This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

The Week That Was (13 – 19 February, 2022)

February 20, 2023

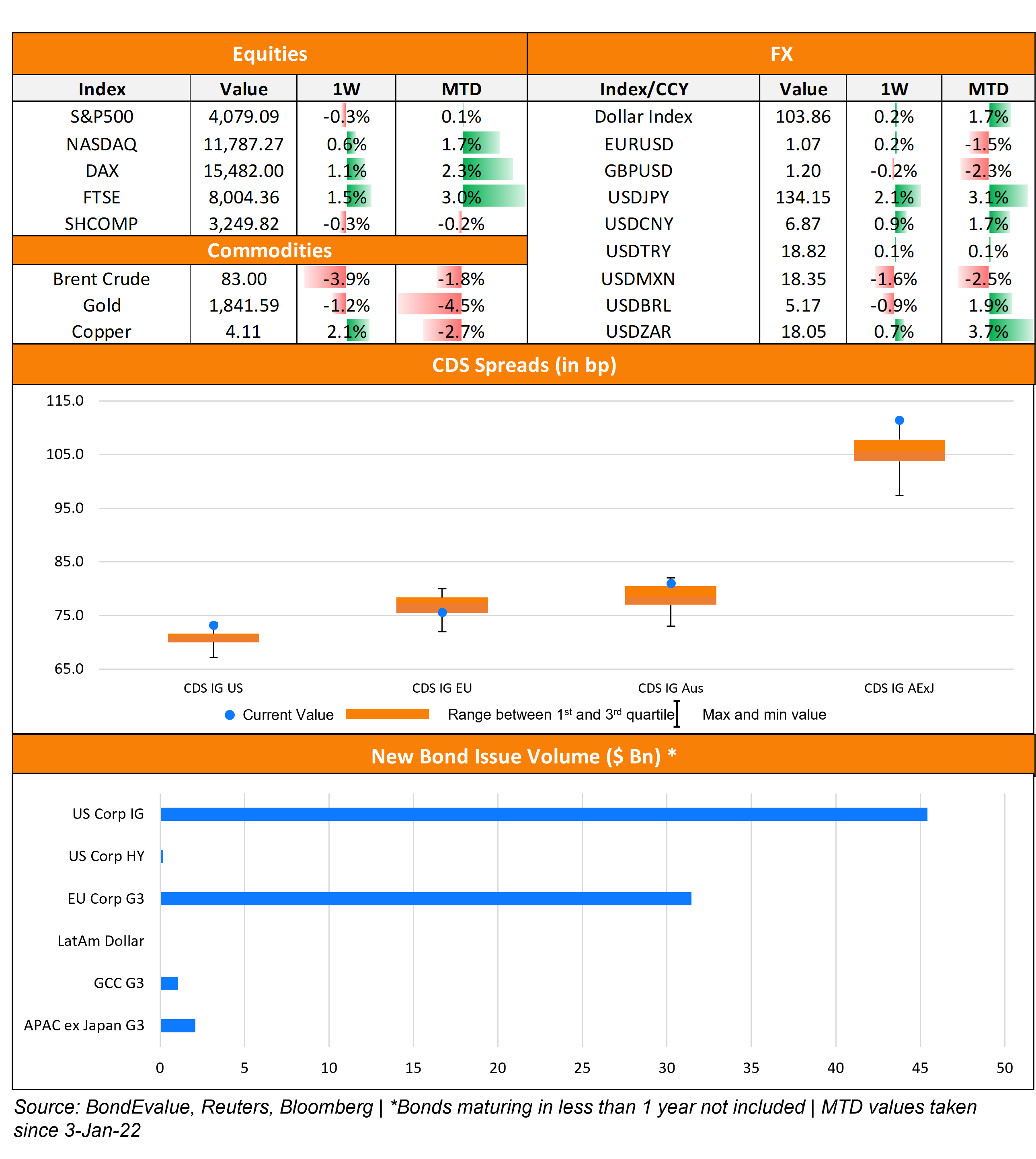

US primary market issuances stood at $45.5bn last week vs. $37.4bn a week prior. IG issuances stood at $45.1bn led by Amgen’s jumbo $24bn eight-part deal, the biggest this year from an issuer, followed by CVS’s $6bn four-trancher. HY issuances stood at a mere $200mn with Vantage Drilling being the sole issuer. In North America, there were a total of 50 upgrades and 57 downgrades across the three major rating agencies last week. As per Lipper data, US IG bond funds saw inflows of $1.2bn in the week ending February 15, adding to the $2.8bn in inflows seen in the week prior. HY bond funds saw $2.8bn of outflows during the week following the prior week’s $871mn in inflows. As per FT, a total of $19bn of inflows have swamped into IG corporate bond funds around the world since the beginning of 2023. This comes after average yields on IG credit have risen considerably over the last year – for example, the average US IG yield has climbed from 3.1% to 5.45% currently during the last one year.

LatAm saw no new deals last week as compared to $1.2bn in new deals a week prior. In South America, there were 4 upgrades and 10 downgrades across the major rating agencies. EU Corporate G3 issuance stood at $29.6bn vs. $45.6bn a week prior. Issuance volumes were led by Credit Mutuel’s €2.5bn two-trancher and BNP Paribas’ €1.8bn dual-tranche issuances. Across the European region, there were 30 upgrades and 23 downgrades. The GCC dollar primary bond market saw $1.1bn in deals vs. $11.1bn in deals the week prior led by Sharjah’s $1bn issuance. Across the Middle East/Africa region, there was 1 upgrade and 25 downgrades across the major rating agencies.

The APAC ex-Japan G3 region saw $2.1bn in issuances vs. $4.96bn in the week before that led by Korea Housing Finance raising $1.3bn via a dual-trancher and Chindata’s $300mn deals. In the APAC region, there were 9 upgrades and 15 downgrades combined across the three rating agencies last week.

Go back to Latest bond Market News

Related Posts:

The Week That Was (Oct 4th – 11th)

October 11, 2021

The Week That Was (27 June – 03 July, 2022)

July 4, 2022

The Week That Was (15 August – 20 August, 2022)

August 22, 2022

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.