside initial guidance of T+130bp area. The senior unsecured bonds have expected ratings of Aa2/AA/AA-, and received orders over $1bn, 3.3x issue size. The bonds are issued by Korean Air Lines and guaranteed by Korea Development Bank.

New Bonds Pipeline

- Jinko Power hires for $ Credit Enhanced Green bond

- Aozora Bank hires for $ 3Y Green bond

- Tianjin Binhai New Area Construction & Investment hires for $ bond

- NH Investment hires for $ 3Y and/or 5Y Green bond

Rating Changes

- Fitch Downgrades Sino-Ocean to ‘BB’; Remains on Rating Watch Negative

- Moody’s downgrades CIFI’s ratings to B1/B2; outlook negative

- China SCE Group Downgraded To ‘B-‘ On Weakening Sales And Liquidity; Outlook Negative

- Fitch Downgrades El Salvador to ‘CC’; Removes from UCO

Term of the Day

Dead Cat Bounce

Dead cat bounce is a market jargon used to denote a short-lived bounce back in the price of an asset class (stocks, bonds etc.) or an index after a severe prolonged longer-run drop. Reasons for such a move could include prices reaching certain support levels as some traders clear their short positions.

Talking Heads

“My guess is that if they want to securely control inflation, they’re going have to raise rates further than that. But that’s not a decision they need to make right now… It was very clear that doing 75 basis points, which is what the Fed has now said it’s going to do next week, is better than doing only 50 basis points. And I’m sure they’re going have to continue to raise interest rates.

On worries about ‘generalized stagflation’ in global economy – World Bank’s Gill

“Six months ago we were really concerned about a slowing recovery and very high prices of some commodities, and now I think we are much more concerned about a generalized stagflation, which brings back really bad memories of the mid-1970s and the lost decades.”

On World Bank seeing rising risk of global recession in 2023

World Bank President David Malpass

“Global growth is slowing sharply, with further slowing likely as more countries fall into recession… moderate hit to the global economy over the next year could tip it into recession”.

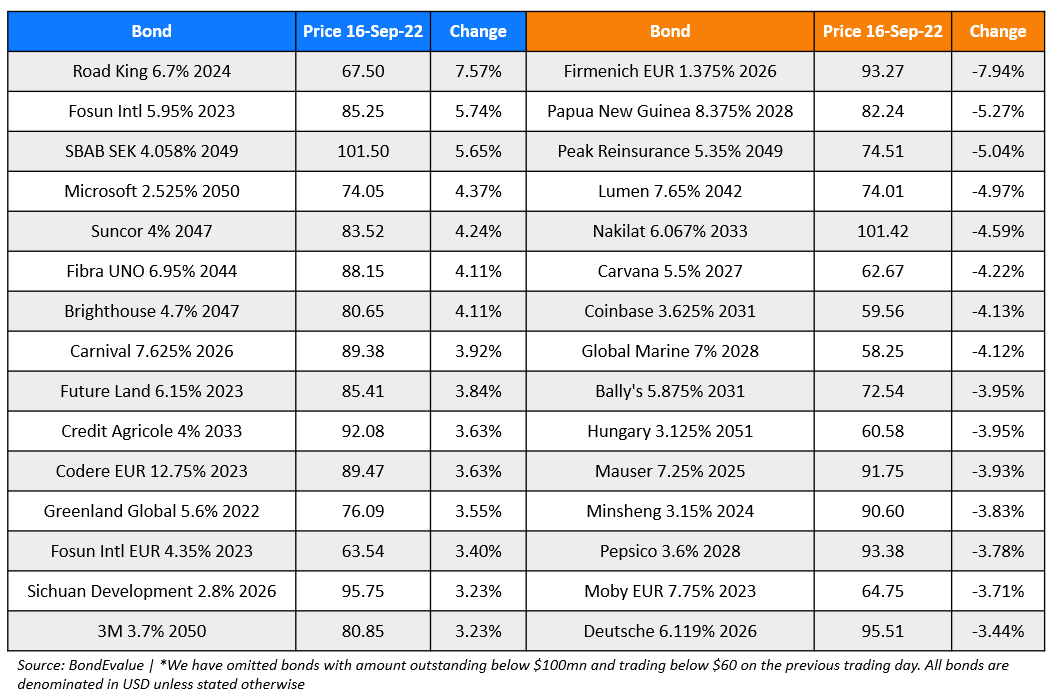

Top Gainers & Losers – 16-September-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.