This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Turkey Raises $1.5bn via New 2028s at 10%; Deutsche Prices EUR AT1 at 10%; Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

November 8, 2022

US Treasury yields moved higher across the curve led by the long-end with the 10Y and 30Y yields up 7-10bp. The peak Fed Funds rate was unchanged at 5.14% for the June 2023 meeting. Current probabilities of a 50bp hike at the FOMC’s December meeting stand at 57% and that of a 75bp at 43%. In the credit markets, US IG CDS spreads tightened 1.5bp and HY CDS spreads saw an 8.8bp tightening. US equity markets continued to rally with the S&P and Nasdaq up 1% and 0.9% respectively.

European equity markets were broadly positive. EU Main CDS spreads tightened 2.2bp and Crossover spreads tightened 12.9bp. Asian equity markets have opened mixed today. Asia ex-Japan CDS spreads were unchanged after it saw a 20.9bp tightening with Korean credit markets witnessing ease in credit sentiment as insurer Heungkuk Life Insurance Co. reversed its decision to skip the call on its perp, pushing the perp ~20 points higher (scroll down for details).

.jpeg)

New Bond Issues

- Jinan Hi-tech $ 3Y at 7.2% area

-1.png)

Turkey raised $1.5bn via a 6Y bond at a yield of 10%, inside initial guidance of low 10%s. The bonds are rated B3/B (Moody’s/Fitch). The issuance is said to help push Turkey’s borrowing toward its target of $11bn for 2022, given that it had only sold $7.5bn yet. As per Bloomberg citing JPMorgan Index data, the yield premium on Turkey’s debt has narrowed to 494bp over US Treasuries, the lowest in a year and less than half of similar single-B rated sovereign, Egypt. Sergey Dergachev, Senior PM and Head of EM corporate debt at Union Investment Privatfonds said, “Outperformance of Turkish credit has been stellar. Turkish sovereign debt is one of the most liquid high-yield sovereign credits out there and is relatively easy to trade. It seems to me that the transmission of high inflation and the central bank policy to credit spreads is diminishing”. Turkey’s new 6Y bond was priced at a new issue premium of 64bp over its existing 6.125% bonds due October 2028 that currently yield 9.36%.

Deutsche Bank raised €1.25bn via a PerpNC5.5 AT1 at a yield of 10%, 50bp inside initial guidance of 10.5% area. The subordinated perps are rated Ba2/BB-. The coupon is fixed until the first call and reset date of 30 April 2028. If not redeemed, the coupon resets then and every five years thereafter to the 5Y MS plus a spread of 694bp. A trigger event would occur if the group’s consolidated CET1 ratio falls below 5.125%. As of the quarter ended September 2022, Deutsche’s CET1 ratio stood at 13.3%. The new bonds were priced 93bp tighter to its existing senior unsecured EUR 6.75% Perp callable in October 2028 that currently yields 10.93%.

Lloyds Banking Group raised $1bn via a 11NC10 Tier 2 bond at a yield of 7.953%, 25bp inside initial guidance of T+400bp area. Proceeds will be used for general corporate purposes. The new bonds are priced at a new issue premium of 79bp vs. its existing 4.976% 2033s callable in August 2032 that currently yield 7.13%.

HSBC raised ~$2.4bn equivalent via a multi-currency issuance. It raised €1.25bn ($1.25bn) via a 10NC5 senior unsecured bond at a yield of 6.364%, 25bp inside initial guidance of MS+210bp area. It also raised £1bn ($1.15bn) via a 12NC7 senior unsecured bond at a yield of 8.201%, 25bp inside initial guidance of MS+210bp area. Both the tranches are rated Baa1/BBB/A-. The euro-tranche received orders over €2.9bn, 2.3x issue size while its sterling-tranche saw £2.75bn in orders, 2.75x issue size.

ING Groep raised €2.25bn via a two-trancher deal. It raised €1.25bn via a 5NC4 senior unsecured bond at a yield of 4.903%, 25bp inside initial guidance of MS+210bp area. It also raised €1bn via a 11NC10 senior unsecured bond at a yield of 5.281%, 25bp inside initial guidance of MS+240bp area. The bonds are rated Baa1/A-/A+ (Moody’s/S&P/Fitch) and received orders over €5bn, 2.2x issue size.

Oracle raised $7bn via a four-trancher deal. -1.png)

The senior unsecured bonds are rated Baa2/BBB/BBB+. Proceeds will be used to prepay its borrowings under the bridge facility which was used to help fund its acquisition of medical-records systems provider Cerner Corp.

New Bonds Pipeline

- Double Dragon hires for tap of $130mn 7.25% 2025s

- Korea Investment & Securities hires for $ Green bond

Rating Changes

- Mongolian Mining Corp. Downgraded To ‘CC’ On Proposed Cash Tender Offer; Outlook Negative

- Fitch Downgrades VTR’s Ratings to ‘B’; Rating Watch Negative

- Oracle Corp. Outlook Revised To Stable From Negative On New Financial Policy; Ratings Affirmed; New Notes Rated ‘BBB’

- Anheuser Busch Outlook Revised To Positive On Solid Deleveraging Prospects; ‘BBB+/A-2’

Term of the Day

Coupon Step-up

Coupon step-up refers to a feature seen in certain bonds wherein the coupon increases (steps-up) either as per a predefined schedule or upon the occurrence of an event. Coupon step-ups can either be a single step-up or multiple step-ups through the life of the bond. A commonly seen step-up is for perpetual bonds, wherein the coupon increases in the event that the bond is not called on its first call date (assuming the reset date is the same as the first call date). However, not every bond’s coupon step-up happens if the bond is not called on its first call date, as it depends on the covenant structure of the bond.

In Mapletree’s SGD 3.95% Perp’s case, the coupon step-up would only happen in November 2027 although its first call date is in November 2022.

Talking Heads

On Is ‘Not Touching’ High-Yield Bonds Just Yet – DoubleLine Capital’s Deputy CIO Jeff Sherman

“You’re talking about a 9-handle yield on junk bonds — there’s things in the investment-grade market that have similar yields. I’m not touching high-yield today. We think there’s been too much of this belief in a Fed pivot, the risk rally we saw in equities, so it’s looking a little rich again… When you dig down in credit quality, we think if you’re going to do that, that should be your replacement for equity today. The downside is already priced into a lot of these markets.”

On Citi, Morgan Stanley End Bearishness on Emerging Currencies

Citigroup

Due to calming of the Treasury market and the nearing of an end to the Fed hiking cycle , “This is why we are bringing our overweight dollar stance back to neutral in our model portfolio. We are now positioned flat on the currency front in our model portfolio”

Morgan Stanley

“The relatively mature phase of the Fed hiking cycle and relatively fair pricing for US terminal rate expectations suggest poor risk-reward in continuing to build long dollar positions. Additional emerging-market currency weakness from current levels looks unlikely”

On Looming UK Bond Glut This Week Being the ‘Real Test’ for Investors

Gordon Shannon, a portfolio manager at TwentyFour Asset Management

“When the gilt market is tested, it’s clear that it’s still not totally not confident about what’s been happening. There’s less actual buyers for medium-dated gilts versus the short end. So fundamentals are coming to the fore”

Antoine Bouvet, a rates strategist at ING Groep NV

It’s “not a great look” for the gilt operation

Imogen Bachra, head of UK rates strategy at NatWest Markets

“It’s the heaviest week of supply in some time”

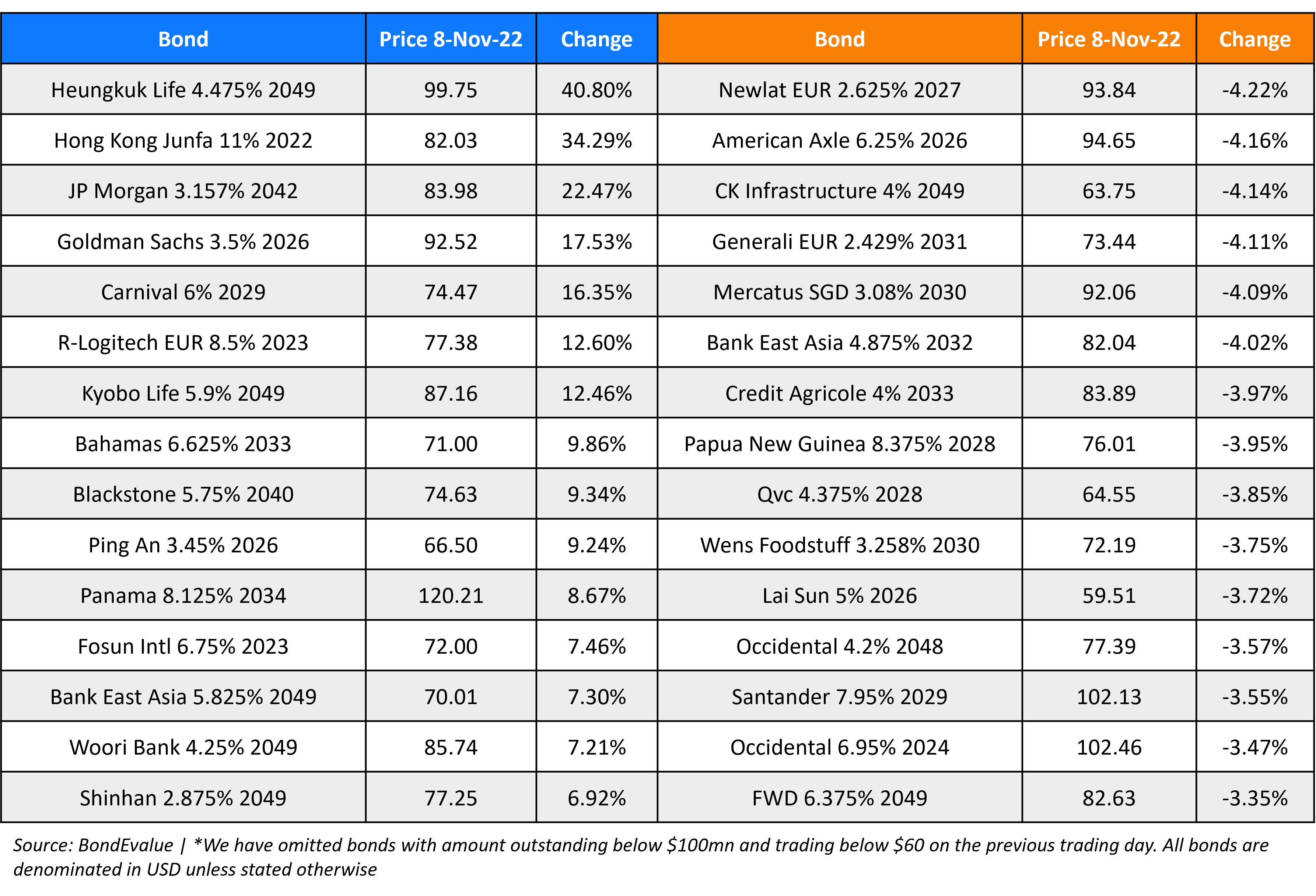

Top Gainers & Losers – 08-November-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.