This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

February 22, 2023

US Treasury yields jumped 5-8bp higher across the curve as markets reprice the rate hike path of the Fed. The peak Fed funds rate jumped 5bp to 5.36% for the July 2023 meeting. The S&P US Flash PMIs beat expectations yesterday. The Manufacturing print came at 47.8, beating the surveyed 47.2 and the Services print was at 50.5, significantly beating the exepected 47.3 number. The Services sector recorded its highest level in eight months and has thus gone back into expansion for the first time since June 2022.

Markets are now pricing in a 24% chance of a 50bp hike in March vs. 9% a week ago. Broadly going by the maximum probability of rate hikes, CME probabilities show that markets are now pricing in 25bp hikes at each of the next three Fed meetings in March, May and June. The chance of a 25bp hike in June has is now at 58%. US IG and HY CDS shot higher by 4.2bp and 22.5bp. The S&P and Nasdaq closed lower by 2% and 2.5% on Tuesday, its largest one-day drop this year.

European equity markets also ended lower. The European main CDS spread widened by 3.2bp and the crossover CDS spread widened 15.8bp. Asian equity markets have opened with a negative bias. Asia ex-Japan CDS spreads soared higher by 9bp, its largest one-day move this year.

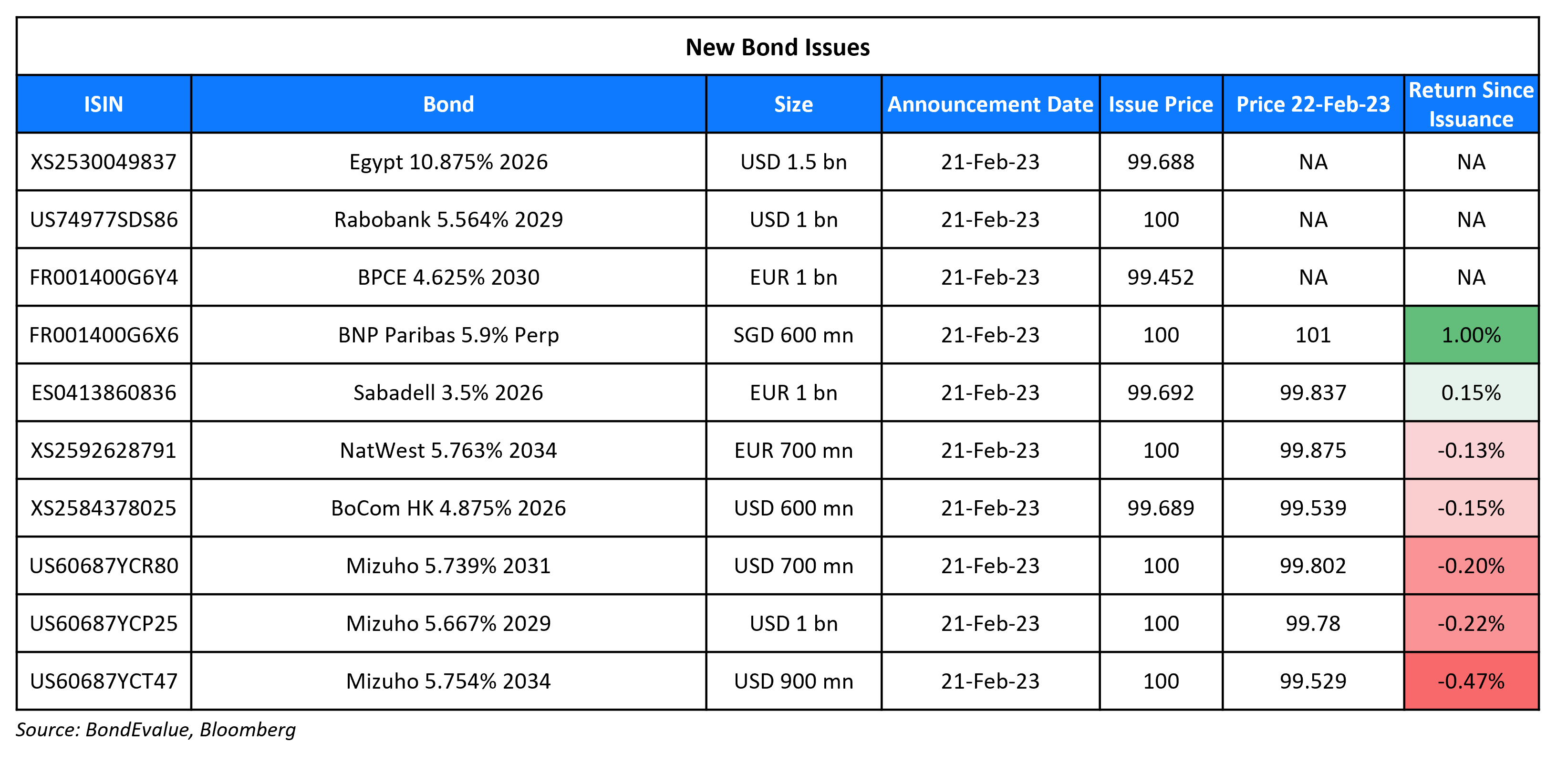

New Bond Issues

BNP Paribas raised S$600mn via a PerpNC5 AT1 bond at a yield of 5.9%, 40bp inside initial guidance of 6.3% area. The notes have expected ratings of BBB-/BBB. Proceeds will be used as AT1 Capital and for general corporate purposes. The current coupon of 5.9% is fixed until the first call date on 28 February 2028 and if not called, the coupon resets every 5 years to the 5Y SORA-OIS plus the initial margin of 267.4bps. The notes may be written down if the issuer’s CET1 ratio falls below 5.125%. The new bonds are priced 148bp wider to UOB’s existing 5.25% Perps (callable in January 2028) that yield 4.42%, and 76bp tighter to Barclays’ existing 8.3% Perps (callable in September 2027 with a reset in December 2027) that yield 6.66%

Egypt raised $1.5bn via a 3Y Sukuk bond at a yield of 11%, 62.5bp inside initial guidance of 11.625% area. The senior unsecured bonds have expected ratings of B3/B. The new bonds are priced 36bp tighter to its existing 3.875% 2026s that yield 11.36%.

Bocom HK raised ~$1.5bn via a three-tranche multi-currency deal. It raised

- $600mn via a 3Y bond at a yield of 4.418%, 43bp inside initial guidance of T+100bp area. The new bonds are priced 78.2bp tighter to its existing 1.2% 2025s that yield 5.2%.

- CNH 3.8bn via a 2Y bond at a yield of 2.97%, 53bp inside initial guidance of 3.5% area.

- HKD 2.7bn via a 2Y bond at a yield of 4.5%, 50bp inside initial guidance of 5% area.

The senior unsecured bonds have expected ratings of A2. Proceeds will be used as working capital and for general corporate purposes.

Rabobank raised $1bn via a 6NC5 bond at a yield of 5.564%, 15bp inside initial guidance of T+155bp area. The senior bonds have expected ratings of A3/A-/A+. Proceeds will be used for general corporate purposes.

New Bonds Pipeline

- HDFC mandates for $ 3Y bond

- Qatar plans for $ bond

- REC hires for $ Long 5Y Green bond

Rating Changes

- Correction: Fitch Downgrades Ghana’s Long-Term Foreign-Currency IDR to ‘RD’

Term of the Day

Schuldschein

Schuldschein (pronounced schuld-shine) is a debt instrument popular with German issuers that is similar to a bond albeit with lower expenses for the issuer. These instruments do not need to be registered at an exchange, thereby reducing documentation and time taken. They are more flexible than a bond, as they can be adjusted to the customer’s needs regarding repayment terms, drawdown periods, etc. and thus have some features of loans. Commerzbank notes that Schuldschein transactions can be arranged very quickly, with a tenor of 2 and 5 years, in order to improve asset-liability management (ALM). Lending can be done by one bank, which might look for participants afterwards.

Porsche raised a massive €2.7bn via a Schuldschein issuance, the largest ever on record.

Talking Heads

On BlackRock ‘overweights’ Treasuries, emerging markets stocks

“Now bond markets are waking up to the risk the Fed hikes rates higher and holds them there for longer… Credit spreads have tightened sharply along with stocks pushing higher, reducing their relative attraction. We remain moderately overweight and still think highly rated companies will weather a mild recession well given stronger balance sheets compared with before the pandemic”

On Goldman Sees Fed Hiking by Further 75 Points on Stronger Growth – Jan Hatzius, Chief Economist

“I don’t think that necessarily breaks the trend toward disinflation but I think it reinforces the idea that the Fed still has work to do… So we think another 75 basis points from here with no cuts until 2024 seems like a more likely outcome… It would be a relatively important step because if they do 50 in March, the market would probably build in at least a decent chance of another 50”

On India Not Keen to Add Debt Securities to Global Indexes, TD Says

“The message that we received was loud and clear; officials and even domestic funds were content with the status quo… However, this doesn’t rule out inclusion as index providers appear keen to include India, and we still may see some progress this year”

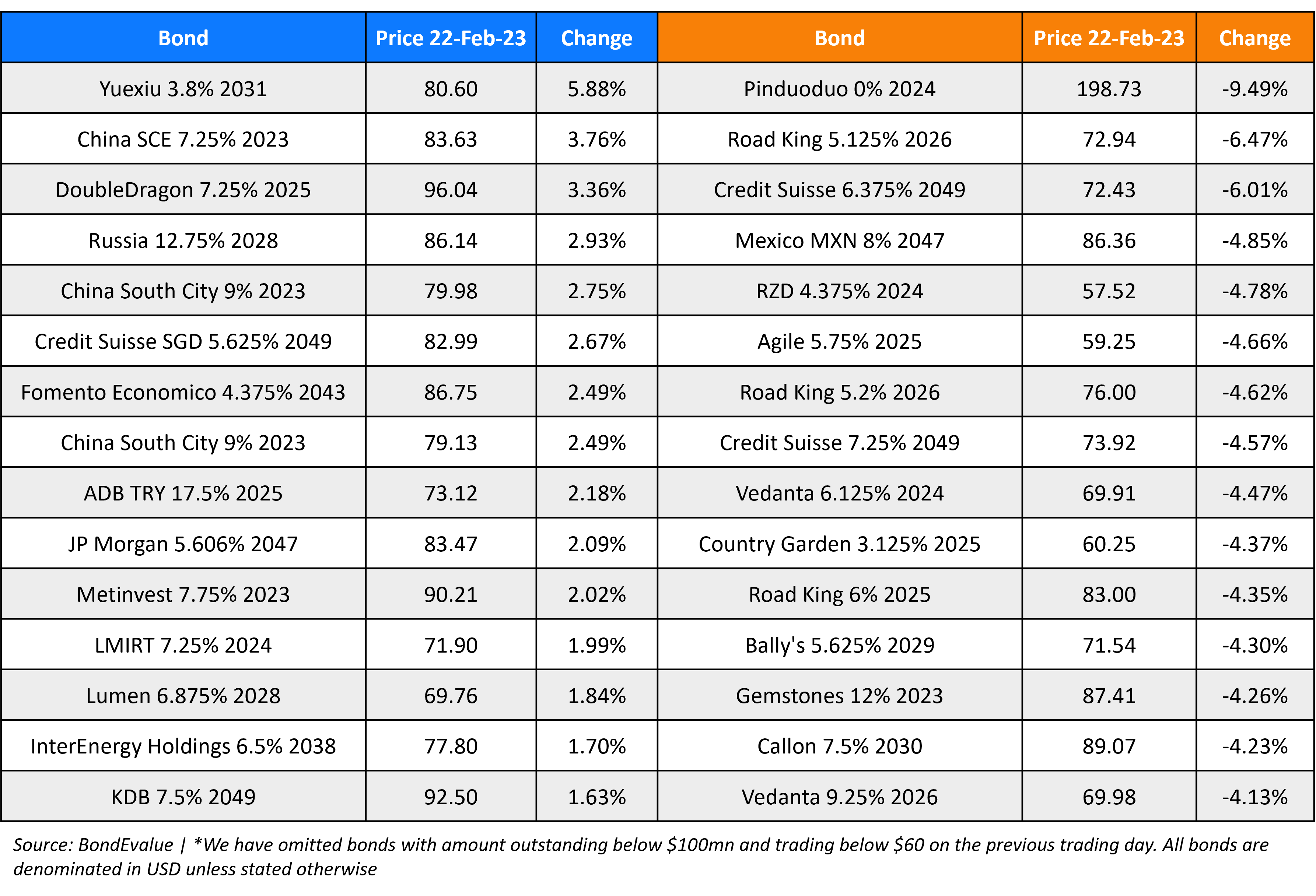

Top Gainers & Losers – 22-February-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.