This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

February 2024: Dollar Bonds Drop Amid Higher For Longer Rate Expectations

March 1, 2024

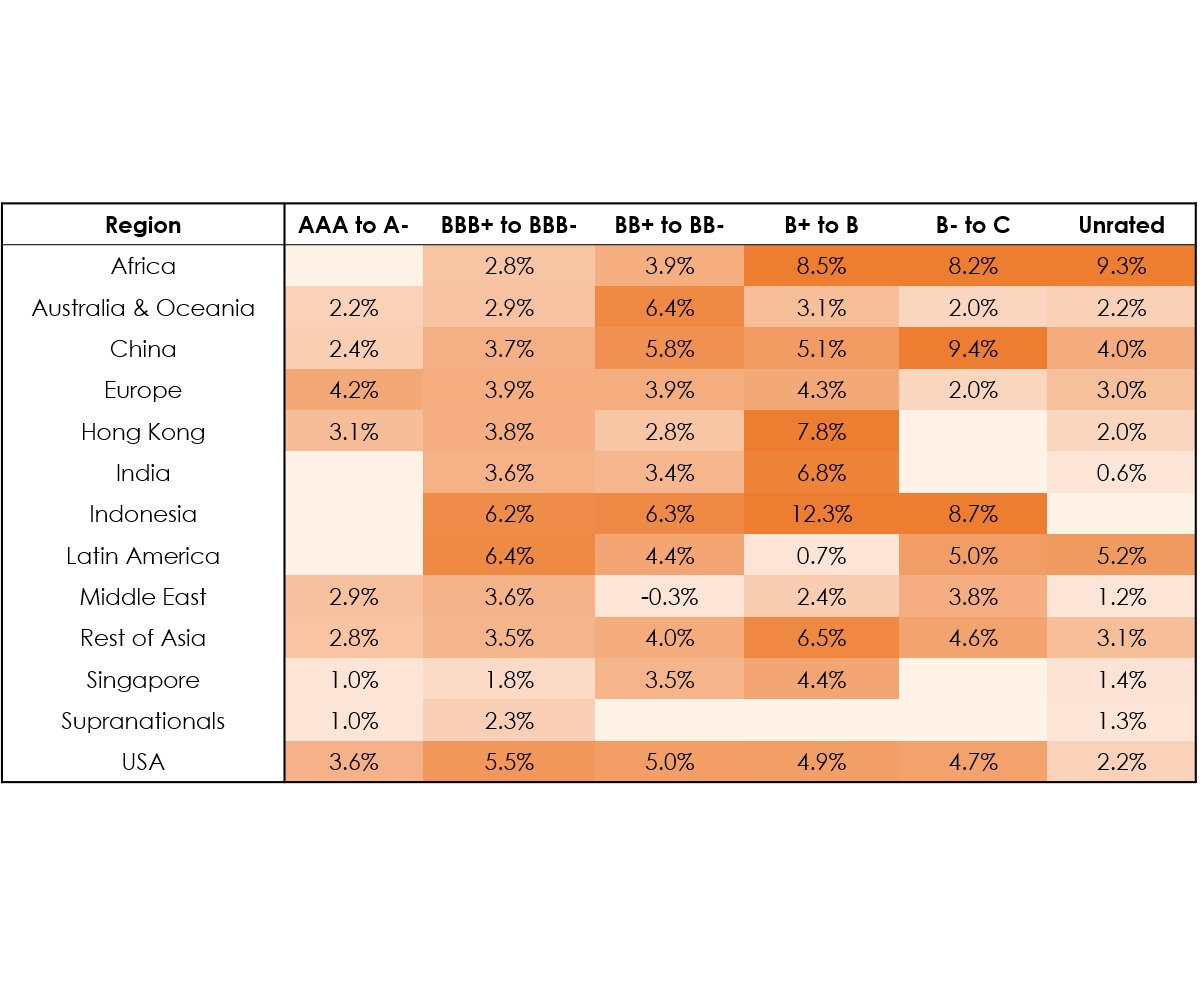

February 2024 was a relatively poor month for bond investors with 74% of dollar bonds ending lower (price returns ex-coupons). However, looking deeper, about 52% of High Yield (HY) bonds ended higher and outperformed Investment Grade (IG) bonds, where 83% of IG bonds ended lower. This came amid higher for longer rate expectations by the Fed alongside the repricing of rate cuts and solid economic data.

February saw the Treasury yield curve bear flatten, with short-term rates rising more than long-term rates as markets repriced their expectations of Fed rate cuts in 2024. The 2Y yield closed over 30bp higher at 4.62% and the 10Y yield was up 23bp at 4.25% to end the month. The US economy continued to show resilience, starting with the non-farm payrolls (NFP) showing a massive pick-up of 353k jobs, much higher than expectations of 185k and also above the prior month's upwardly revised 333k. Average Hourly Earnings (AHE) YoY rose 4.5%, much higher than the surveyed 4.1% and the prior month's upwardly revised 4.3% reading, while the unemployment rate held steady at 3.7%. Besides, US inflation also continued to show a lower pace of deceleration, with January CPI YoY up 3.1% vs. the prior month's 3.4%, but higher than estimates of 2.9%. Core CPI YoY also rose by 3.9%, unchanged from the prior month and higher than the estimated 3.7%. Manufacturing activity continued to show improvement, just at the cusp of going back to expansionary territory and the Services sector improved further. Following the continued upbeat data, the FOMC's January meeting minutes and several Fed speaker hinting at a delay in rate cuts, the market also repriced its expectations of Fed rate cuts in 2024. Whilst beginning the month expecting 125bp in rate cuts, markets are now expecting only 75bp in rate cuts currently.

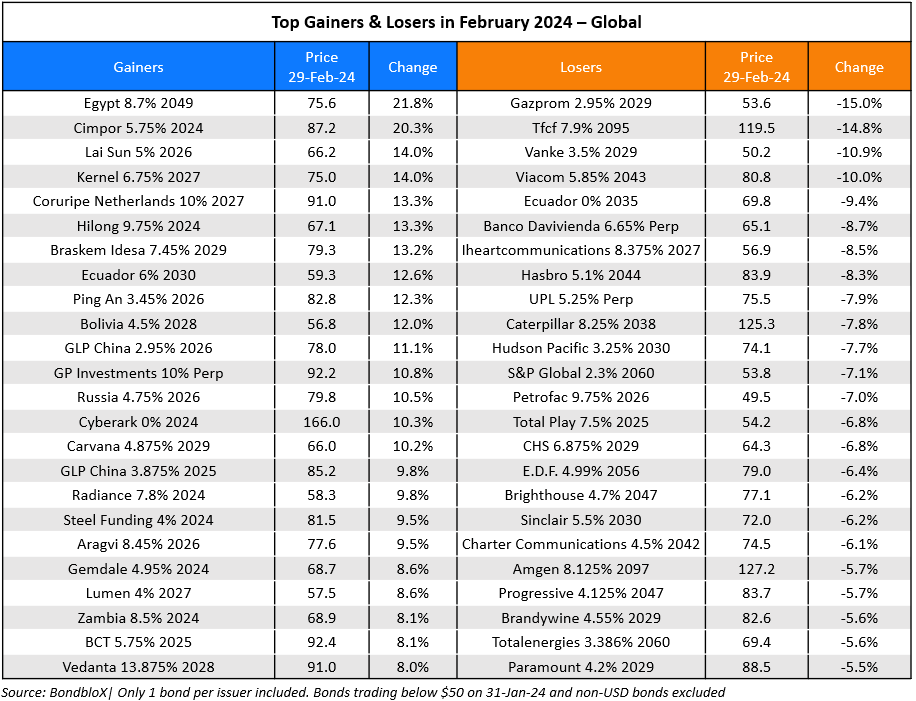

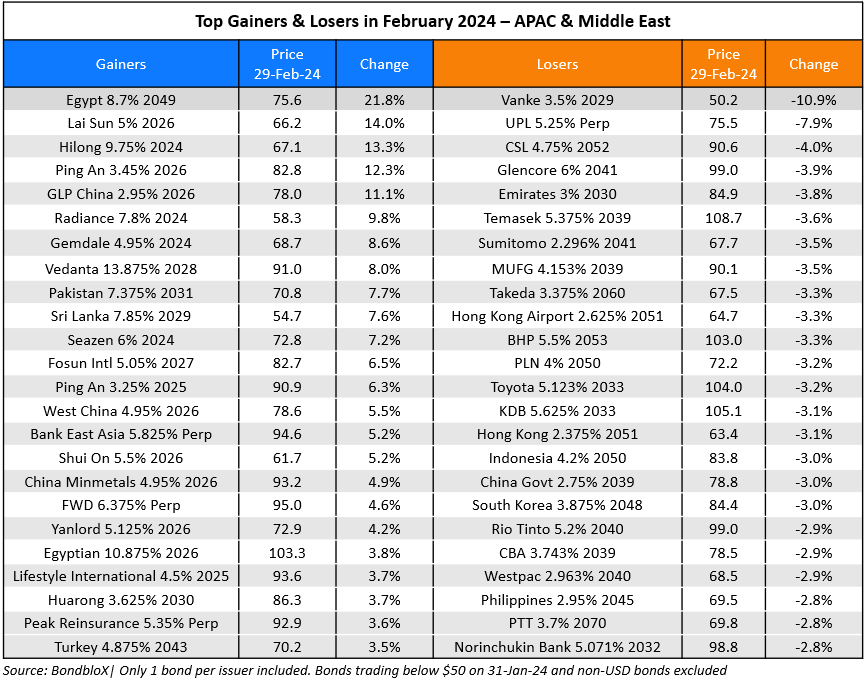

HY dollar bonds outperformed IG dollar bonds. In the top-rated AAA to A- bucket, longer dated bonds performed poorly due to rise in the benchmark rates, where for instance, the 30Y Treasury yield rose 30bp to 4.4%. Some of the top losers included bonds maturing beyond 2060 of companies like Totalenergies, Apple, Paypal that fell over 5% each. However, there was no particular pattern among the gainers. In the BBB+ to BBB- bucket, China Vanke’s and Viacom’s bonds were among the top losers. Vanke’s 2027s and 2029s dropped by 8-11% last month, after a report claimed that the company was in talks with creditors to extend some of its non-standard debt. FWD's 6.375% Perp was also among the top gainers in this space after the company reported that it was considering stake sale worth $10bn to reduce debt.

Under the HY segment, in the BB to B bucket,Braskem's dollar bonds were among the top gainers after it was reported that the company had received interest from petroleum companies PIC and Saudi Aramco to acquire a stake in it. Kenya’s bonds were also among the top gainers after the country launched a tender offer for its June 2024s, alleviating debt repayment concerns. Turkey’s bonds also topped the charts in terms of returns. UPL's dollar bonds were among the top losers after it reported a weak set of numbers in 3Q 2024 and was subsequently downgraded to Ba1 by Moody’s. Charter Communications' bonds also dropped after it reported poor results in the beginning of the month. In the B- to C space, Egypt's bonds were the biggest gainers with returns ranging from 12–22% after the UAE agreed to invest $35bn in development projects of the country. Meanwhile Community Health Systems’ bonds were among the top losers here after it highlighted an ongoing DOJ investigation.

Issuance Volumes

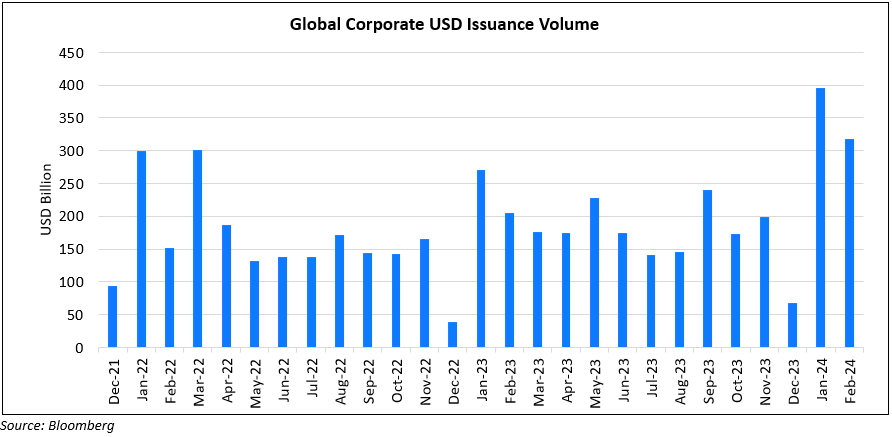

Global corporate dollar bond issuances stood at $318bn in February, ~20% higher than January. As compared to February 2023, issuance volumes were up 1.6x. 86% of the issuance volumes came from IG issuers with HY comprising 13% and unrated issuers taking the remainder.

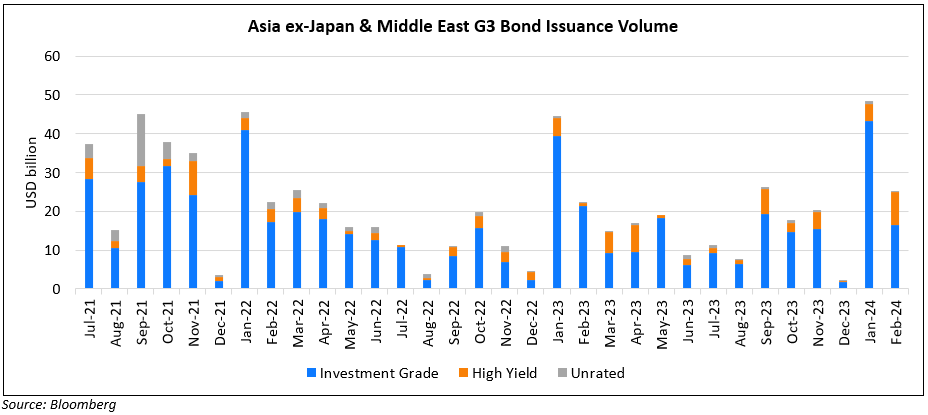

Asia ex-Japan & Middle East G3 issuance stood at $28.5bn, up 52% MoM and 1.1x YoY. 65% of the volumes came from IG issuers with HY issuing 34% and unrated issuers taking the rest.

Largest Deals

The largest deals globally were led by US corporates with AbbVie’s $15bn and Cisco’s $13.5bn seven-part deals leading the tables, followed by Bristol Myers’ $13bn nine-part debt deal. Besides, Eli Lily’s $6.5bn six-part debt deal, IBM’s and Citigroup’s $5.5bn seven-part and two-part deals led tables too.

In the APAC and Middle East region, deal volumes were led by KDB’s $3bn two-tranche deal, Saudi Electricity’s $2.2bn and Bahrain’s $2bn two-tranchers leading the tables, followed by Westpac's $1.5bn two-trancher, NAB’s $1.35bn deal and Hyundai Capital Services’ $1bn two-part deals.

Top Gainers & Losers

Go back to Latest bond Market News

Related Posts:

Bond Yields – Explained

November 16, 2018

Bond Investors Up $75.4 Billion in 1Q19

April 10, 2019

2021 Recap: China Real Estate – When Hope Went Up In Smoke

December 20, 2021

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.