This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

IRB Infra Launches $ 8Y; US Averts Govt Shutdown

February 29, 2024

US Treasury yields were marginally lower across the curve, down by 1-3bp. US 4Q 2023 GDP (second estimate) came in slightly lower at 3.2% than the preliminary estimate of 3.3%. Also, the US congress reached a deal to provide one week of temporary funding to avert a partial government shutdown on March 2. New York Fed President John Williams said that more work was required to get inflation back to 2%, adding that the Fed “has the time” to take in data before making the call to cut rates. Separately, Boston Fed President Susan Collins repeated that “it will likely become appropriate to begin easing policy later this year”. Looking at credit markets, US IG CDS spreads widened 1.1bp and HY CDS spreads were 5bp wider. Equity markets closed lower with the S&P and Nasdaq down 0.2% and 0.6% respectively.

European equity markets ended lower. Credit markets in the region saw the European main CDS spreads stay flat while crossover spreads widened slightly by 0.3bp. Asian equity markets have opened in the green today. Asia ex-Japan IG CDS spreads were 1.3bp wider. The Hong Kong government has lifted several housing market tightening measures including scrapping of all extra stamp duties, easing mortgage rules etc. to aid their residential property market, as per its budget announcement.

New Bond Issues

- IRB Infra $ 8Y at 7.5% area

.png)

NatWest raised $1bn via a 10.25NC5.25 Tier 2 bond at a yield of 6.475%, 25bp inside initial guidance of T+245bp area. The SEC-registered subordinated bonds are rated Baa1/BBB-/BBB+. The first call date on the notes occurs on 1 June 2029 and if not redeemed, the coupon resets to the 5Y CMT plus 220bp. NatWest’s new bonds offer a yield pick-up of 47.5bp over Westpac’s 4.11% Tier 2 note due 2034 (callable in July 2029) and CBA’s 3.61% Tier 2 note due 2034 (callable in September 2029) that are both rated Baa1/BBB+/A- and currently yield 6%. NatWest’s new bonds also offer a yield pick-up of 44.5bp over NAB’s 3.933% Tier 2 note due 2034 (callable in August 2029) that are rated Baa1/BBB+/A- and currently yield 6.03%.

Mapletree Pan Asia Commercial Trust raised S$200mn via a 10Y green bond at a yield of 3.90%, 25bp inside initial guidance of 4.15% area. The senior unsecured notes are rated Baa1. Proceeds will be used for financing or refinancing, in whole or in part, the eligible green projects in accordance with Mapletree Pan Asia Commercial Trust green finance framework. The issuer is MPACT Treasury Co Pte Ltd.

SuMi Trust raised $2.25bn via a three-part deal. It raised:

- $1bn via a 3Y bond at a yield of 5.234%, 25bp inside initial guidance of T+105bp area

- $750mn via a 5Y bond at 5.221%, 25bp inside initial guidance of T+120bp area

- $500mn via a 10Y at a yield of 5.362%, 25bp inside initial guidance of T+135bp area

The senior unsecured notes are rated A1/A. Proceeds will be used for general corporate purposes.

Citigroup raised $550mn via a PerpNC5 preference share at a yield of 7.2%, 17.5bp inside initial guidance of 7.375% area. The senior unsecured notes are rated Ba1/BB+/BBB-. Proceeds will be used for general corporate purposes including partial/full redemption of outstanding shares of Citigroup preferreds and related depositary shares, and repurchases/redemptions of other outstanding securities of Citigroup and its subsidiaries. The notes have an optional redemption wherein Citigroup may (a) redeem their preferred stock in whole or in part, from time to time, on any dividend payment date on or after the first reset date or (b) in whole but not in part at any time within 90 days following a Regulatory Capital Event.

Metropolitan Bank raised $1bn via a two-trancher. It raised $500mn via a 5Y bond at a yield of 5.403%, 30bp inside initial guidance of T+140bp area. It also raised $500mn via a 10Y bond at a yield of 5.599%, 30bp inside initial guidance of T+160bp area. The senior unsecured notes are rated Baa2. Proceeds will be used for general corporate purposes.

New Bond Pipeline

- Del Monte Philippines hires for $ Perp

Rating Changes

- Fitch Upgrades Costa Rica to ‘BB’; Outlook Stable

- Fitch Downgrades Total Play to ‘CCC+’; Removes Rating Watch Negative

- Fitch Downgrades Ventas’s LT IDR to ‘BBB’ from ‘BBB+’; ST IDR to ‘F3’ from ‘F2’; Outlook Stable

Term of the Day

SEC Registered Bonds

As the name suggests, these are bonds registered with the US Securities and Exchange Commission (SEC). These are not to be confused with 144A bonds, which are privately placed, not SEC registered and have lesser documentation and are traded among Qualified Institutional Buyers (QIBs). Given 144As are restricted securities, they have resale and transfer restrictions that are not applicable for SEC-registered securities. Besides these, they also have a few other differences like being eligible for inclusion in bond indices like Barclays Aggregate Bond Index, no investment restrictions and no private placement restrictions on communications.

Talking Heads

On Pemex’s Bond Bulls Pocketing Gains That Dwarf Rest of Market

Octavio Romero, CEO of Pemex

“Pemex doesn’t understand where Moody’s got its information. It’s irresponsible… has the full support of the Mexican government”

Sergey Goncharov, a money manager at Vontobel Asset Management

“It seems like AMLO 2.0 is the way to think of most political issues — and Pemex specifically”

Andrew De Luca, an EM credit analyst at T. Rowe Price

“Discussions are being held on how to further support Pemex both in the short-term and the long-term

On The Big Bond Steepener Flopping as Fed Delays Rate Cuts

Wood, deputy head of fixed income at Schroders

“The longer the Fed keeps rates restrictive, the more confident we get that growth will moderate at a time when inflation is within target”

GSAM’s Ashish Shah

“We do still like the steepener… inflation “may not be coming down in a straight line, but it is coming down.”

On Banks Needing to Improve Trading Client Risk Controls – ECB

“There are some banks where we see major deficiencies, we don’t see remediation, we don’t see appropriate follow-through… till a few major areas, even the banks that are conducting remediation”

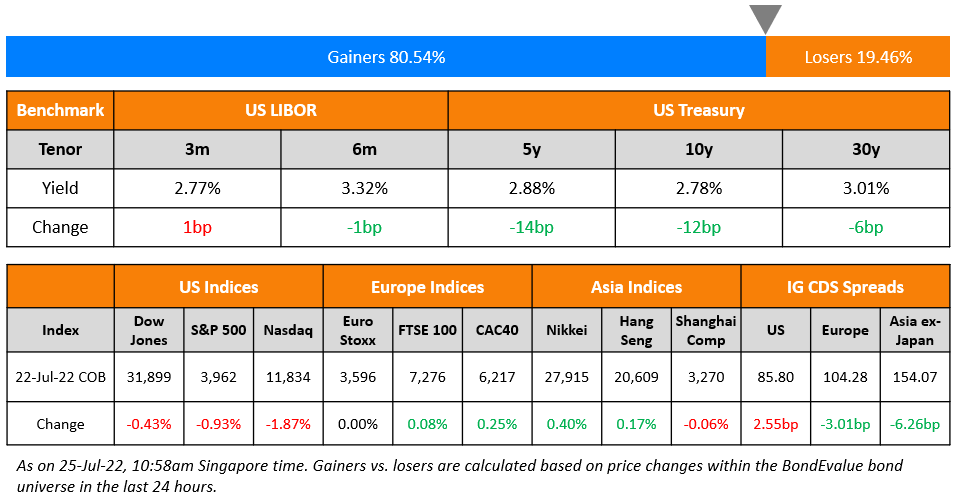

Top Gainers & Losers- 29-February-24*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.