This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

5 New $ Deals Launched incl. SBI, SIA; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers & Losers

January 12, 2022

US equity markets saw strong gains with the S&P and Nasdaq up 0.9% and 1.4% respectively. Energy led the gainers, up 3.4% with IT, Materials, Consumer Discretionary and Communication Services up over 1% each. US 10Y Treasury yields were down 2bp to 1.74%. European markets were also higher with the DAX, CAC and FTSE up 1.1%, 1% and 0.6% respectively. Brazil’s Bovespa was up 1.8%. In the Middle East, UAE’s ADX was flat while Saudi TASI was up 1.5%. Asian markets have opened in the green – Shanghai, HSI, STI and Nikkei were up 0.4%, 2.1%, 0.1% and 1.9% respectively. US IG CDS spreads were 0.8bp tighter and HY CDS spreads also tightened 0.8bp. EU Main CDS spreads were 1bp tighter and Crossover CDS spreads were 6bp tighter. Asia ex-Japan CDS spreads tightened 0.6bp.

The World Bank its global GDP forecasts noting that it may expand 4.1% in 2022 vs. 4.3% anticipated earlier due to Covid flare-ups, diminished policy support, and supply-chain bottlenecks.

New Bond Issues

- State Bank of India $ 5Y formosa at T+130bp area

- Singapore Airlines $ 7Y at T+210bp area

- China Chengtong HK $ 3/5Y at T+150/175bp area

- Woori Bank $ 5Y sustainability at T+90bp area

- Mitsui & Co $ 5Y at T+90bp area

.png)

Panama raised $2.5bn via a two-tranche deal. It raised:

- $1bn via a 11Y bond at a yield of 3.298%, 30bp inside the initial guidance of T+185bp area

- $1.5bn via a 40Y bond at a yield of 4.534%, 25bp inside the initial guidance of T+270bp area

The bonds were unrated. Proceeds will be used for general budgetary purposes.

.png)

SocGen raised $5bn via a five-tranche deal.

MUFG raised $2.3bn via a two-tranche deal. It raised:

- $1.3bn via a 6NC5 bond at a yield of 2.341%, 22bp inside initial guidance of T+105bp area

- $1bn via a 11NC10 bond at a yield of 2.852%, 20bp inside initial guidance of T+130bp area

Both bonds have expected ratings of A1/A–/A–. Proceeds will be used to fund the operations of MUFG Bank and Mitsubishi Trust and Banking Corp through loans that are intended to qualify as internal TLAC debt.

Agricultural Bank of China raised $700mn via a two-tranche deal. It raised:

- $400mn via a 3Y bond at a yield of 1.578%, 35bp inside the initial guidance of T+70bp area

- $300mn via a 5Y green bond at a yield of 2.02%, 38bp inside the initial guidance of T+85bp area

Both bonds have expected ratings of A1 (Moody’s). The 3Y bond received orders over $950mn, 2.4x issue size, while the 5Y green bond received orders over $950mn, 3.2x issue size. Proceeds for the 3Y tranche will be used for general corporate purposes, while proceeds for the 5Y green tranche will be used to finance and/or refinance green projects. For the 3Y bond, banks and financial institutions were allocated 97%, and asset managers and fund managers 3%. Asia bought 91% and EMEA 9%. For the 5Y green bond, banks and private banks received 74%, pensions, insurers and agencies 22%, and asset managers and fund managers 4%. Asia bought 87% and EMEA 13%. The new 3Y bonds are priced 17.8bp wider to its existing 0.7% Jun 2024s that yield 1.4%.

SF Holding raised $700mn via a two-part tap issuance. It raised:

- $400mn via a tap of its 2.375% 2026s at a yield of 2.737%, 40bp inside the initial guidance of T+160bp area

- $300mn via a tap of its 3.125% 2031s at a yield of 3.374%, 37.5bp inside the initial guidance of T+195bp area

The 2.375% 2026s received orders over $2.6bn, 6.5x issue size. Banks and financial institutions received 27%, fund managers and asset managers 56%, and insurers, sovereign wealth funds and private banks 17%. Asia took 97% and EMEA 3%. The 3.125% 2031s received orders over $1.2bn, 4x issue size. Banks and financial institutions were allocated 38%, fund managers and asset managers 44%, and insurers 18%. Asia took 98% and EMEA 2%. Both bonds are rated A3/A-/A-. The 2.375% 2026 tap is priced at a new issue premium of 10.7bp over its initially issued bond that yields 2.63%. The 3.125% 2031 tap is priced at a new issue premium of 5.4bp over its initially issued bond that yields 3.32%.

HKT Group raised $650mn via a 10Y bond at a yield of 3.009%, 30bp inside initial guidance of T+155bp area. The bonds have expected ratings of Baa2/BBB (Moody’s/S&P), and received orders over $1.2bn, 1.8x issue size. Proceeds will be used for general corporate needs, including debt repayment. The bonds are issued by HKT Capital No 6, a wholly owned subsidiary of HKT. Fund managers and insurance companies took 70%, banks 27% and private banks 3%. Asia accounted for 94% and EMEA 6%.

Link REIT raised $600mn via a 10Y bond at a yield of 2.86%, 30bp inside initial guidance of T+140bp area. The bonds have expected ratings of A2/A (Moody’s/S&P), and received orders over $1.1bn, 1.8x issue size. Proceeds will be used for general corporate purposes. The bonds are issued by indirect wholly owned subsidiary The Link Finance (Cayman) 2009 and guaranteed by The Link Holdings, Link Properties and HSBC Institutional Trust Services Asia. Fund managers and insurers took 60%, banks 36% and private banks and others 4%. Asia accounted for 99% and Europe 1%.

Beijing Gas Group raised $500mn via a 3Y green bond at a yield of 1.97%, 40bp inside initial guidance of T+115bp area. The bonds have expected ratings of A3/A (Moody’s/Fitch), and received orders over $3bn, 6x issue size. The proceeds from the Hong Kong-listed sale will be used for financing and/or refinancing green projects. The bonds are issued by Beijing Gas Singapore Capital Corp and guaranteed by Beijing Gas Group. Asset/fund managers took 43%, banks and financial institutions 54%, sovereigns 2% and private banks and others 1%. APAC bought 93% while EMEA took 7%.

Guangzhou Development District raised $490mn via a 5Y green bond at a yield of 2.85%, 45bp inside initial guidance of 3.3% area. The bonds have expected ratings of Baa1/BBB+ (Moody’s/Fitch), and received orders over $1.13bn, 2.3x issue size. Proceeds will be used to finance and/or refinance eligible green projects. Banks received 79%, fund managers, asset managers and hedge funds 18%, and insurers and others 3%. Asia Pacific investors bought 99% and EMEA 1%.

Zhenjiang State-owned Investment Holding raised $150mn via a 364-day bond at a yield of 1.9%, 8bp inside initial guidance of 1.98% area. The bonds are unrated. The proceeds will be used to repay debt, as well as for working capital and other general corporate purposes. The bonds are issued by HK Onlink Technology, supported by a letter of credit from Bank of Jiangsu Zhenjiang branch, and has a keepwell provision from Zhenjiang State-owned Investment.

Yancheng High-Tech Zone Investment Group raised $100mn via a 3Y bond at a yield of 2%. The bonds are unrated. Proceeds will be used for general corporate purposes and/or refinancing offshore loans. The bonds are supported by a letter of credit from Bank of Shanghai Nanjing branch.

New Bonds Pipeline

- Petron hires for $ 7NC4 bond

- Mitsui Fudosan hires for $ 300 mn 10Y green bond

- CCB hires for $ 10NC5 tier 2 bond

- JY Grandmark hires for $ bond

- JSW Infrastructure hires for $ 7Y SLB bond

- ADB marketing hires for $ 5Y bond

- China Oilfield Services Limited hires for $ bond

- CIMB Bank hires for $ 5Y or 5.5Y sustainability development senior bond

- Guangdong Provincial Communications Group hires for $ bond

- IRFC hires for $ bond

- Chengdu Jingkai Guotou Investment Group hires for $ tap of 5.3% 2024s bond

Rating Changes

- Fitch Downgrades Shimao Group to ‘B-‘; Ratings Remain on RWN

- Duke Realty Corp. Rating Outlook Revised To Positive From Stable On Sustained Strong Operating Performance

Term of the Day

Balance Sheet Runoff

A balance sheet run-off in central banking parlance refers to a process of reducing the size of the central bank’s balance sheet in a path towards tightening monetary policy. Here, the portfolio assets of the central bank like Treasuries, MBS etc. are allowed to mature without reinvesting coupons and/or redemption amounts, thereby allowing these securities to mature over time and stably reducing the balance sheet size. A runoff can also include outright sales of these assets, indicating a rapid reduction in the balance sheet.

Talking Heads

On Powell Assuring Americans That Fed Will Tackle High Inflation – Fed Chair, Jerome Powell

“If we have to raise interest rates more over time, we will. We will use our tools to get inflation back…To get the kind of very strong labor market we want, with high participation, it is going to take a long expansion…To get a long expansion we are going to need price stability. And so in a way, high inflation is a severe threat to the achievement of maximum employment.”

On World Bank Cutting Global Growth Forecast on Virus Flare-Ups

Ayhan Kose, the chief economist of the Prospects Group

“There is there a serious slowdown underway. The global economy “is basically on two different flight paths: Advanced economies are flying high; emerging-market, developing economies are somewhat flying low and lagging behind.”

On JPMorgan’s Bob Michele Says Hide in Cash With Treasury Yields Going Higher

“Without the central bank purchases and with cash now offering some yield, let’s see how willing investors are to continue to purchase long-duration government debt at significantly negative real yields…We disagree and think the Fed would let the markets drop much further if their primary concern was battling inflation. The strike of any put is likely to be declines of 15%–30% in equities, not 2%–3%.”

On Jeffrey Gundlach Seeing ‘Recessionary Pressure’ Building With Inflation

The Fed seems pretty far behind the curve when you consider wage growth. We’re going to be more on recession watch than we have been… Consumer sentiment has worsened and bond yields “are no longer sending a don’t worry, be happy signal. The market is starting to flash signs of a weaker economy ahead.

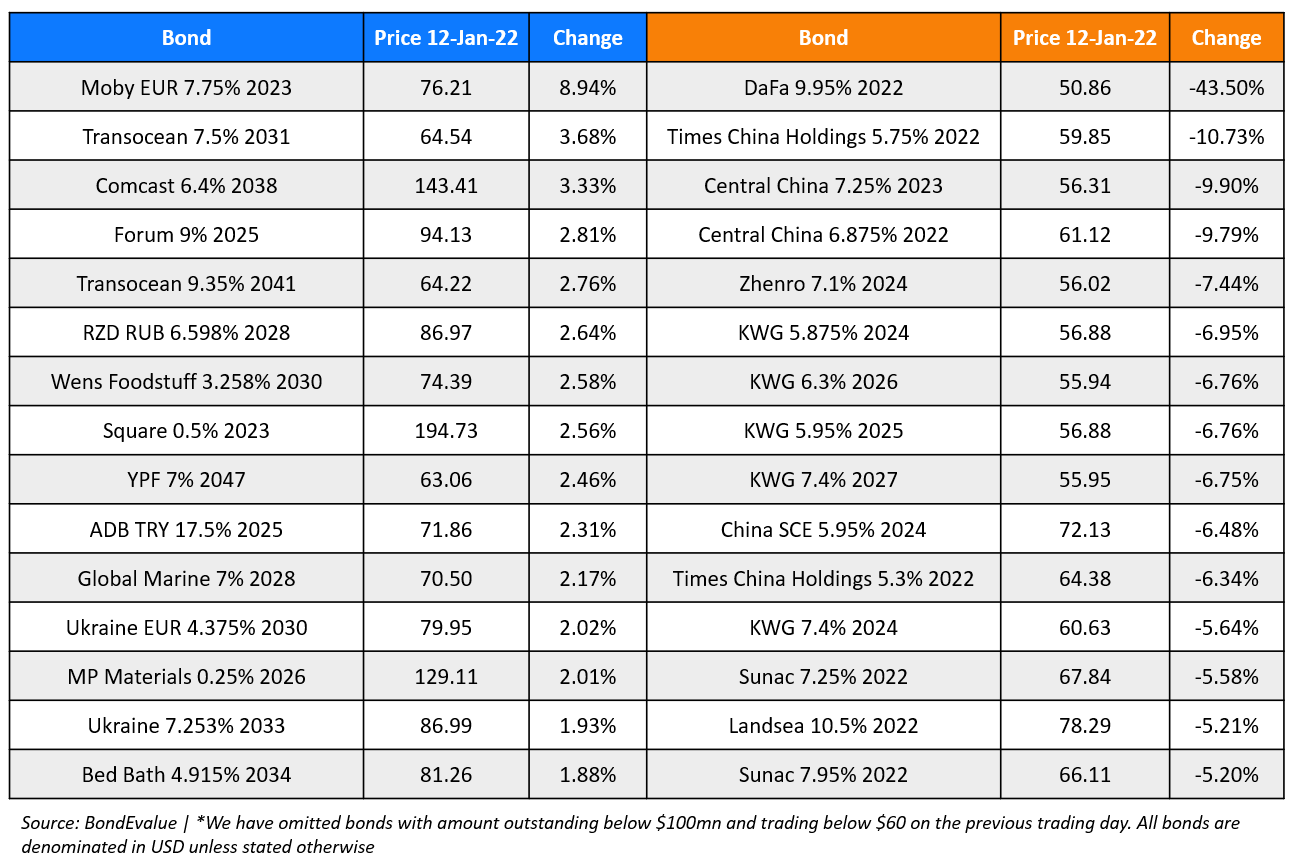

Top Gainers & Losers – 12-Jan-22*

Other Stories:

Aeromexico Creditors Approve Restructuring Plan

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.