This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Bond Markets Kickstart 2023 with Surge in Deals; Macro; New Issues; Talking Heads; Top Gainers and Losers

January 4, 2023

US Treasuries rallied on Tuesday with yields dropping by 8-12bp. This was the strongest start to a new year since 2001. The peak fed funds rate was up 1bp to 4.97% for the June 2023 meeting. The probability of a 25bp hike at the FOMC’s February 2023 meeting stands at 68%, unchanged from yesterday. US equity markets ended lower, with the S&P and Nasdaq down 0.4% and 0.7% respectively. US IG and HY CDS spreads were 1.5bp and 5.8bp tighter.

Bond markets kickstarted the year with a surge in issuance volumes. There were 60 new USD and EUR-denominated bond deals priced across regions totaling ~60.7bn. In terms of dollar deals, markets saw 41 new deals totaling $40.8bn, ~2% of 2022’s full year issuance volume in just a day. Of the 41 dollar deals, 19 were from investment grade issuers who collectively raised $34bn.

European equity markets ended slightly higher. The European main and crossover CDS spreads tightened by 1.8bp and 12.2bp respectively. German 10Y Bund yields fell over 7bp after Germany’s December inflation print came in at 9.6% vs. 11.3% in November. Turkey’s inflation also cooled to 64.3% in December from 84.4% in November with analysts noting that this was due to base effects (Term of the Day, explained below). Asian equity markets have opened mixed today. Asia ex-Japan CDS spreads tightened by 3.9bp. Singapore’s PMI fell 0.1 points to 49.7 in December, a fourth consecutive month of contraction in overall activity.

New Bond Issues

- Indonesia $ 5Y/10Y/30Y at 5.15%/5.5%/6.15% areas

- Hong Kong SAR $ 30Y at T+190bp area

-

Kexim $ 3Y/5Y bond and 10Y blue bond at IPG T+120bp/T+155bp/T+180bp areas

- NAB $ 3Y/3Y FRN/5Y/10Y Tier 2 at T+100bp/SOFR equiv./T+130bp/T+300bp areas

.png)

UBS raised $4bn via a dual-trancher. It raised $1.75n via 4NC3 bond at a yield of 5.711%, 25bp inside initial guidance of T+180bp area. It also raised $2.25bn via 11NC10 bond at a yield of 5.959%, 30bp inside initial guidance of T+250bp area. The senior unsecured bonds are rated A-/A+ (S&P/Fitch).

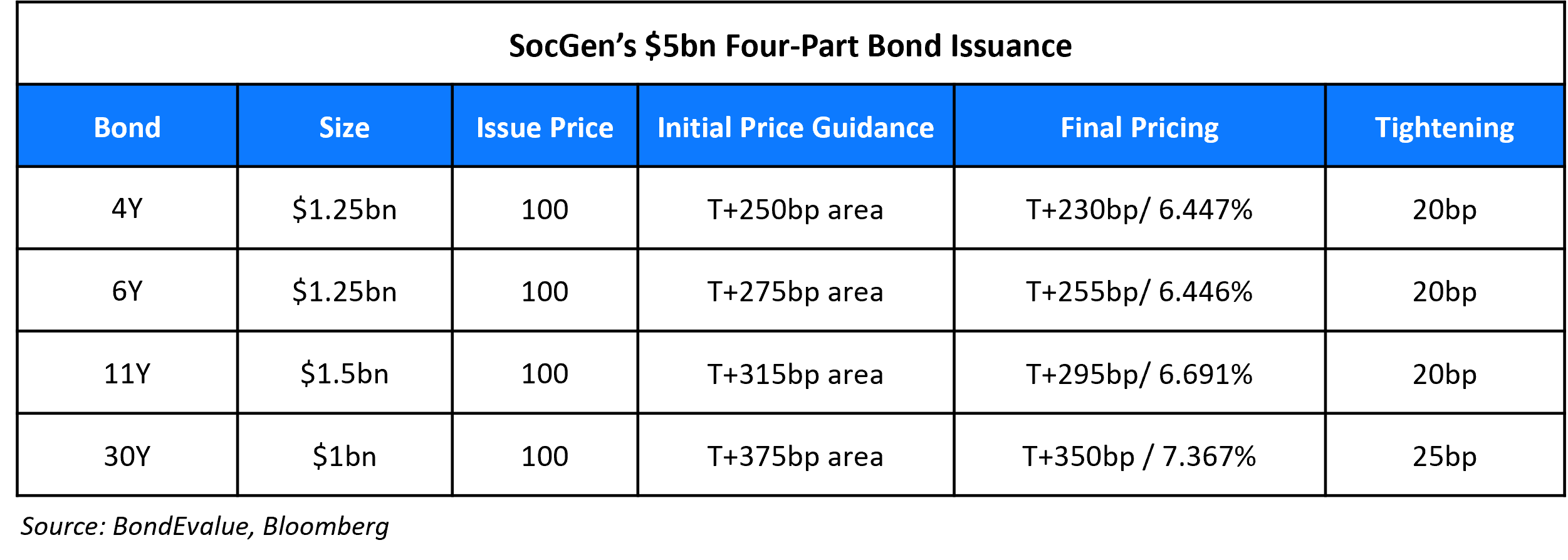

SocGen raised $5bn via a four-tranche deal. It raised:

The senior non-preferred bonds have expected ratings of Baa2/BBB/A-. Its 30Y subordinated Tier 2 note has expected ratings of Baa3/BBB-/BBB.

Mexico raised $4bn via a dual-trancher. It raised $1.25bn via 5Y bond at a yield of 5.446%, 45bp inside initial guidance of T+195bp area. It also raised $2.75bn via 12Y bond at 6.395%, 35bp inside initial guidance of T+295bp area. The senior unsecured bonds are rated Baa2/BBB/BBB-. The 5Y was priced 25bp tighter to its green 3.875% bonds due April 2028 that currently yield 3.7%. The 12Y was priced 18.5bp wider to its 6.75% bonds due September 2034 that currently yield 6.21%.

CBA raised $1.5bn via a dual-trancher. It raised $1.2bn via 2Y bond at a yield of 5.079%, unchanged from initial guidance of area. It also raised $300mn via 2Y FRN at a SOFR+63bp unchanged from initial guidance. The bonds received orders over $2.8bn, 1.9x issue size.

Ford Motor Credit raised $2.75bn via a three-trancher. It raised:

- $1.3bn via a 3Y bond at a yield of 7%, 37.5bp inside initial guidance of 7.375% area

- $300mn via a 3Y FRN at SOFR+295bp vs. initial guidance of SOFR equivalent

- $1.15bn via 7Y bond at a yield of 7.375%, 37.5bp inside initial guidance of 7.75% area. The bonds were priced at a new issue premium of 17.5bp vs. its older 9.625% bonds due April 2030.

The senior unsecured bonds are rated Ba2/BB+/BB+. Proceeds will be used for general corporate purposes.

BNP Paribas raised €1.25bn via an 8NC7 issuance at a yield of 3.892%, ~22.5bp inside initial guidance of MS+110/115bp area. The senior preferred bonds are rated Aa3/A+/AA-.

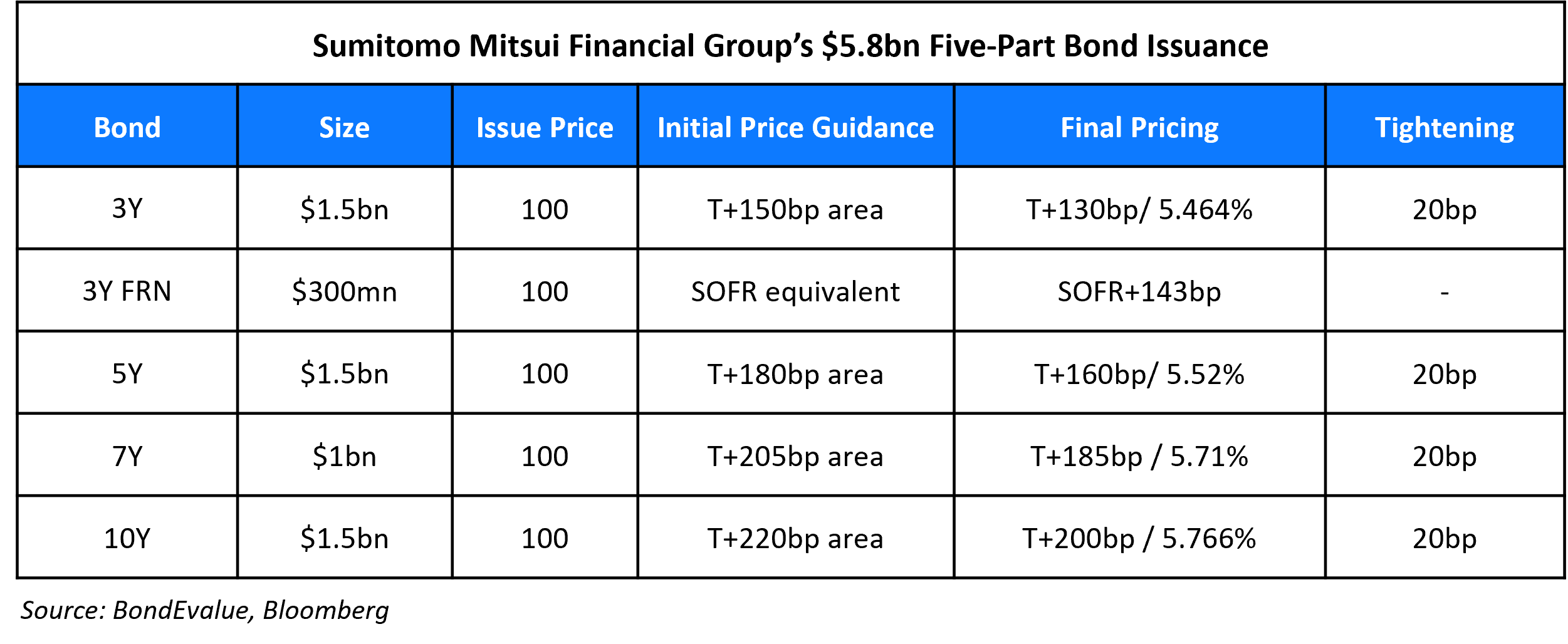

Sumitomo Mitsui Financial Group (SMFG) raised $5.8bn via a five-tranche deal. It raised

The senior unsecured bonds have expected ratings of A1/A-. Proceeds will be used for general corporate purposes.

Term of the Day

Base Effects

Base effect refers to the impact of comparing current levels of an index for a given period vs. levels during the same period a year/month ago. Let us take inflation as the metric. Analysts look at the inflation print for a given month and compare it with the same month in the previous year to find out the YoY change. If the rate of inflation was low/high in the previous year’s corresponding period, even a little increase/decrease in the price index will result in a larger/smaller rate of inflation in the current year.

For example, let’s assumed the inflation index values are at 100 in December 2020, at 110 in December 2021 and 120 in December 2022. While the inflation index has picked by 10 points in both years, the percentage rise in inflation over the previous year is 10% for 2021 and 9.09% for 2022. This is due to the higher base of 110 in 2021 leading to a lower inflation in 2022.

Talking Heads

On Treasuries Chalking Up Strongest New Year Surge Since Greenspan

Ian Lyngen, head of US rates at BMO Capital Markets

“The last two weeks of 2022 can be aptly characterized as a bearish phase in US rates. As investors return from the long weekend we’re anticipating ‘cooler heads’ will prevail.”

Gregory Faranello, head of US rates trading and strategy at AmeriVet Securities

“The corporate calendar is generally large in January, but for the first trading day of a year this is impressive and a sign of the times”

On Fed Minutes to Reveal Source of Inflation Angst Pushing Up Rates

Kevin Cummins, chief US economist at NatWest Markets

“The inflation forecast being raised was surprising because it sounded like most economists on the street were expecting very little change there, and I was expecting them to cut their forecast. It seems that there is more of a consensus view that they’ve got to go above 5% than certainly I would have thought the numbers implied.”

On no Dollars as foreign currency crunch hits Egypt’s economy

Farouk Soussa, economist at Goldman Sachs

“The CBE could clear the market by continuing to raise rates, floating the currency and restricting the money supply, but the implications for prices and growth are problematic. The authorities’ preferred option is to wait for inflows from the Qataris, the Emiratis and the Saudis to buy assets in Egypt, but that is also uncertain”

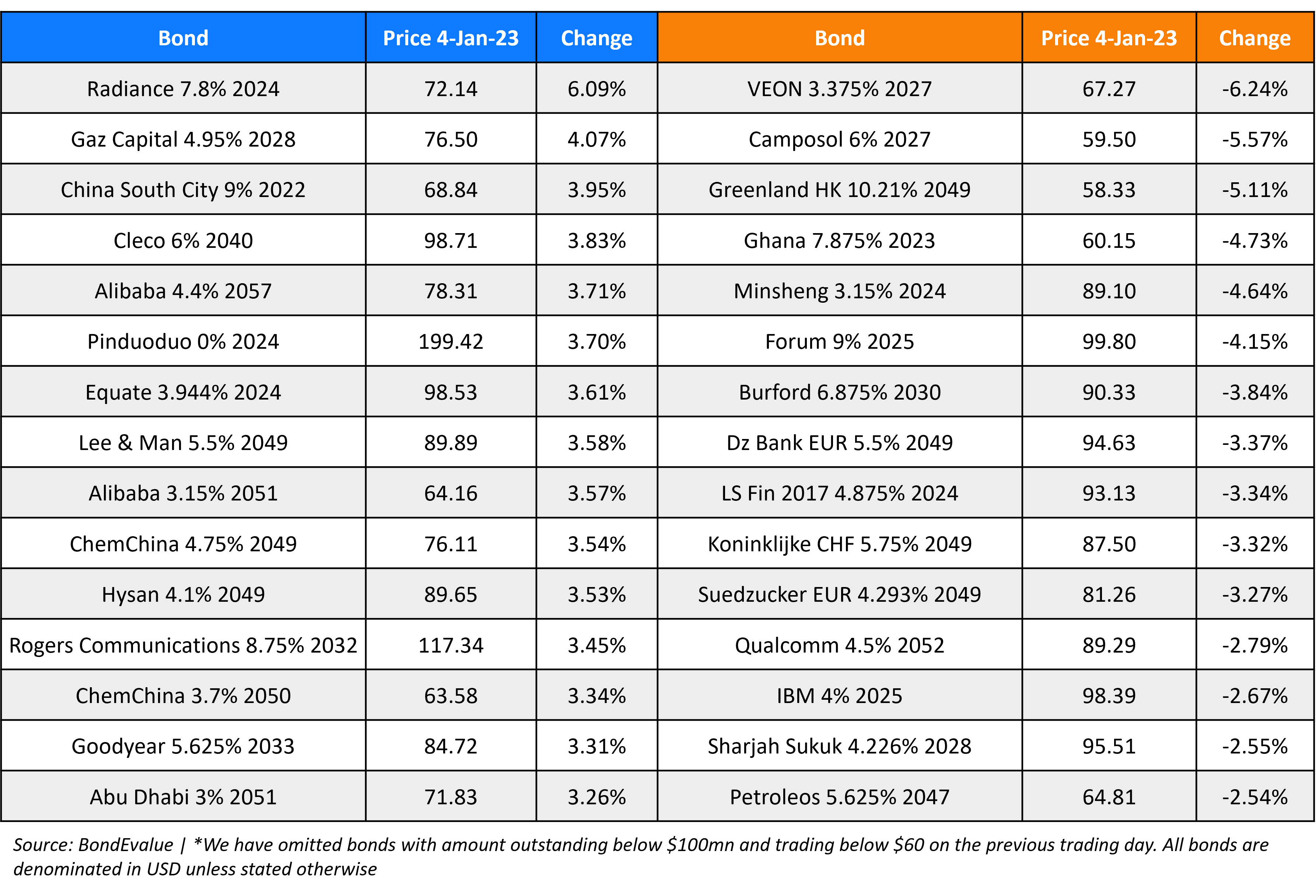

Top Gainers & Losers – 04-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.