This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

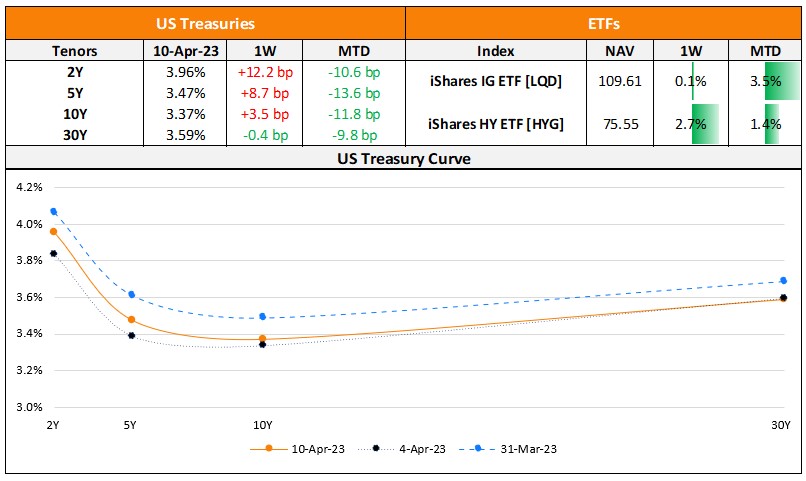

Bond Market News

The Week That Was (03 – 09 April 2022)

US primary markets saw $16.8bn in new deals last week as compared to $20.7bn in new deals a week prior to it. Of the deal volumes, IG issuers raised $9.65bn in new issuances led by GM Financial’s $2.25bn and Micron’s $1.5bn dual-tranchers each. HY saw $7.14bn in new deals led by Cloud Software’s $3.84bn issuance and Ford Motor’s $1.5bn deal. In North America, there were a total of 35 upgrades and 33 downgrades across the three major rating agencies last week. US IG bond funds saw $1.79bn in inflows for the week ended April 5 after $881mn was withdrawn in the week prior to it. HY funds saw $3.77bn in inflows reversing the $2.1bn in withdrawals the week before.

EU Corporate G3 issuance fell slightly to $19.5bn vs. $22.9bn a week prior. Issuance volumes were led by KfW’s $3bn deal and BPCE’s €3bn dual-trancher. Across the European region, there were 24 upgrades and 16 downgrades. The GCC dollar primary bond market saw $4bn in new deals vs. $1.2bn in the week before that, led by Saudi Electricity’s $2bn dual-trancher, followed by Bahrain and CBB International’s $1bn issuances each. Across the Middle East/Africa region, there were 6 upgrades and 2 downgrades across the major rating agencies. LatAm saw $2.25bn in in new deals with Brazil being the sole issuer, as compared to $1.5bn in new deals a week prior to it. The South American region saw 2 upgrades and 4 downgrades across the rating agencies.

The APAC ex-Japan G3 region saw a drop in issuances to just $1.25bn after $6.5bn in new issuances the week prior to it. There were only two deals with REC Ltd raising $750mn and Shinhan Bank raising $500mn. In the APAC region, there was 1 upgrade and 6 downgrades combined across the three rating agencies last week.

-png.png)

Go back to Latest bond Market News

Related Posts:

The Week That Was (Oct 4th – 11th)

October 11, 2021

The Week That Was (27 June – 03 July, 2022)

July 4, 2022

The Week That Was (15 August – 20 August, 2022)

August 22, 2022

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.