This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

The Week That Was (Mar 21 – 27, 2022)

The yield curve continues to flatten further – the 2s10s has now flattened from 38bp in the beginning of the month to 15bp currently. US primary market issuances rose to $32bn vs. $18.5bn in the week prior. Investment grade (IG) corporates once again took the chunk of issuances, with $26.6bn of deals while high yield (HY) issuance stood at $4.3bn. The largest IG deals were led by GSK Consumer Healthcare $8.75bn seven-part offering, and Home Depot’s $4bn four-trancher. In the HY space, Ford Motor’s $1.5bn issuance, followed by Paramount Global and Yum Brands’ $1bn deal each. In North America, there were a total of 20 upgrades and 14 downgrades combined across the three major rating agencies last week. LatAm saw no issuances last week as compared to $762mn in the prior week. In South America, there was no upgrades and 9 downgrades across the major rating agencies. EU Corporate G3 issuances stood at $47bn vs. $31.4bn in the week prior, led by the ING’s $4bn four-trancher, KfW’s €2bn deal and HSBC’s $2bn issuance. Across the European region, there were 65 upgrades and 20 downgrades across the three major rating agencies. The GCC G3 region saw $3bn vs. $100mn in issuances in the week, led by MDGH’s $1.5bn issuance, followed by ADCB and Boubyan’s $500mn deals each. Across the Middle East/Africa region, there were 3 upgrades and no downgrades across the three major rating agencies. APAC ex-Japan G3 issuances stood at $8.6bn vs. $5.96bn led by Philippines‘ $2.25bn triple-trancher, Indonesia’s $1.75bn dual-trancher and PTT Global Chemicals’ $1.3bn two-trancher, . In the APAC region, there were 2 upgrades and 13 downgrades combined across the three major rating agencies last week.

Go back to Latest bond Market News

Related Posts:

The Week That Was (Oct 4th – 11th)

October 11, 2021

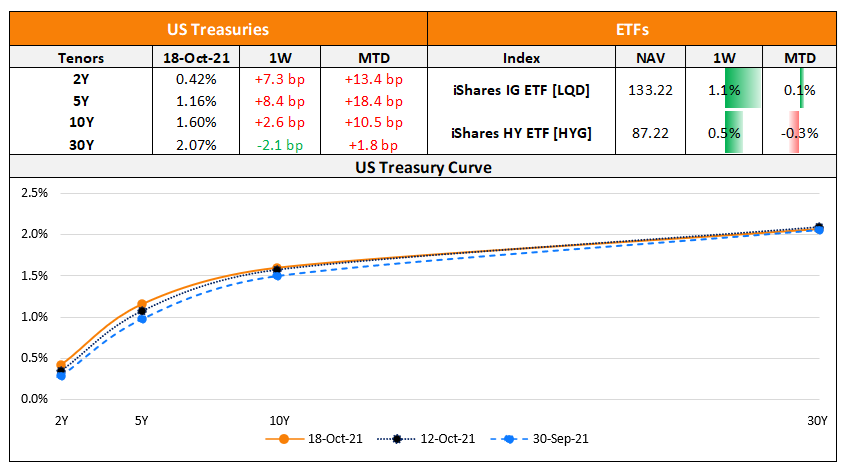

The Week That Was (11 – 17 Oct 2021)

October 18, 2021

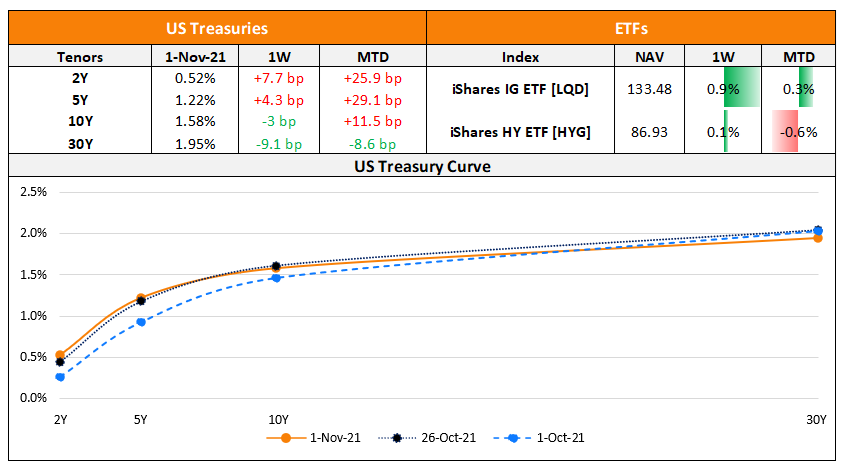

The Week That Was (25 – 31 Oct)

November 1, 2021

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.