This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

December 19, 2022

The US Treasury curve steepened with the 2Y yield own 7bp while the 10Y and 30Y yields were up 4-5bp. The peak Fed funds rate was up 1bp to 4.89% for the May 2023 meeting. US flash manufacturing PMI fell to 46.2 in December from 47.7 a month ago with S&P noting that they witnessed “one of the sharpest declines in new orders since the 2008-9 financial crisis during December, as customer spending waned”. The flash services PMI also fell to 44.4 from 46.2. Thus, the composite PMI fell to 44.6, a sixth straight month below the 50 mark, indicating a contraction in the private sector. Markets continue to price in the probability of a 25bp hike at the February 2023 meeting at 73%, little changed from Friday. US IG CDS spreads widened 2.7bp and HY CDS spreads widened 14.9bp. US equity markets fell with the S&P and Nasdaq down 2.5% and 3.2% respectively on Thursday.

European equity markets were lower too. EU Main CDS spreads widened 6.8bp and Crossover spreads widened by 36.7bp. Asian equity markets have opened broadly lower today. Asia ex-Japan CDS spreads widened by 6.4bp.

%20x%20311px%20(h).jpg?upscale=true&upscale=true&width=1400&upscale=true&name=Tablet%20banner%20661px%20(w)%20x%20311px%20(h).jpg)

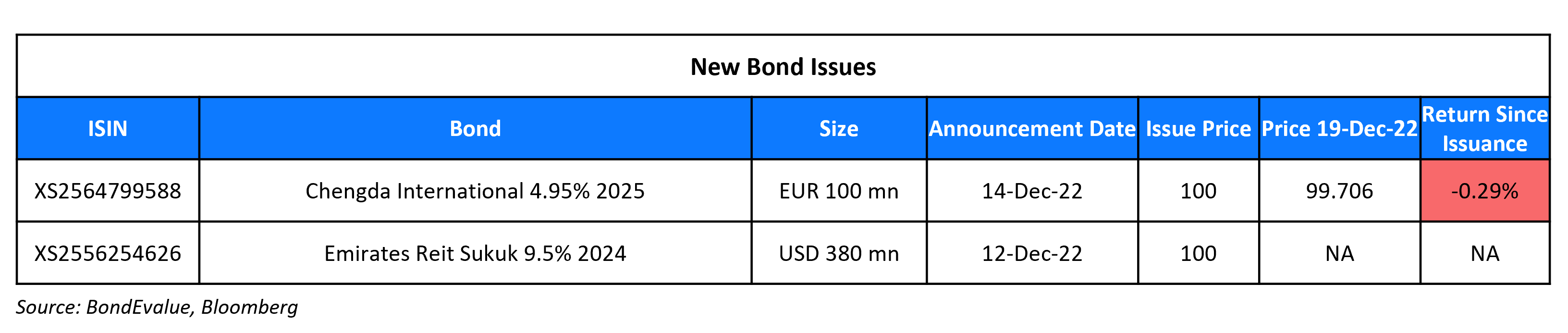

New Bond Issues

New Bonds Pipeline

- Korea Investment & Securities hires for $ Green bond

- Zhongrong International Trust hires for $367mn Short 1Y bond

- TSMC Arizona hires for $ bond

Rating Changes

Term of the Day

Special Drawing Rights (SDR)

Special Drawing Rights (SDR) issued by the IMF to its member countries’ central banks are a reserve asset that can be exchanged for hard currencies with another central bank. The value of an SDR is set daily based on a basket of five major international currencies: the USD (42%), the EUR (31%), the CNY (11%), the JPY (8%) and the GBP (8%). An allocation of SDRs requires approval by IMF members holding 85% of the total votes and US is the biggest holding 16.5% of the votes.

Talking Heads

On Distressed Traders Seeing Bright Spots in Riskiest Emerging Debt

Gabriel Sterne, head of global emerging-markets research at Oxford Economics

“There are plenty of non-defaulted sovereigns with highly elevated spreads, yet few of these sovereigns with elevated spreads face funding cliffs in 2023”

Lupin Rahman, global head of emerging-market sovereign credit at Pimco in London

“We would caution investors against following this siren call of high yield and low bond prices. “There is a lot of risk premium to be harvested in very safe emerging market credits”

On Bond Managers Sensing Opportunity With Yields Below Fed’s Rate

Marion Le Morhedec, global head of fixed income at AXA Investment

“We believe that the outlook for 2023 is starting to brighten”

Andrzej Skiba, head of the BlueBay US fixed income team at RBC Global Asset Management

A 10-year at 3.5% does look a little too low, but at the same time it’s difficult to see upward pressure on government bond yields when inflation is starting to co-operate”

On Bonds Getting a Wake-Up Call From ECB Warning

Ralf Preusser, global head of rates strategy at Bank of America Securities

“It’s a lot less controversial now to not only see European yields reset higher in absolute terms, but we also see European rates markets underperform the US very meaningfully throughout all of 2023”

Mohit Kumar, a rates strategist at Jefferies

“Overly aggressive monetary policy risks engineering a sharper recession and widening of peripheral spreads, which will raise fragmentation risks”

On Credit Investors Getting Ahead of Themselves

Martin Hasse, MM Warburg & Co.’s

“The entry point will be better in the second half. The market does not price in risks related to recession and we see a widening of spreads in the first half”

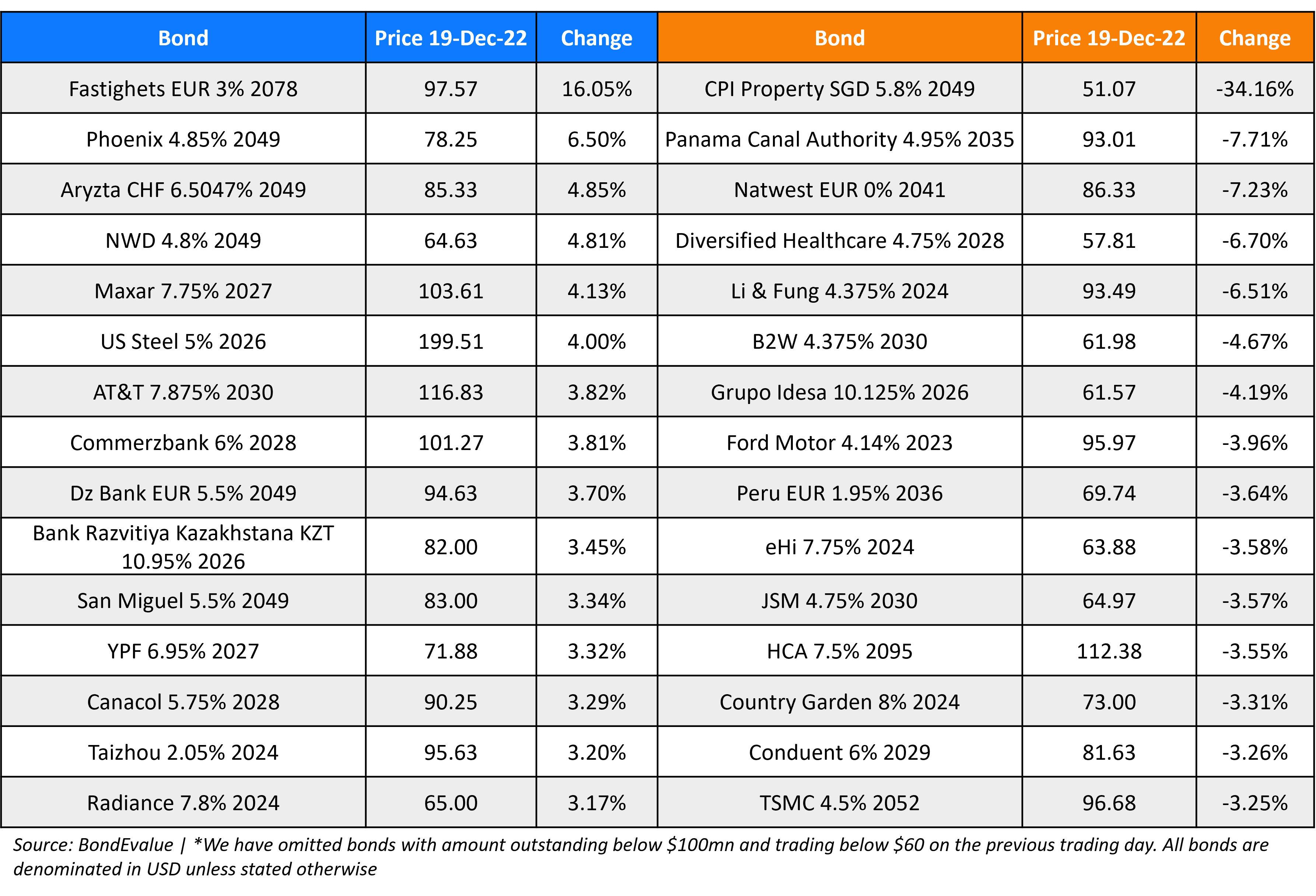

Top Gainers & Losers – 19-December-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.