This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Credit Agricole Prices S$ 10NC5 Tier 2 at 5.25%

August 31, 2023

US Treasury yields were flat on Wednesday. US ADP employment data showed a 177k increase in private payrolls, below the 371k last month and estimates of 195k. For Q2, the second revision of US GDP came at 2.1%, lower than the preliminary 2.4% reading. CME probabilities for a 25bp rate hike at the November meeting remain relatively unchanged at 42%. US IG credit spreads were tighter by 0.1bp while HY CDS spreads tightened 2.1bp. The S&P and Nasdaq were higher by 0.4-0.5%.

European equity markets were mixed. In credit markets, European main CDS spreads were tighter by 0.7bp with crossover spreads tightening 3.3bp. German inflation came at 6.1% in August, easing slightly from 6.2% the month prior. Spanish inflation rose for a second month in a row to 2.6% on higher fuel prices. Asian equity markets have opened mixed this morning and Asia ex-Japan CDS spreads have tightened by 2.6bp.

New Bond Issues

-

Taizhou Urban Construction $ 3Y at 6% area

Allianz raised $1bn via a 30NC10 Tier 2 bond at a yield of 6.35%, 40bp inside initial guidance of 6.75% area. The bonds are callable in 10 years and every 5 years thereafter. If not called, the coupon will reset at every call date to the US 5Y Treasury plus a spread of 323.2bp. The bonds are unrated. Proceeds will be used for general corporate purposes, including the potential refinancing of existing debt.

Credit Agricole raised S$350mn via a 10NC5 Tier 2 bond at a yield of 5.25%, 25bp inside initial guidance of 5.5% area. If the bonds are uncalled on the first call date of 7 September 2028, its coupon will reset then and every 5 years thereafter at the SGD 5Y overnight indexed swap (OIS) rate plus a spread of 204.5bp. The bonds have a 75% clean-up call (Term of the Day, explained below). The bonds also have a statutory write-down/conversion clause in the event that the relevant regulatory authority decides to exercise its statutory loss absorption power. The bonds have expected ratings of Baa1/BBB+/A-, and received orders over S$560mn, 1.6x issue size. Banks and financial institutions were allocated 36% of the deal, insurers and funds took 34%, while private banks and securities firms took 30%. This is the French bank’s second tier 2 offering this year in the SGD market after issuing a 4.85% bond due 2033 earlier in February. The final pricing of this Tier 2 issuance is in-line with Lloyds’ 5.25% 10NC5 Tier 2s (rated Baa1/BBB+) just two weeks earlier. The table below compares Credit Agricole’s new Tier 2s with other similar-rated SGD-denominated Tier 2s.

Hefei Industry Investment raised $300mn via a 3Y bond at a yield of 5.8%, 20bp inside initial guidance of 6% area. The senior unsecured bonds have expected ratings of BBB (Fitch) and also have a change of control put at 101. Proceeds will be used to refinance the issuer’s outstanding 2.95% 2023s, maturing in September.

Nordea Bank raised €1bn via a 3NC2 senior non-preferred bond at a yield of 4.39%, 22bp inside initial guidance of MS+90bp area. If uncalled after 2 years, the coupon will reset at the 3M EURIBOR plus a spread of 68bp quarterly thereafter. The bonds have expected ratings of A3/A/AA-, and received orders over €1.85bn, 1.9x issue size. Proceeds will be used to finance/refinance existing loans.

Rating Changes

- 3M Co. Downgraded To ‘BBB+’ On $6 Billion Combat Arms Earplugs Settlement; Ratings Remain On CreditWatch Negative

New Bond Pipeline

- ADCB hires for $ Long 5Y Green bond

- LG Energy hires for $ 3Y and/or 5Y Green bond

- Mongolian Mining hires for $ bond

Term of the Day

Clean-up Call

A clean-up call refers to a call provision, whereby once a stated percentage of a security is retired, the issuer is obliged to call the remainder of the tranche. While clean-up calls are generally more commonly observed in mortgage-backed securities (MBS), they may also be present as a feature in some bonds. This is different from a normal call option in a bond where the issuer has an option to redeem their bond fully during the specified call date./period.

For example, Credit Agricole today priced a S$350mn 10NC5 Tier 2 bond at a yield of 5.25% with a 75% clean-up call. This indicates that once 75% of the bond is called back, the issuer is obligated to immediately redeem the remaining 25%.

Talking Heads

On Companies Facing Hybrid Dilemma

Matthias Reschke, JPMorgan Chase head of European IG Finance

“There are two camps of corporate issuers with hybrids: those that see the merit as a well-established part of the capital stack and will likely be replacing them with new hybrid issuances”

Nik Dhanani, the global head of strategic solutions at HSBC

“For many corporates, hybrids are now an established component of the capital structure, and they continue to see value in the instrument even if absolute costs are higher”

On where defaults loom, finding resilient companies Is Delivering Big Returns

Dimitry Griko, founder of Arkaim Advisors

“The common feature is they’ve all sold off more than they initially deserved… We have companies where the assets are extremely geographically diversified and the Ebitda, for example, was not as influenced by the war as one would expect.”

Okan Akin, a credit analyst at AllianceBernstein

“With healthy financials and a solid ability to meet their repayment obligations, many companies in distressed countries offer good investment opportunities”

“As long as it looks like we’re on a path to gradually get to 2% (inflation), there’s no reason to hike further from here… We’ll have to have a little bit more time before we can say unequivocally that that’s the case (regarding soft landing)”

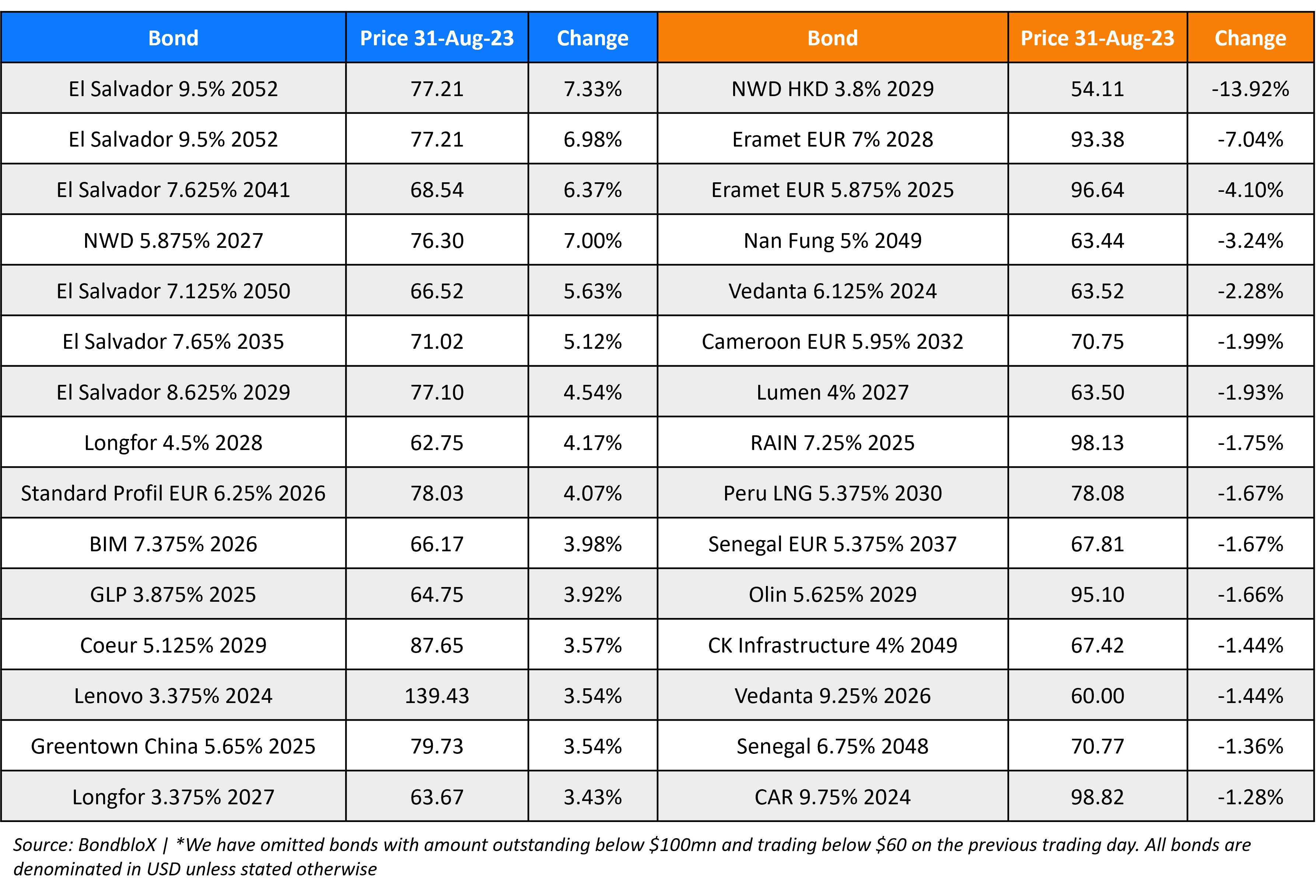

Top Gainers & Losers- 31-August-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.