This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

HSBC, Indonesia Launch $ Bonds; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

March 22, 2022

US equity markets erased early gains with the S&P closing flat and Nasdaq down 0.4%. Sectoral gains were led by Energy, up 3.8% while losses were led by Consumer Discretionary and Communication Services, down over 0.8% each. In a speech to the National Association for Business Economics, Fed Chair Jerome Powell said that he would be ready for more aggressive rate hikes if needed (scroll down to Talking Heads for details). The hawkish comments saw the curve bear flatten as yields on the short-end of curve rose more than the long end – The 2Y jumped from 1.93% to 2.17%, 5Y from 2.15% to 2.37%, 10Y from 2.15% to 2.33% and the 30Y from 2.43% to 2.56%. Post last week’s FOMC meeting, market participants were pricing in 6 more hikes of 25bp, but after Powell’s comments yesterday, Bloomberg notes that 7.5 more hikes have been penciled in. The 5s30s is at its lowest since 2007 at 19bp and the 2s10s has flattened to 16bp. European markets were mixed – the DAX and CAC were down 0.6% each while FTSE was up 0.5%. Brazil’s Bovespa ended 0.7% higher. In the Middle East, UAE’s ADX was down 0.5% and Saudi TASI was down 0.3% on Sunday. Asian markets have opened with a positive bias – Shanghai, HSI and Nikkei were up 0.1%, 1.3% and 1.5% each while STI was down 0.2%. US IG CDS spreads tightened 1bp and HY spreads were 8.7bp wider. EU Main CDS spreads were 0.7bp wider tighter and Crossover CDS spreads were 34.8bp wider. Asia ex-Japan CDS spreads were 0.6bp tighter.

With the growing interest among investors and professionals in ESG bonds – green bonds, social bonds, sustainable bonds and sustainability-linked bonds – BondEvalue has now enriched its data to include key ESG metrics for ESG bonds on the BondEvalue App. For the product release update, click here

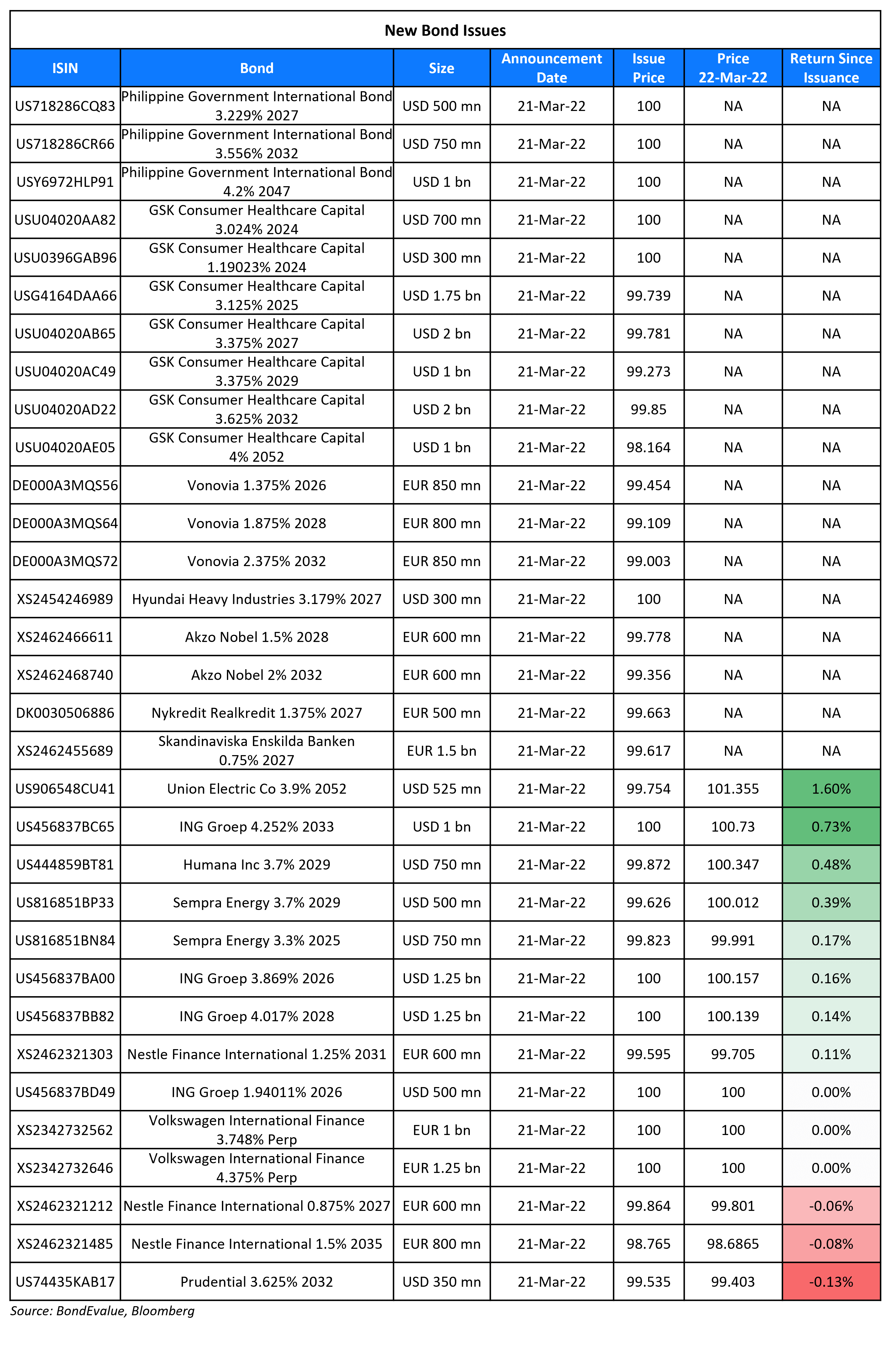

New Bond Issues

- HSBC Holdings $ 11NC10 at T+275bp area

- Indonesia $ 10/30Y at 3.95/4% area

Turkey raised $2bn via a 5.5Y bond at a yield of 8.625%, 25bp inside initial guidance of 8.875% area. The bonds are rated B2/B+ (Moody’s/Fitch). The new bond was priced at a new issue premium of 132.5bp over its 7.25% sukuk due 2027 issued last month, that yielded 7.3% at the time of pricing. The new bonds will offer a new issue premium of 72.5bp over its 6% bonds due March 2027 that yielded 7.9% at the time of pricing.

The Republic of the Philippines raised $2.25bn via a three-trancher. It raised:

- $500mn via a 5Y bond at a yield of 3.229%, 35bp inside initial guidance of T+125bp area

- $750mn via a 10.5Y bond at a yield of 3.556%, 40bp inside initial guidance of T+165bp area

- $1bn via a 25Y sustainability bond at a yield of 4.2%, 50bp inside initial guidance of 4.7% area

The bonds are rated Baa2/BBB+/BBB, in line with the issuer, and received orders over $8bn, 3.6x issue size.. Proceeds from the 5Y and 10.5Y bonds will be used for general budget financing. Proceeds from the sustainability tranche will be used to finance or refinance assets in line with its sustainable finance framework. Vigeo Eiris provided a second party option. The new 10.5Y bond was priced 35.6bp wider to its existing 1.95% bonds due January 2032 that yield 3.2% and the 25Y was priced 12bp wider to its 3.2% bonds due July 2046 that yield 4.08%

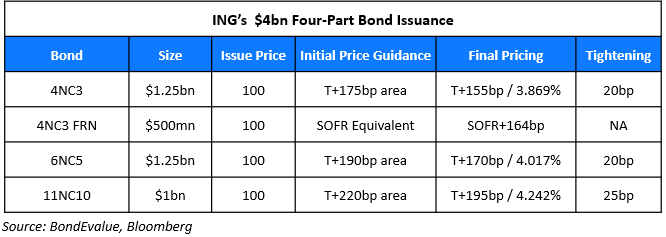

ING Groep raised $4bn via a four-trancher. Details are in the table below:

The bonds are rated Baa1/A-/A+. Proceeds will be used for general corporate purposes.

Prudential raised $350mn via a 10Y bond at a yield of 3.681%, 22bp inside the initial guidance of T+160bp area. The bonds have expected ratings of A2/A. Proceeds will be used to repay outstanding indebtedness. The new bonds are priced 21.1bp wider to its existing 3.125% 2030s that yield 3.47%.

Hyundai Heavy Industries raised $300mn via a 5Y green bond at a yield of 3.179%, 20bp inside initial guidance of T+115bp area. The bonds are rated Aa2 by Moody’s and received orders over $610mn, over 2x issue size. Banks took 49%, asset and fund managers 47%, private banks 3% and pension funds 1%. The bonds are guaranteed by the Korea Development Bank. Proceeds will be used to fund or refinance green projects related to clean transportation, pollution prevention, sustainable water management, renewable energy and energy efficiency.

New Bonds Pipeline

- PTT Global Chemical hires for $ 10Y/30Y bond

- Aluminium Corporation of China hires for $ bond

- Petron hires for $ 7NC4 bond

- Electricity Generating (EGCO) hires for $ 7Y or 10Y bond

Rating Changes

- B&G Foods Inc. Downgraded To ‘B’ From ‘B+’ On Expectations Of Sustained Elevated Leverage; Outlook Stable

- Moody’s affirms Country Garden Baa3 ratings; changes outlook to negative

- Fitch Revises Harley-Davidson’s Outlook to Stable; Affirms IDR at ‘BBB+’

Term of the Day

Debt Trap Diplomacy

Also known as debt diplomacy, this refers to lending money that may not get repaid in order to get concessions, in simple terms. This has particularly been targeted at China where China has lent money cheaply to developing countries that might need help on debt relief, funds for projects involving substantial investments and their like. In return for the loan(s), China asks for concessions – in the case of Sri Lanka, they were forced to hand over control of the Hambantota port project to China for 99 years giving China a key port position and a strategic advantage. Similarly, in exchange for funds, China constructed its first military base in Djibouti.

Explore BondbloX Kristals – a basket of single bonds listed on the BondbloX Exchange following themes such as SGD REIT Perps, USD Bank Perps, and SGD Bank Perps. Avail an introductory discount of $1,000 for every purchase of $100,000 worth of BondbloX Kristals*. Click on the banner above to know more.

Talking Heads

On Powell Ready to Back Half-Point Hike in May If Necessary

Jerome Powell, Federal Reserve Chairman

“If we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so… My colleagues and I may well reach the conclusion that we’ll need to move more quickly and if so we will do so… And if we determine that we need to tighten beyond common measures of neutral and into a more restrictive stance, we will do that as well… The risk is rising that an extended period of high inflation could push longer-term expectations uncomfortably higher.

Derek Tang, an economist at L.H. Meyer

“He doesn’t want to preside over another episode where they were too slow to act. He is trying to get ahead of things. We were leaning toward a half-point hike in June, but this speech could move it to May.”

On Bonds Extend Drop After Fed Sparks One of Worst Days in Decade

Tracy Chen, a portfolio manager at Brandywine Global

“At the end of last week, investors including us were thinking the long-end looks cheap. But our models can’t factor in the uncertainty about inflation from the commodity price shock.”

Thomas Atteberry, First Pacific Advisors

“In recent past cycles the Fed was much more methodical in their hiking cycles, so basically you weren’t getting surprised. Powell adding this optionality and taking the past-cycle predictability off the table makes it just more more volatile and unpredictable. This has made the environment more difficult for fixed-income investors.”

Andrew Hollenhorst, chief U.S. economist at Citigroup Inc

“The Fed has a big constraint now, which is inflation that is just too high now… Fed is fighting against inflation and wants to actually do things that are going to tighten financial conditions… the upcoming round of balance-sheet run off will most likely be anything but ‘watching paint dry’

On Petrobras Hit by Fuel Politics With Subsidies Surging All Over

William Nozaki, Economist

“Finding ways to solve the problem of fuel inflation is among the main discussions we are having at the moment

David Zylbersztajn, Professor at Pontifical Catholic University of Rio de Janeiro

“The consequence of this rhetoric will be a lack of investments and fuel shortages”

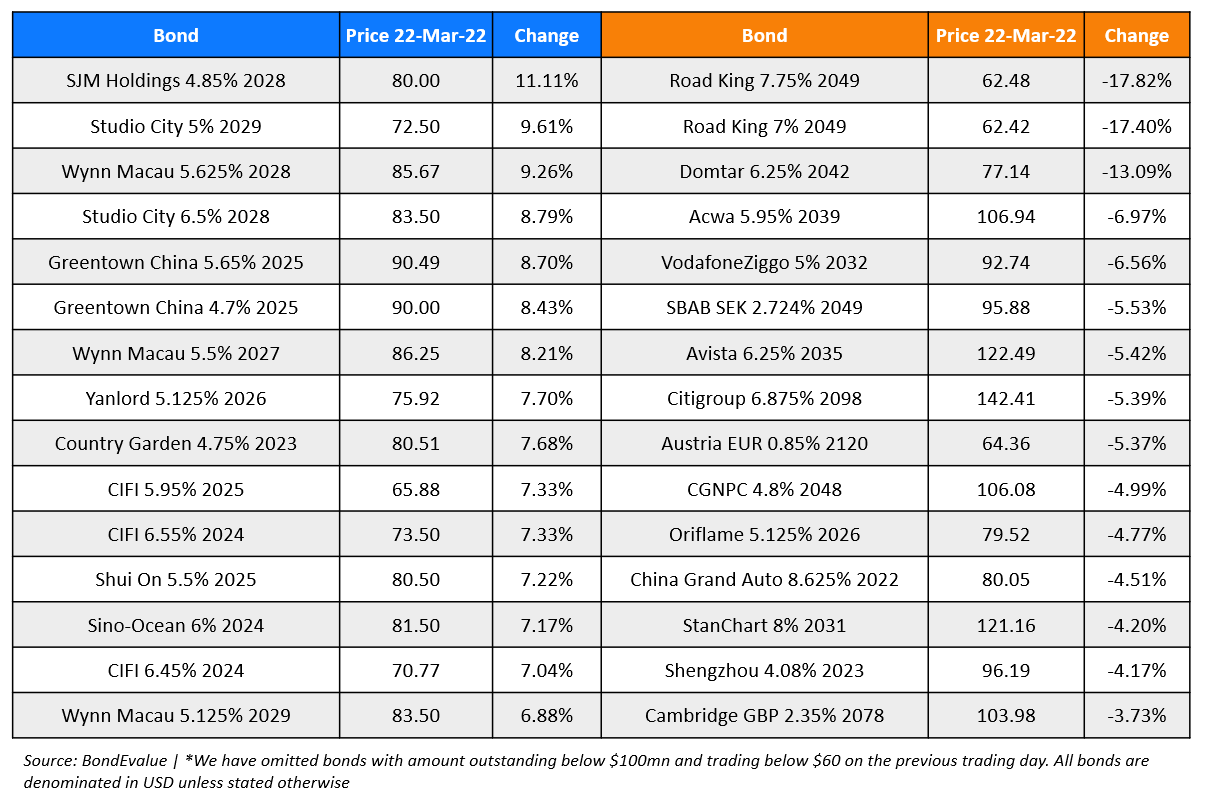

Top Gainers & Losers – 22-Mar-22*

Other Stories

ESR-Reit, ALog Trust unitholders vote in favour of merger to form ESR-Logos Reit

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.