This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Fed Minutes Sound Cautious Tone; ADCB Prices AT1 at 8%

November 22, 2023

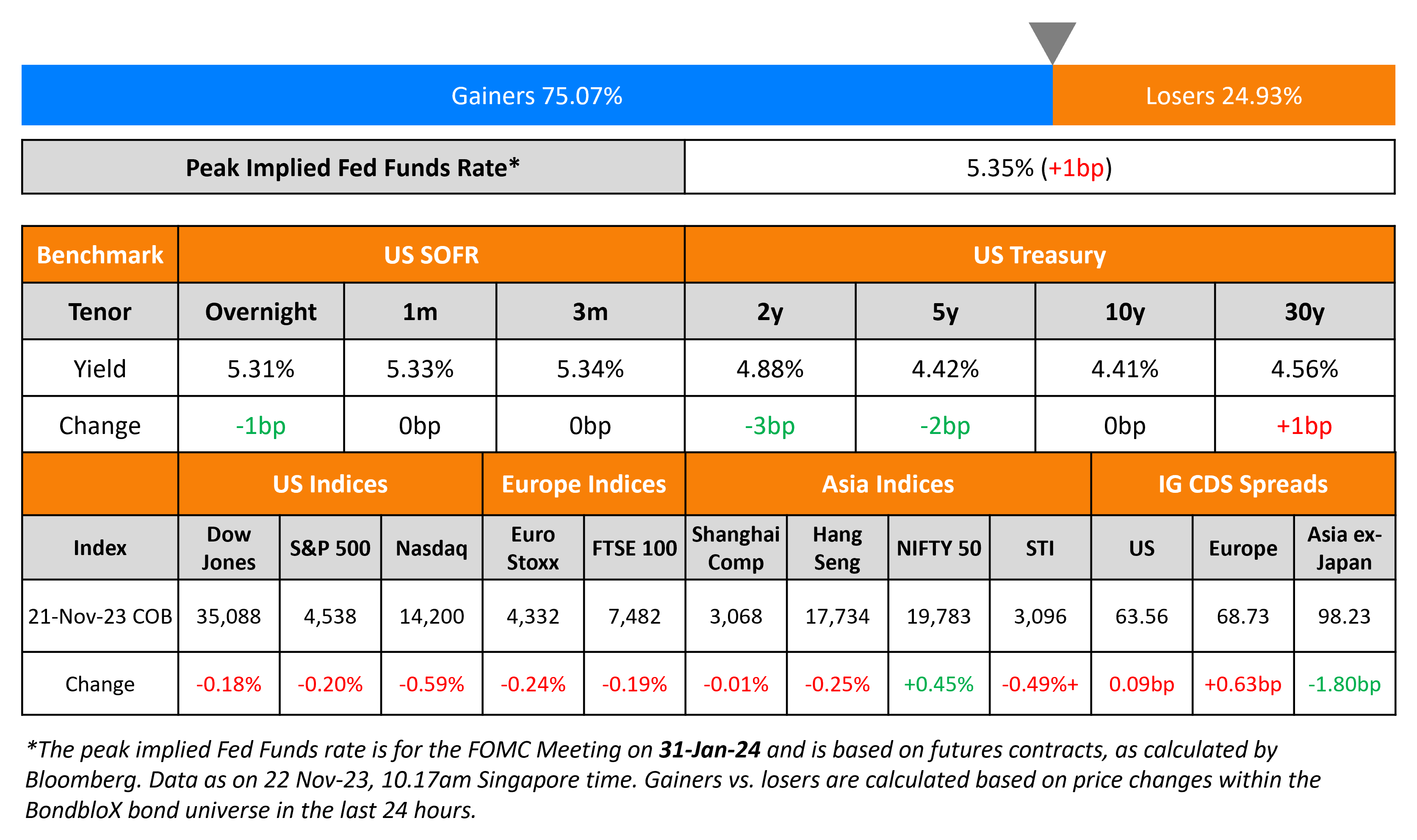

US Treasury yields were steady across the curve on Tuesday. The Federal Reserve’s minutes released yesterday showed that policymakers agreed on a stance to “proceed carefully” on future interest-rate moves and base any further tightening on progress toward their inflation goal. The auction of US 10Y Treasury inflation-protected securities (TIPS) was weak, with analysts noting that it may signal a possible deceleration in inflation. The bid-to-cover was at 2.38x, lower than the previous 2.44x and tailed by 3.5bp. The Peak Fed Funds Rate was higher again by 1bp. US credit markets saw IG CDS spreads widen 0.1bp and HY spreads tighten by 0.5bp. S&P and Nasdaq fell by 0.2% and 0.6% respectively.

European equity markets were stable. In credit markets, European main CDS spreads were wider by 0.6bp and crossover spreads widened by 2.3bp. Asian equity markets have opened weaker today and Asia ex-Japan IG CDS spreads were tighter by 1.8bp.

New Bond Issues

- CCB HK $ 3Y at T+95bp area / CCB DIFC $ 3Y FRN at SOFR+110bp area / CCB Luxembourg € 3Y at MS+90bp area

Pioneer Reward, a subsidiary of Huatai Securities, raised $800mn via a 3Y FRN at a yield of 6.246%. The floating coupon will reset at the overnight SOFR plus a spread of 90bps and will be paid quarterly. The senior unsecured bonds have expected ratings of BBB+ (S&P) and are guaranteed by Huatai Securities, rated Baa1/BBB+ (Moody’s/S&P). Proceeds will be used to repay offshore debt when due and support offshore business development.

Abu Dhabi Commercial Bank (ADCB) raised $750mn via a PerpNC5.5 AT1 bond at a yield of 8%, 62.5bp inside initial guidance of 8.625% area. If uncalled after its first call date in November 2028, the coupon will reset at the first reset date in May 2029 and every five years thereafter at the US 5Y Treasury yield plus a spread of 352.4bp. The bonds are unrated but the issuer is rated A1/A (Moody’s/S&P). The issue received orders over $4bn, 5.3x issue size. Proceeds will be used to enhance its tier 1 capital as well as for general corporate purposes. While there were no clear comparable from the Middle East, taking a look at those from Europe, the new bonds are priced 21bp wider compared to HSBC’s 8% Perp (callable in 2028) yielding 7.79% and priced 40bp tighter compared to BNP’s 7.75% Perp (callable in 2029) yielding 8.40%.

Rating Changes

- Marks & Spencer PLC Upgraded To ‘BBB-‘ On Robust Operating Performance And Deleveraging; Outlook Stable

- Moody’s upgrades Air New Zealand to Baa1; outlook stable

- Moody’s downgrades Canacol’s ratings to B1; negative outlook

- Falabella S.A. Downgraded To ‘BB+’ From ‘BBB-‘ On Weak Performance And Higher Leverage; Outlook Negative

New Bond Pipeline

- Mongolia hires for $ senior bond

Term of the Day

TIPS

TIPS or Treasury Inflation-Protected Securities are fixed income securities issued by the US Treasury whose returns are linked to the inflation rate. TIPS provide investors protection against inflation by adjusting the principal higher with inflation and lower with deflation, as measured by the Consumer Price Index (CPI). At maturity, investors are paid the higher of the adjusted principal or the original principal. Interest on TIPS is fixed, paid out twice a year and is applied to the adjusted principal. As investors expect inflation in the US to climb higher, demand for TIPS is likely to increase.

Talking Heads

On cautious policy mode as risks become more two-sided – Fed Minutes

“All participants agreed that the Committee was in a position to proceed carefully. Participants noted that further tightening of monetary policy would be appropriate if incoming information indicated that progress toward the Committee’s inflation objective was insufficient”… “all participants judged it appropriate to maintain” the current rate setting.

On Risk of Missing Out If Staying in Cash

Greg Whiteley, head of government securities investing at DoubleLine

“My sense of things right now is that 4 1/2 to 5% is a safe place to be buying bonds”

Ryan Murphy, head of fixed-income business development at Capital Group

“At some point, though, and you’ve seen this just over the course of this month, that approach means you miss all the potential price appreciation if the economy starts to slow”

On Seeing S&P 500 Hitting Record 5,000 Next Year – BofA

“The market has absorbed significant geopolitical shocks already. US exceptionalism is intact… much more upside potential… Bull markets typically end with high conviction and euphoria — we are far from that”

On US high-grade corporate bond spreads to tighten in 2024 – JPMC

“What is not a possibility but rather a certainty, in our view, is that yields at multi-decade highs leads to buying of HG credit day in and day out… Such an environment of slow but positive growth, declining rates such that total returns for HG bond holders will be strong, and lower policy rates which makes cash less attractive are all quite supportive for HG credit markets”

Top Gainers & Losers- 22-November-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.