This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

January 25, 2023

US Treasury yields were slightly lower across the curve on Tuesday. The peak Fed funds rate was 1bp higher at 4.91% for the June 2023 meeting. The probability of a 25bp hike at the FOMC’s February 2023 meeting stands at 97%. US S&P flash manufacturing PMI came at 46.8, and its services PMI was at 46.6 in January, indicating another month of contraction. US equity markets ended slightly lower with the S&P and Nasdaq down 0.1% and 0.3%. US IG CDS spreads tightened by 0.4bp and HY spreads were 2.6bp tighter.

European equity markets ended flat. The European main and crossover CDS spreads widened by 0.5bp and 3.9bp respectively. Asian equity markets have opened higher today. Asia ex-Japan CDS spreads were flat.

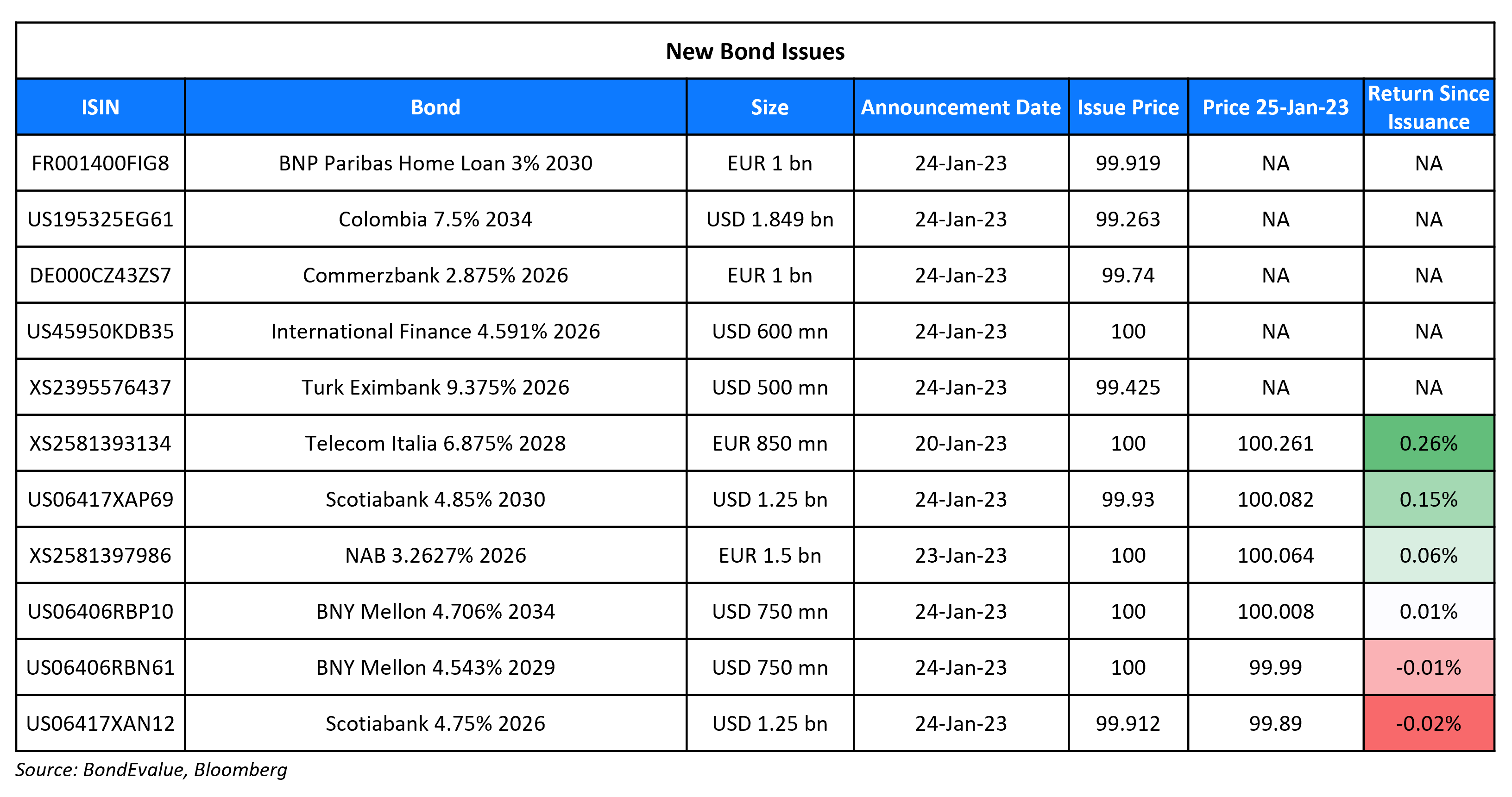

New Bond Issues

Scotiabank raised $2.5bn via a two-tranche deal. It raised

- $1.25bn via a 3Y bond at a yield of 4.782%, 22bp inside initial guidance of T+115bp area. The new bonds are priced 12.8bp tighter to its existing 4.5% bonds due December 2025 that yield 4.91%.

- $1.25bn via a 7Y bond at a yield of 4.862%, 25bp inside initial guidance of T+160bp area.

The senior unsecured bonds have expected ratings of A2/A-/AA-. Proceeds will be used for general corporate purposes.

Commerzbank raised €1bn via a 3.25Y bond at a yield of 2.963%, 5bp inside initial guidance of MS+2bp area. The covered bonds have expected ratings of Aaa, and received orders over €2.2bn, 2.2x issue size.

Colombia raised $1.8bn via a 11Y bond at a yield of 7.65%, 35bp inside the initial guidance of 8% area. The senior unsecured bonds have expected ratings of Baa2/BB+/BB+. Proceeds will be used for general budgetary purposes. The new bonds are priced at a new issue premium (Term of the day, explained below) of 31bp vs. its existing 8% bonds due April 2033 that yield 7.34%.

Term of the Day

New Issue Premium

A new issue premium refers to the incremental higher yield (yield premium) on an issuer’s newly issued bond over bonds by the same issuer with a similar maturity. A newly issued bond by an issuer typically offers a higher yield to its own comparable bond to entice investor demand in the security. Sometimes, if an issuer does not have a comparable bond with a similar maturity, but does have a yield curve (i.e., other bonds issued across different maturities), analysts can interpolate and arrive at an estimated yield for a hypothetical comparable. However, while new issue premiums are typically the case, it is not necessary that an issuer’s new bond would always have a new issue premium.

Talking Heads

On Bond Traders Hedging Prospects That This May Be Fed’s Last Hike

Ian Lyngen, the head of US rates strategy at BMO Capital Markets

“Given the timing of the window between the February and March FOMC meetings, the Fed will have a much greater understanding of the performance of the US economy when it meets late in Q1”

On Debt-Limit Fighting Risks of Early End to Fed QT

Blake Gwinn, head of US rates strategy at RBC Capital Markets

“It’s a complicating factor — because we just don’t know how all these things are going to net out against each other. There’s really two major sources of uncertainty around this process. We don’t know what the right level of reserves is”

On Fed needs mortgage-backed securities exit plan ‘earlier than later’ – Fed’s Esther George

“You can’t just wake up one day and say, ‘hey, we’re going to get out of this business… At some point people will have to address: is that the footprint we want in the mortgage market?… I’ve never felt comfortable saying we should want inflation”

On China’s Actions Delaying Zambia Debt Deal – David Malpass, President of World Bank

“China is asking lots of questions in the creditors committees, and that causes delays, that strings out the process… It’s important for them to be focused on getting to an actual debt restructuring where the burden can be lightened for Zambia”

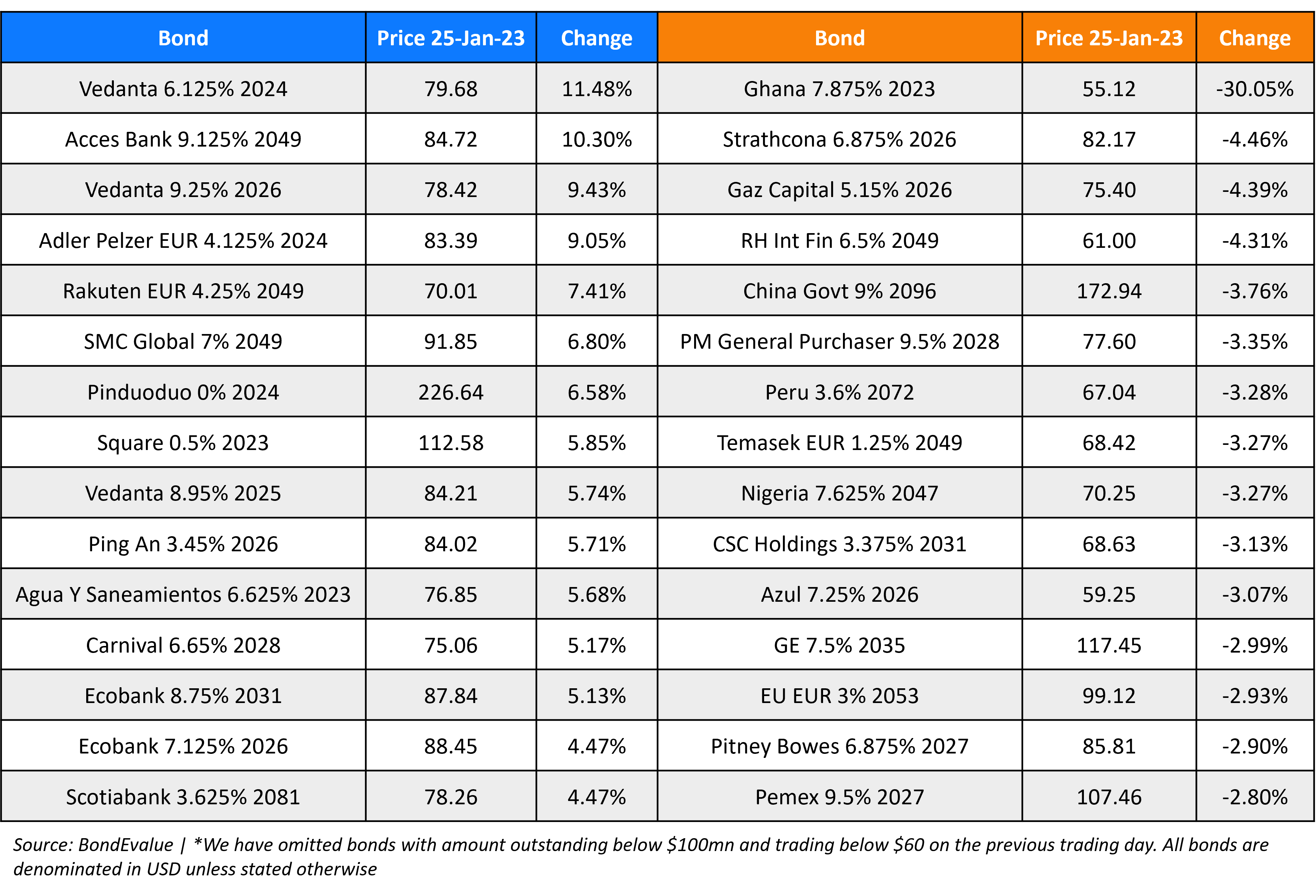

Top Gainers & Losers – 25-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.