This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

AVIC Launches $ 3Y; Markets Await CPI Data

March 12, 2024

US Treasury yields moved 3-6bp higher across the curve on Monday. The New York Fed’s 1Y inflation expectations edged up to 3.04% from the prior 3%. Markets await the US CPI data release later today with expectations for the Headline and Core prints at 3.1% and 3.7% respectively. Looking at credit markets, US IG CDS spreads tightened 0.1bp and HY CDS spreads were 0.6bp tighter. Equity markets closed lower with the S&P and Nasdaq down 0.1% and 0.5% respectively.

European equity markets ended slightly lower. Credit markets in the region saw the European main CDS spreads widen 0.6bp and crossover spreads widen by 2.9bp. Asian equity markets have opened slightly higher today. Asia ex-Japan IG CDS spreads were 0.9bp wider. Japan’s final Q3 GDP reading was revised upward to 0.1% from the preliminary reading of -0.1%, helping them avoid a technical recession.

New Bond Issues

- Avic International Leasing $ 3Y at T+130bp area

ANZ raised $3.5bn via a three-part deal. It raised:

- $1.25bn via a 2Y bond at a yield of 5%, 23bp inside initial guidance of IPT+70bp area, and offering a new issue premium of 44bp over its existing 4.75% note due September 2026 that currently yield 4.56%

- $1.25bn via a 2Y FRN at a yield of SOFR+56bp vs initial guidance of SOFR equivalent

- $1bn via a 10.5NC5.5 bond at a yield of 5.731%, 25bp inside initial guidance of IPT+190bp area. The bonds are callable from 18 September 2029, and if not called, the coupon resets then and every five years thereafter to the prevailing 5Y US Treasury yield plus 161.8bp. The bonds offer a new issue premium of 14.1bp over its existing 6.405% 2034s (callable in September 2029) that currently yield 5.59%.

The 2Y fixed note and FRN are rated Aa2/AA-/A+, while the 10.5NC5.5 notes are rated A3/BBB+/A-. Proceeds will be used for general corporate purposes.

ING Groep raised $3bn via a two-part deal. It raised:

- $1.5b via a 6NC5 bond at a yield of 5.335%, 30bp inside initial guidance of T+155bp

- $1.5b via a 11NC10 bond at a yield of 5.55%, 30bp inside initial guidance of T+175bp

The notes are rated Baa1/A-/A+.

Banco do Brasil raised $750mn via a 7Y sustainability note at a yield of 6.30%, 45bp inside initial guidance of 6.75% area. The notes are rated Ba2/BB/BB, and proceeds will be used to finance and/or refinance, in whole or in part, of existing or future environmental and social projects that meet the eligibility criteria.

Santander raised $4bn via a four-part deal.

The senior non-preferred notes are rated Baa1/A-/A- and the subordinated 10Y is rated Baa2/BBB+/BBB.

New Bond Pipeline

- EHi Car Services hires for $ bond

- Shinhan Bank hires for bond

Rating Changes

- Moody’s upgrades Aston Martin’s CFR to B3 from Caa1; outlook changed to stable from positive

- Moody’s withdraws China Vanke’s Baa3 issuer ratings, assigns Ba1 CFR and downgrades senior unsecured ratings; places all ratings on review for downgrade

- Moody’s changes Greenko’s outlook to negative, affirms ratings

- Moody’s places EQM Midstream Partners’ ratings on review for upgrade

Term of the Day

Technical Recession

A technical recession for economic purposes is defined as one where a country witnessed two consecutive quarters of negative GDP growth/decline in GDP. However in reality, it might not necessarily indicate an actual recession and could be influenced by temporary factors. A actual recession may sustain for a considerable period of time and covers a wide range of declines in economic activity.

Talking Heads

On ECB rate cut coming, but not just yet – ECB Governing Council Member, Peter Kazimir

“We will learn a bit more in April, but only in June, with new forecasts at hand, will the level of confidence reach the threshold… current picture clearly favours staying calm for the coming weeks and delivering the first rate cut in summer”… Once rates start coming down, favoring a smooth and steady cycle of easing.

On Fed to start rate cuts in June; risk fewer delivered this year: Reuters poll

Michael Gapen, chief US economist at BofA

“Fed is seeking ‘greater confidence’ on inflation before it starts normalizing its policy stance… (inflation progress) will give the Fed enough confidence to begin a gradual cutting cycle in June… this Fed is data dependent and wants to avoid backtracking after it starts”

Andrew Hollenhorst, chief US economist at Citi

“It only takes two dots moving higher to shift the median from 75 bps of cuts to 50 bps of cuts…. given more hawkish Fed officials are already above the median .. we think the most likely case is the 2024 median stays put signaling 75 bps of cuts this year.”

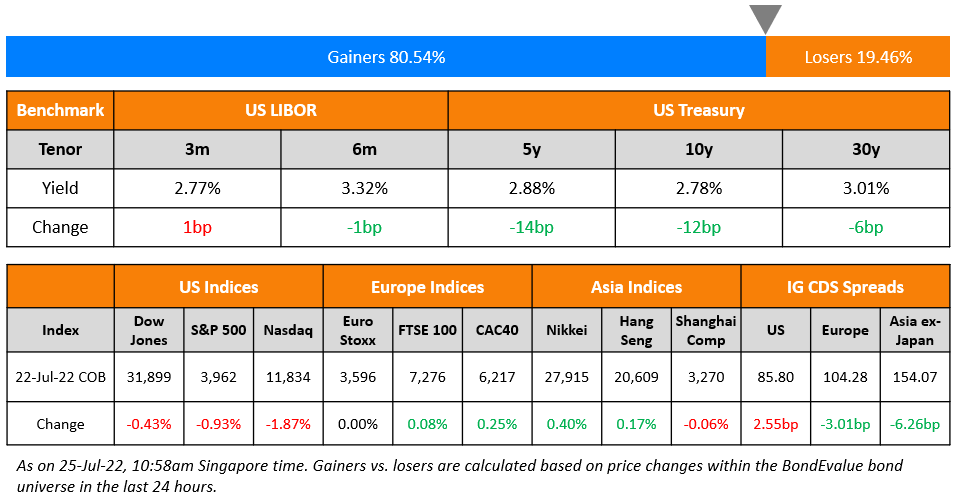

Top Gainers & Losers- 12-March-24*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.