This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Fed Officials On Rate Cuts As They Await More Data

April 5, 2024

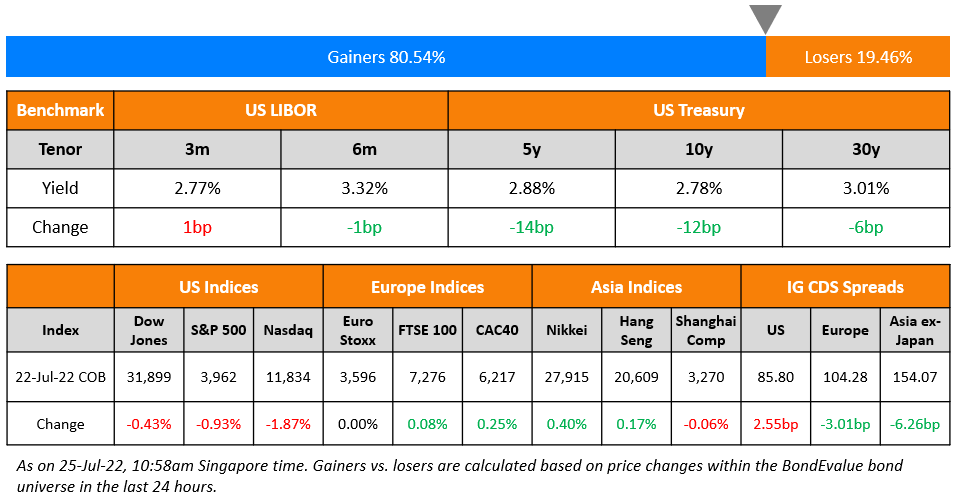

US Treasury yields moved lower by 4-5bp across the curve on Thursday amid risk-off sentiment in markets. US IG CDS spreads widened 1.6bp and the HY spreads widened 8bp with the S&P and Nasdaq closing 1.2-1.4% lower. This came as Brent crude crossed the $90/bbl mark amid tensions in the Middle East over the course of the week after an Israeli strike on an Iranian diplomatic compound in Syria. Oil prices have jumped over 6% this week and are up nearly 20% YTD.

Three Fed speaker came out with their take on the path of the Fed’s policy. Minneapolis Fed President Neel Kashkari said that he has “jotted down two rate cuts this year if inflation continues to fall back towards our 2% target”. However he noted that if inflation moves “sideways, then that would make me question whether we needed to do those rate cuts at all”. Cleveland Fed’s Loretta Mester said that she “wants to see a couple more months of data” to help make a stronger case for whether rates should be cut. Richmond Fed’s Thomas Barkin outlined his concerns on recent inflation data noting, “You get another month that looks like January or February, that takes you in a very different direction of how forward leaning you are”. However he also highlighted that he believed the disinflation process is continuing.

European equity indices ended slightly higher. European IG CDS spreads tightened 1.3bp and crossover spreads were 6bp tighter. Asian equity markets have opened lower today. The European Composite PMI’s final reading came at 50.3, slightly better than expectations of 49.9. Asia ex-Japan IG CDS spreads were 0.1bp wider.

New Bond Issues

Rating Changes

-

Lumen Technologies Inc. Upgraded To ‘CCC+’ From ‘SD’; Outlook Stable; Debt Rating Actions Taken

-

Fitch Upgrades Rolls-Royce & Partners Finance to ‘BBB-‘; Outlook Positive

- Fitch Downgrades Volcan to ‘CC’

Term of the Day

Revolving Credit

Revolving credit is a form of borrowing where the credit line has a maximum limit but the borrower can access it in any quantum based on their funding needs. In a normal borrowing, once the loan has been repaid, the borrower must take a new loan to borrow more. In revolving debt, the borrower can re-access any funds that have been paid back too. Revolving debt generally comes with a higher interest rate and does not necessarily have a fixed coupon.

Talking Heads

On Sovereign Distress Lingers in Latin America Despite Rally in Emerging Markets

Carlos de Sousa, a portfolio manager at Vontobel Asset

“These are countries with very low margin of maneuver… if something goes wrong, or there’s a severe external shock, then they may not manage to avoid it”

Guido Chamorro, co-head of EM sovereign debt at Pictet Asset

“Latin America can feel all or nothing. Either you make it into investment grade or else you run the risk of going into full distress”

On Market in a ‘Golden Age of Credit Allocation’

Chris Sheldon, KKR’s co-head of credit and markets

“The timing and magnitude of rate cuts is impossible to predict…economy is slowing, defaults will rise, but not sky rocket and that dispersion will increase… opportunities for credit selection… a good time to be credit investor”

US 10-Year Yield Is Set to Revisit 4.5%

Padhraic Garvey, head of global debt and rates strategy at ING Financial

“Tough to stand in the way of the 10-year heading to 4.5%”

Michael Darda at Roth MKM

Overall, the “no landing” view on the economy is beginning to take hold in the bond market

Michael Gladchun, a co-PM Loomis, Sayles & Co.

As yields “have backed up again up towards the high levels, we have been buyers of the dip”

Top Gainers & Losers- 05-April-24*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.