This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Pakistan to Try Renegotiating IMF Loan

May 26, 2022

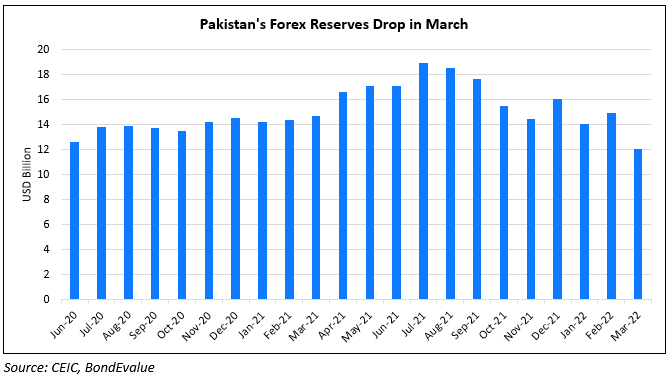

Pakistan’s foreign minister said that he hopes the nation can renegotiate an IMF deal to counter the rise in food and fuel prices. IMF’s $6bn loan program to Pakistan was agreed in 2019 but got stuck after a dispute with the previous government under Imran Khan. At that time, the prior government reintroduced controversial energy subsidies that the IMF had sought to remove. The plan by the new government to renegotiate the deal comes after the country has been struggling to cope with decreasing forex reserves and one of the highest inflation rates in Asia. Some analysts have even sounded a warning of the country defaulting on its foreign debts.

Pakistan’s dollar bonds were trading higher with its 7.375% 2031s up 0.9 points to 63.89, yielding 14.82%

For the full story, click here

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.