This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

HSBC, OCBC, Goldman, ANZ Price New Issues; Macro; Rating Changes; Gainers and Losers

August 8, 2023

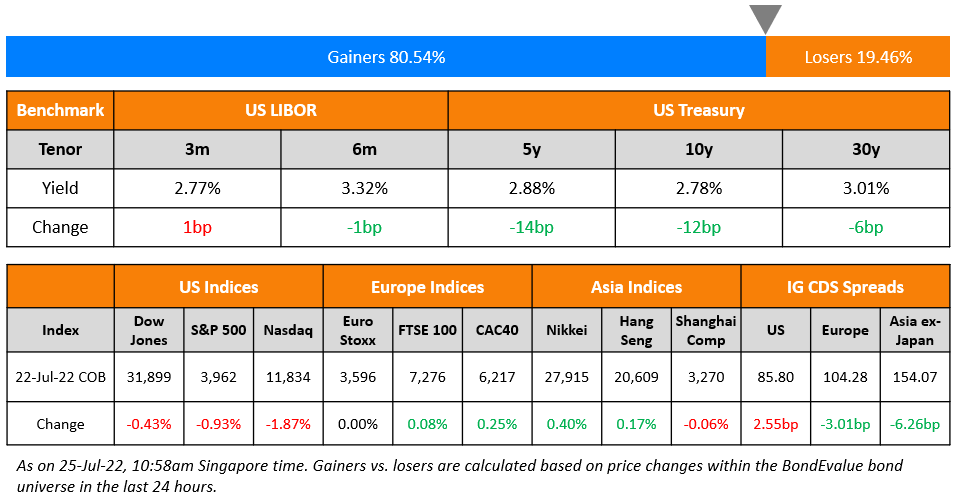

US 2Y Treasury yields were down 5bp while the rest of the curve held stable. Following the large selloff in US Treasuries last week, Goldman Sachs and JPMorgan have come out with calls to buy Treasuries. They believe that the sell-off especially in the 10Y and 30Y were overdone. Further, Goldman and Morgan Stanley are bullish on the 30Y inflation-linked bonds while JPMorgan is bullish on the 5Y note. US IG credit spreads were tighter by 1.3bp and HY CDS spreads tightened by 6.8bp. The S&P and Nasdaq were higher by 0.6-0.9%.

European equity markets ended mixed. In credit markets, European main CDS spreads were 1bp wider and Crossover CDS widened 5.8bp. Asia ex-Japan CDS spreads tightened by 1.1bp. Asian equity markets have opened mixed this morning.

New Bond Issues

- China Life Insurance $ 10NC5 at 5.8% area

HSBC raised $3bn via a two-tranche TLAC deal. It raised $2.3bn via a 4NC3 bond at a yield of 5.887%, 25bp inside initial guidance of T+170bp area. It also raised $700mn via a 4NC3 FRN at a yield of 6.905%. If uncalled after 3 years, the coupon on the fixed rate 4NC3s will reset at the overnight SOFR+157bp and will be paid quarterly thereafter. The new bonds offer a new issue premium of 7.7bp over its existing 2.251% 2027s (callable in 2026) that yield 5.81%. The FRN’s coupon will be reset at the overnight SOFR+157bp and will be paid quarterly. The senior unsecured bonds have expected ratings of A3/A-/A+. Proceeds will be used for general corporate purposes.

OCBC raised S$550mn via a PerpNC5.5 AT1 bond at a yield of 4.5%, 25bp inside initial guidance of 4.75% area. If uncalled, the coupon will reset at the first reset date and every 5 years thereafter at the SGD 5Y swap rate plus 133.48bp. The new AT1s have a write-off clause which may be triggered if the MAS deems the issuer non-viable and/or if MAS makes a public sector injection of capital or support without which the issuer would have become non-viable. The bonds have expected ratings of Baa1/BBB-/BBB+. Proceeds will be used for general corporate purposes. The new bonds are priced 3bp wider to its existing 3% AT1s, callable in 2030 that yield 4.47%. This is the first SGD-denominated AT1 since the write-down of Credit Suisse’s AT1s in March.

Goldman Sachs raised $2.75bn via a two-part deal. It raised $2.25bn via a 3NC2 bond at a yield of 5.798%, 22bp inside initial guidance of T+125bp area. It also raised $500mn via a 3NC2 FRN bond at a yield of 6.4%. If uncalled after 2 years, the coupon will reset at the overnight SOFR+107.5bp and will be paid quarterly thereafter. The new bonds are priced 1.2bp tighter to its existing 0.855% 2026s (callable in 2025) that yield 5.81%. The FRN’s coupon will be reset at the overnight SOFR+106.5bp and will be paid quarterly. The senior unsecured bonds have expected ratings of A2/BBB+/A. Proceeds will be used for general corporate purposes.

ANZ NZ raised $1bn via a 5Y bond at a yield of 5.355%, 25bp inside initial guidance of T+145bp area. The senior unsecured bonds have expected ratings of A1/AA-/A+. Proceeds will be used for general corporate purposes. The new bonds offer a new issue premium of 5.5bp over its existing 3.45% 2028s that yield 5.3%.

Rating Actions

- Moody’s upgrades Rio Tinto to A1; outlook stable

- Jefferies Finance LLC Outlook Revised To Negative On Increased Consolidated Leverage; ‘BB-‘ Ratings Affirmed

- Moody’s changes Aston Martin’s outlook to positive from stable; Caa1 ratings affirmed

Term of the Day

Blue Bond

Blue bonds are a type of sustainable debt wherein the proceeds from such issuance are earmarked for marine/water projects related to ocean conservation (hence the name blue bonds). These are similar to green bonds, which are earmarked for green or environmentally-friendly projects. Blue bonds became popular in late 2018 when Seychelles issued the world’s first sovereign blue bond.

Gabon priced a $500mn 15Y blue bond at 200bp over the US 10Y Treasury.

Talking Heads

On China Bonds Are Clear Winners With More Easing – Invesco

Freddy Wong, head of APAC Fixed Income

“When you lack growth, and you are slowly stimulating, allowing an interest-rate environment to keep rates lower for longer, this is why the China trade has been very obvious… We believe sell-side’s forecast on Chinese economic growth was too optimistic at that time. As such, we turned more bullish on CNY rates”

On Hedge Funds Boosting Record Treasury Shorts as Markets Convulsed

Naokazu Koshimizu, senior rates strategist at Nomura

“Short positions in these few years seem to be largely due to the futures basis trade”… selling may continue “unless there is a huge disruption in the Treasury market which deteriorates the basis trade… Once the Fed stops raising interest rates, the next step must be cutting”

On Climate change putting sovereigns at downgrade risk -Patrycja Klusak Study

“Our results support the idea that deferring green investments will increase costs of borrowing for nations, which will translate into higher costs of corporate debt… There are no winners”

On Pemex Bond Investors Getting Tired of AMLO’s Band-Aid Fixes

Edwin Gutierrez, money manager at Abrdn

“This administration really is not making a concerted effort to address investor concerns… good news in the near term as it clarifies any uncertainty over short-term financing. But obviously these governance issues will continue to weigh on the company.”

Claudia Calich, the head of EM debt at M&G Investments

“Some of the spread volatility is reflecting risks ahead for the election. It’s difficult because it’s a bit of the ‘chicken or the egg’ — who do you blame? Do you blame the company for not being more efficient or do you blame the Mexican government?”

Top Gainers & Losers- 08-August-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.