This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

UOB Launches S$ PerpNC5; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

January 12, 2023

US Treasury yield were lower by 7-9bp across the 5Y to the 30Y while 2Y yields were down 3bp. The peak Fed funds rate was up 1bp to 4.94% for the June 2023 meeting. Markets keenly await the US inflation data prints later today – Headline CPI is expected to soften to 6.5% in December from 7.1% in November. Core CPI is also expected to soften to 5.7% from 6%. The probability of a 25bp hike at the FOMC’s February 2023 meeting stands at 77% vs. 80% yesterday. US equity markets ended higher with the S&P up 1.3% and Nasdaq up 1.8%. US IG and HY CDS spreads were 2.5bp and 16.3bp tighter.

European equity markets ended lower. The European main and crossover CDS spreads tightened by 1.8bp and 10bp respectively. The European primary markets are having a record start to the year with new deals of over $150bn priced so far. Asian equity markets have opened lower today. Asia ex-Japan CDS spreads tightened by 4.5bp.

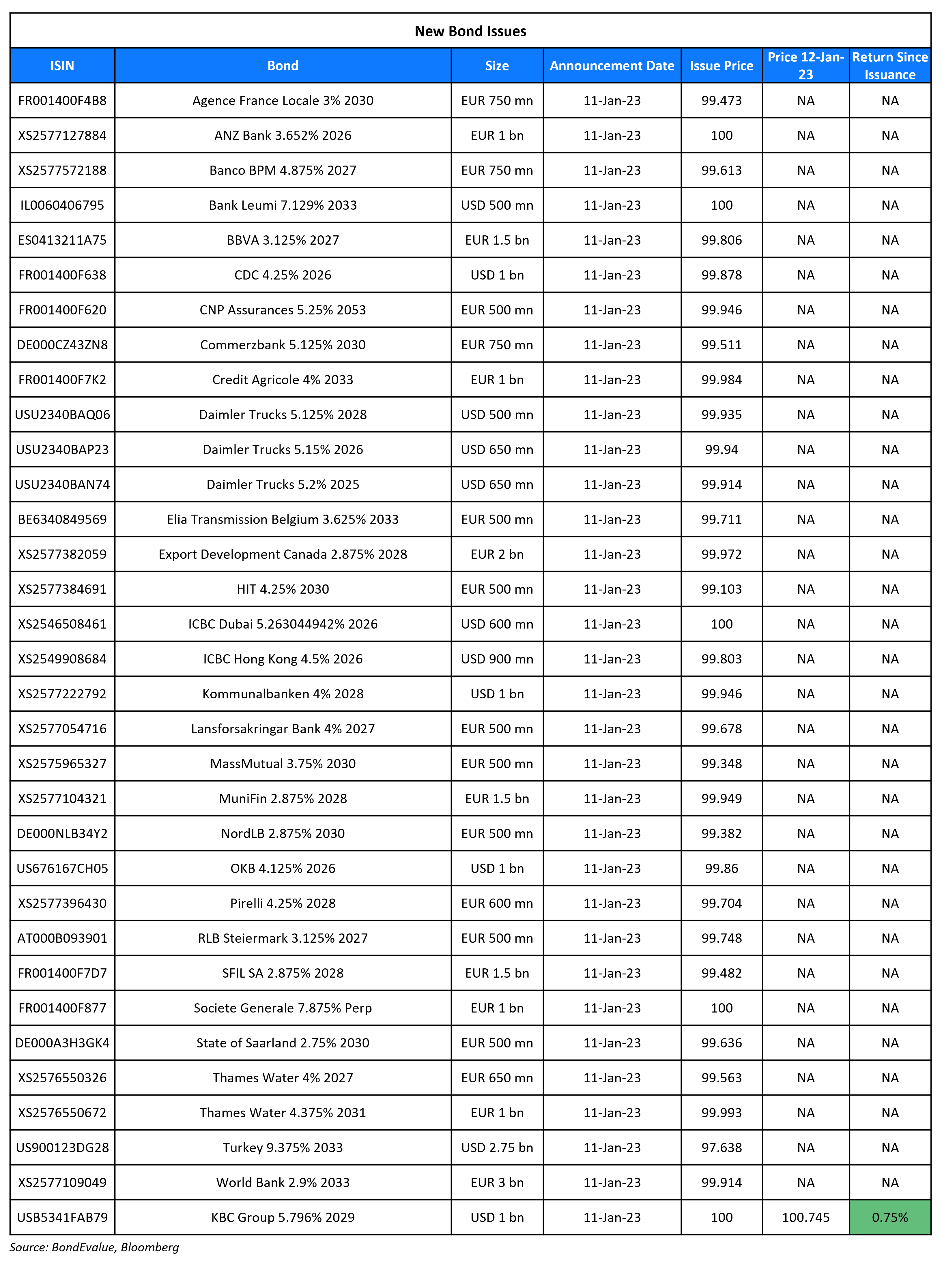

New Bond Issues

- Taian City Development and Investment $ 364-day at 8% area

- UOB S$ PerpNC5 at 5.25% area

Turkey raised $2.7bn via a 10Y bond at a yield of 9.75%, 37.5bp inside initial guidance of 10.125% area. The senior unsecured bonds are rated B3/B (Moody’s/Fitch). The new bonds were priced at a new issue premium of 63bp over its older 6.5% bonds due September 2033 that yield 9.12%.

SocGen raised €1bn via a PerpNC6.5 AT1 bond at a yield of 7.875%, 50bp inside initial guidance of 8.375% area. The AT1 bonds (Term of the Day, explained below) are rated Ba2/BB/BB+, and received orders over €4.5bn, 4.5x issue size. The coupons are payable annually and are fixed until the first reset date of 18 July 2029. The bonds are callable at any date in the six month period preceding (and including) the first reset date. If not called, the coupon resets every five years at the 5Y MS+522.8bp and the payment frequency changes from an annual to a semi-annual basis. A trigger event would occur if the group’s consolidated CET1 ratio falls below 5.125%.

ICBC raised $1.5bn via a two-tranche deal from two of its branches:

- ICBC Hong Kong branch raised $900mn via a 3Y green bond at a yield of 4.504%, 49bp inside initial guidance of T+110bp area. The new bonds are priced 24.6bp tighter to its existing 1.2% bonds due July 2025 that yield 4.74%.

- ICBC Dubai branch raised $600mn via a 3Y green FRN at a yield of 5.246%, 47bp inside initial guidance of SOFR+140bp area.

The senior unsecured bonds have expected ratings of A1 by Moody’s. Proceeds will be used to (re)finance eligible green assets.

Credit Agricole raised €1bn via a 10Y bond at a yield of 4.002%, 25bp inside initial guidance of MS+145bp area. The senior preferred bonds have expected ratings of Aa3/A+/AA-. The new bonds are priced at a new issue premium of 30.2bp over its existing 2.5% bonds due August 2029s that yield 3.7%.

Commerzbank raised €750mn via a 7NC6 bond at a yield of 5.222%, 30bp inside initial guidance of MS+270bp area. The bonds are rated Baa2/BBB-, and received orders over €4.1bn, 5.5x issue size.

New Bonds Pipeline

- Woori Bank hires for $ 3Y Sustainability or 5Y Sustainability bond

Rating Changes

Term of the Day

AT1 Bonds

Additional Tier 1 (AT1) bonds are hybrid securities issued by financial institutions to meet their regulatory capital requirements. AT1s typically carry a provision wherein the instruments can be fully or partially written-down or converted to equity if the issuing bank’s capital ratio falls below a certain threshold. This is why AT1s are also known as contingent convertibles (CoCos). The key characteristics of AT1 bonds are: They have a perpetual maturity with a call option They are subordinated in nature, and the first line of debt to incur losses They can be written-down or converted into equity on the occurrence of a “trigger event” Coupons are usually higher as compared to other debt by the issuer, to compensate investors for the higher risk AT1s carry. However, coupons can be discretionary in nature.

For a complete guide to AT1s, click here

Talking Heads

On Pimco Says ‘Bonds Are Back’ With Recession Likely This Year

Baseline outlook for “a modest recession and moderating inflation… the potential for both attractive returns and mitigation against downside risks… may offer additional downside mitigation versus outer-circle assets in the event of worse outcomes… underweight duration in many portfolios. This reinforces the case for being overweight the Japanese yen, which we see as cheap in our valuation models and a position we would expect to benefit in a deeper-than-anticipated recession”

On Fed’s No-Rate-Cut Mantra Rejected by Markets Seeing Recession

Marc Chandler, chief market strategist at Bannockburn Global

“The market thinks the Fed is playing without a playbook, since their forecasts have been wrong before and they’ve downplayed them in the past… headed for a recession, and that the Fed doesn’t quite yet get it.”

Ed Yardeni, Founder of Yardeni Research

“Fed officials have turned more hawkish because investors aren’t listening to their warnings. Perhaps, Fed officials should listen to the bond market”

On ECB needing several more significant rate hikes – Finland Central Bank Chief, Olli Rehn

“Policy rates will still have to rise significantly. This means significant rate hikes at this winter’s remaining meetings”

On Complex Debt Talks With Ghana Political Upheaval

Mark Bohlund, a senior credit research analyst at REDD Intelligence

“You could definitely argue that external bondholders would be better off seeking to close a restructuring deal with the current government. However, there’s likely to be enough opposition among creditors to frustrate such a process with many wary that whatever is agreed with the current government is unlikely to be upheld were there to be a shift in political power at the next elections.”

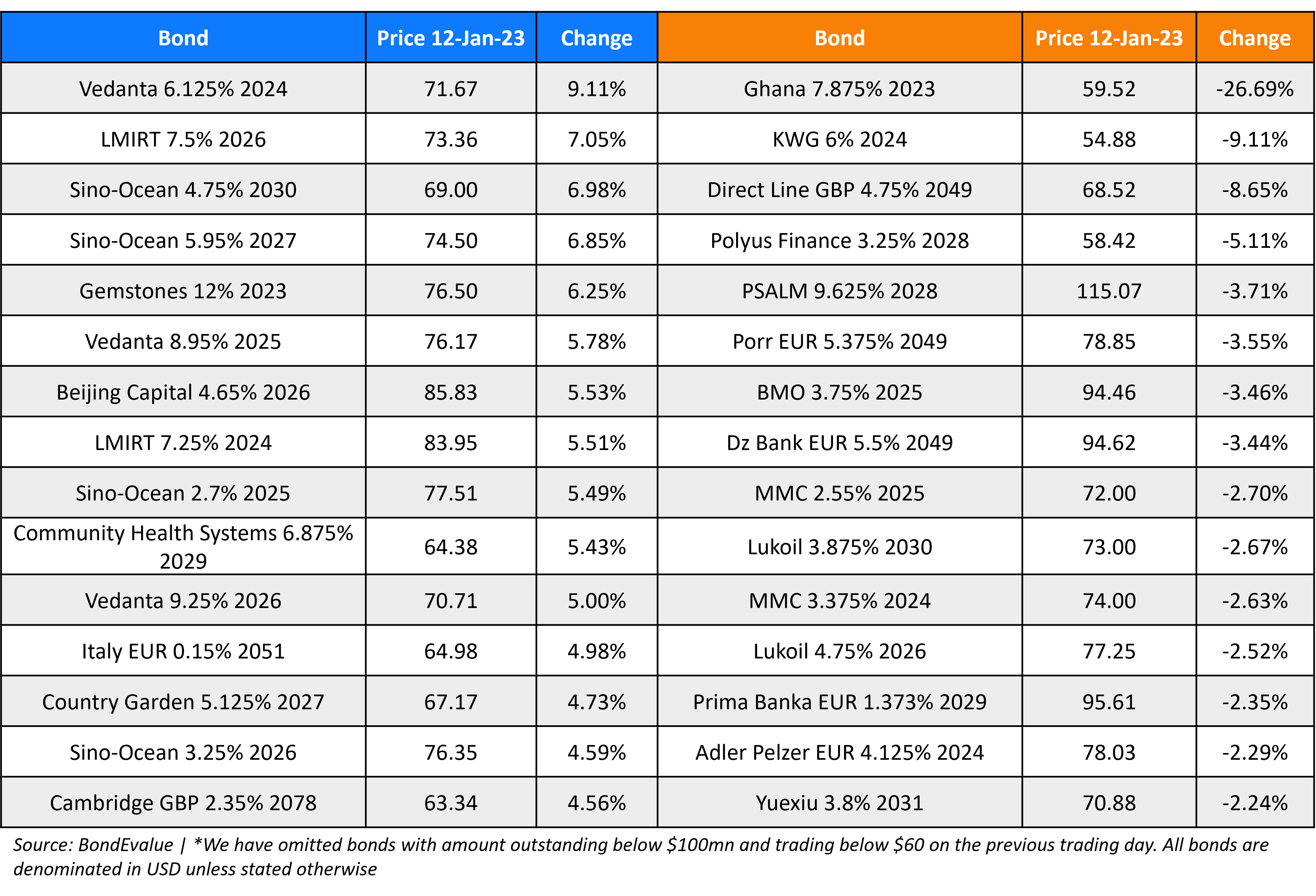

Top Gainers & Losers – 12-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.