This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

January 13, 2023

US Treasury yields were lower by 4-8bp across the curve and the peak Fed funds rate was down 2bp to 4.92% for the June 2023 meeting. The rally came on the back of US CPI coming in at 6.5% for December, in-line with expectations of 6.5% and lower than last month’s 7.1% print. Core CPI also came in-line with estimates at 5.7% and lower than last month’s 6% print. The probability of a 25bp hike at the FOMC’s February 2023 meeting now stands at 92% vs. 77% yesterday. US equity markets ended higher with the S&P up 0.3% and Nasdaq up 0.6%. US IG and HY CDS spreads were 1.5bp and 11.4bp tighter.

European equity markets ended lower. The European main and crossover CDS spreads tightened by 2.1bp and 5.8bp respectively. Asian equity markets have opened higher today. Asia ex-Japan CDS spreads tightened by 4.6bp.

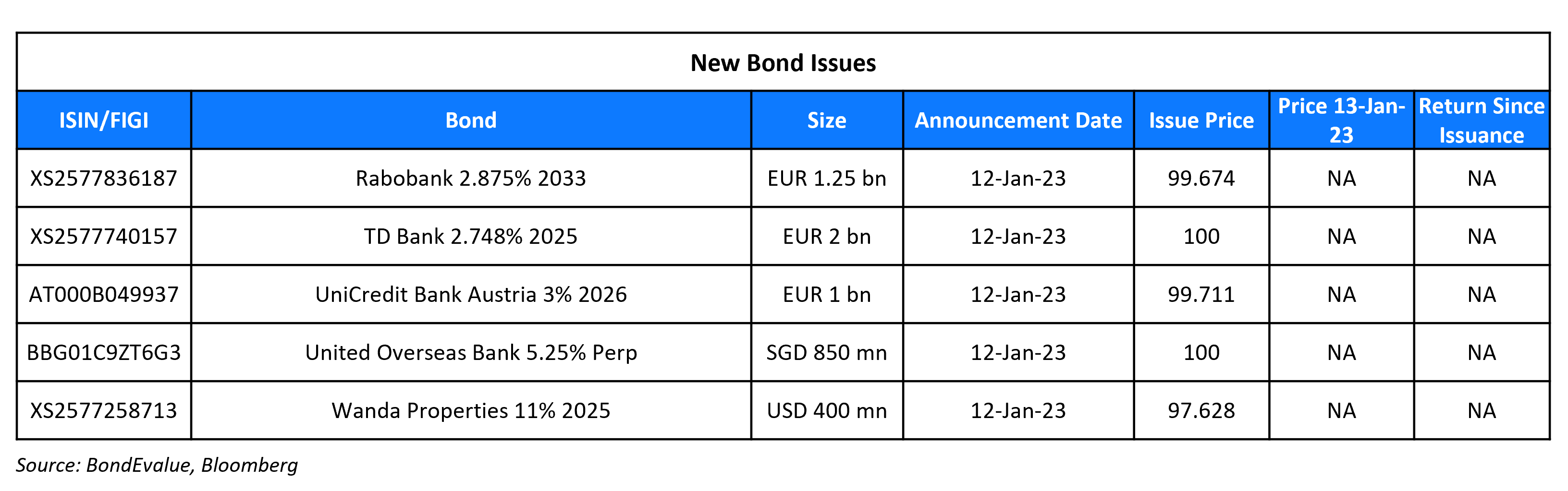

New Bond Issues

UOB raised S$850mn via a PerpNC5 AT1 at a yield of 5.25%, unchanged from initial guidance. The subordinated unsecured notes have expected ratings of Baa1/BBB+. Proceeds will be used for refinancing existing debt and general corporate purposes. If not called on the first call date of 19 January 2028, the bonds will reset then and every 5Y thereafter at the SORA-OIS plus a spread of 239.3bp. The AT1s received orders of over S$2.1bn, with a bid-to-cover ratio (Term of the Day, explained below) of 2.5x. Private banks and securities houses took 85%, followed by fund managers/insurance at 13% and banks/hedge funds/corporates at 2%. The new AT1s offer a new issue premium of 26bp over its older 2.55% Perps callable in June 2028 that are currently yielding 4.99%.

Dalian Wanda raised $400mn via a 2Y bond at a yield of 12.375%, 25bp inside initial guidance of 12.625% area. The bonds are expected to be rated Ba3/BB (Moody’s/Fitch). Wanda Properties Global is the issuer and guarantees will be provided by Wanda Commercial Properties (Hong Kong), Wanda Real Estate Investments and Wanda Commercial Properties Overseas together. Dalian Wanda will also provide a keepwell deed. Proceeds will be used for refinancing existing debt and general corporate purposes. The bonds received final orders of $1.4bn, 3.5x issue size. Asian investors took 81% with EMEA at 19%. By investor type, asset managers took the lion’s share at 97%, with insurance/pension funds/corporates and private banks taking 2% and 1% respectively. A private banker told IFR, “None of my clients put in orders to buy Wanda Commercial…We sold all of our property exposure last year, and clients are very selective with property names.”

The new bonds are priced 145.5bp wider to its existing 7.25% 2024s that yield 10.92%. This is the first Chinese high yield issuer to tap the dollar bond markets since May 2022, when Seazen priced a small deal.

Taian City Development and Investment raised $mn via a 364-day bond at a yield of %, bp inside initial guidance of 8% area.

New Bonds Pipeline

- Khazanah Nasional Bhd hires for $ bond

- Philippines hires for retail $ bond

- Woori Bank hires for $ 3Y Sustainability or 5Y Sustainability bond

Rating Changes

- Sweden-Based Stena AB Upgraded To ‘BB-‘ On Strong Performance; Outlook Stable

- Fitch Downgrades 10 Sri Lankan Banks’ Ratings

- Moody’s places Lippo Karawaci’s ratings on review for downgrade following announcement of tender offer

Term of the Day

Bid-to-cover Ratio

Bid-to-cover is a ratio of the number of bids or orders received for a particular security issuance vs. the amount issued. The bid-to-cover ratio indicates the demand for an issuance – higher the ratio, higher the demand and lower the ratio, lower the demand.

UOB raised S$850mn via an AT1 PerpNC5 at 5.25% on Thursday, which had a bid-to-cover ratio of 2.5x.

Talking Heads

On Downshifting to 25 Basis-Point Interest Rate Hikes

Federal Reserve Bank of Philadelphia leader Patrick Harker

““I expect that we will raise rates a few more times this year, though, to my mind, the days of us raising them 75 basis points at a time have surely passed. In my view, hikes of 25 basis points will be appropriate going forward…At some point this year, I expect that the policy rate will be restrictive enough that we will hold rates in place to let monetary policy do its work…I’ve been in the camp that we need to get rates above 5%…I don’t think we need go much further than 5%…What’s encouraging is that even as we are raising rates, and seeing some signs that inflation is cooling, the national economy remains relatively healthy overall…On the hiring front, I’m most pleased that the labor market remains in excellent shape.”

On Keeping 2023’s Global Growth Forecast Steady at About 2.7%

IMF Managing Director Kristalina Georgieva

“Growth continues to slow down in 2023…The more positive piece of the picture is in the resilience of labor markets. As long as people are employed, even if prices are high, people spend … and that has helped the performance…We are now in a more shockprone world and we have to be open-minded that there could be a risk turn that we are not even thinking about. That’s the whole point of the last years. The unthinkable has happened twice.”

On Cooler Inflation Mixed with Strong Labor Data

Zhiwei Ren, portfolio manager at Penn Mutual Asset Management

“Even though everything is coming in line with expectations, equities are still disappointed because people were expecting a below-expectations CPI report, and that didn’t happen.”

Priya Misra, global head of rates strategy at TD Securities

“The easy part of the decline in inflation may be underway — goods inflation is declining, commodity prices are falling…The much harder part is getting that service inflation down consistent to 2%.”

Maria Vassalou, CIO of multi-asset solutions at Goldman Sachs Asset Management

“The market has priced in a very optimistic scenario about CPI in the previous days. The numbers came in at exactly the expectations level. That means that some of the optimism in the markets may get unwound both in equities and fixed income….While a 25bps hike in the next Fed meeting is still in play, the strength of housing in the core CPI and the benign jobless claims support the scenario of a 50bps hike in the next meeting. However, what matters most for the markets is the terminal Fed rate, not so much the pace of hikes. As we get closer to the terminal rate, the pace of hikes needs to slow down.”

Timothy Graf, head of macro strategy for EMEA at State Street Bank & Trust

“This is continued decent news in terms of the broader inflation trend, but that the stickiness in shelter-related inflation and services inflation means inflation here isn’t coming down fast enough for the Fed’s liking…The Fed should have reason to step down to 25bps at some future meeting and then pause shortly thereafter. I think what this number does is probably extend that time horizon a bit.”

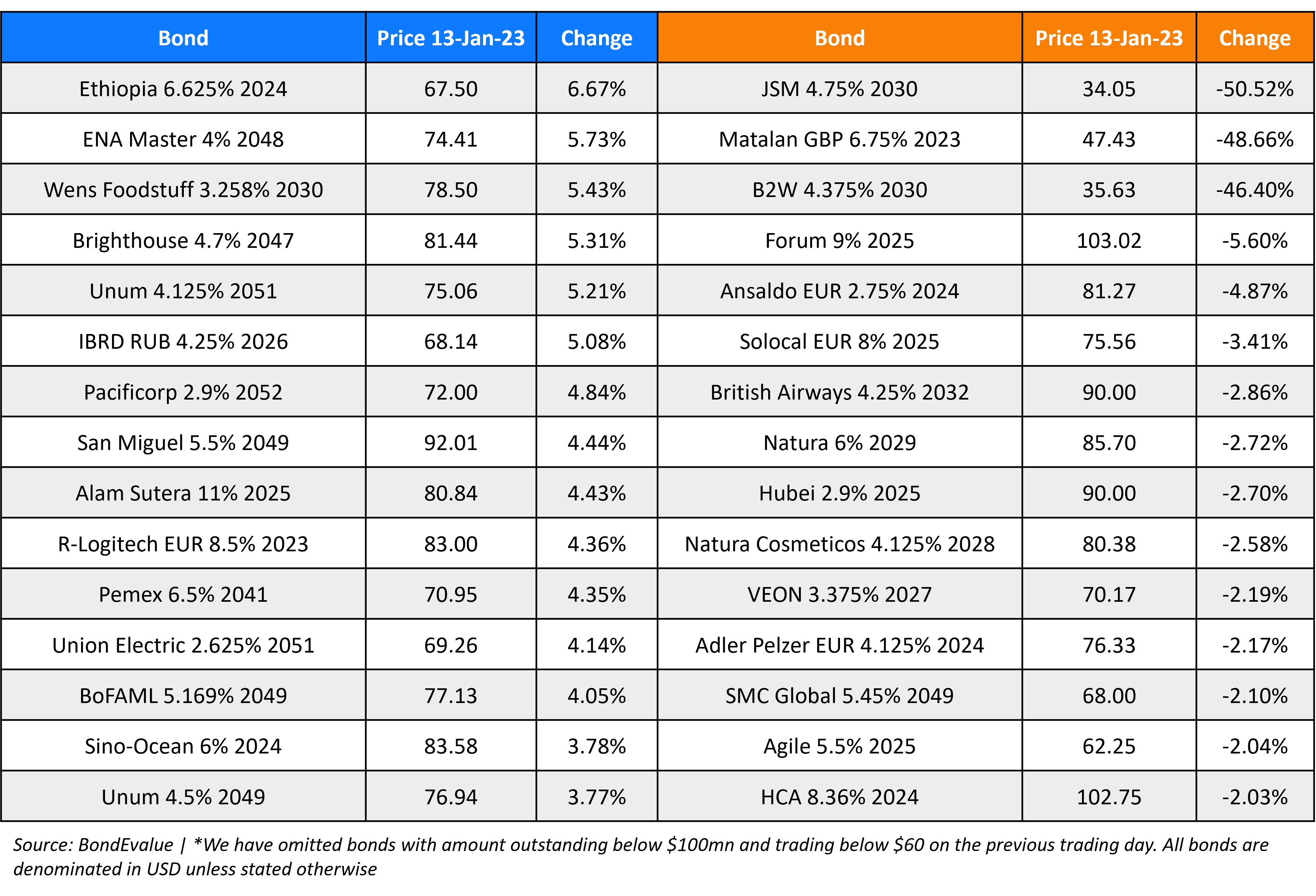

Top Gainers & Losers – 13-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.