This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

March 29, 2023

US Treasury yields moved higher yesterday with the 2Y yield jumping up by 14bp. The peak fed funds rate was only 1bp lower to 4.93% for the May meeting. Markets are trying to reassess when the Fed’s first rate cut would be this year. While CME maximum probabilities continue to show no further rate hikes this year, it was initially showing a 48% chance of a 25bp rate cut in July. However, markets are now looking at pushing that rate cut into the Fed’s meeting in September and status quo July. US consumer confidence for March came in at 104.2, higher than expectations of a 101 print. The reading was also higher than last month’s 103.4 print. The better-than-expected sentiment suggests household spending could remain resilient alongside a solid labor market, thereby helping growth. US IG and HY CDS spreads widened 0.7bp and 6bp respectively. The S&P and Nasdaq ended lower on Tuesday, down by 0.2% and 0.5% respectively.

European equity markets ended slightly higher. European main CDS spreads tightened by 0.5bp and Crossover spreads were 3bp tighter. Asia ex-Japan CDS spreads tightened by 1.2bp and Asian equity markets have opened with a slight positive bias this morning.

Last Call: Deep Dive on Bonds Course for Investors | 30 March in Singapore

-1.png)

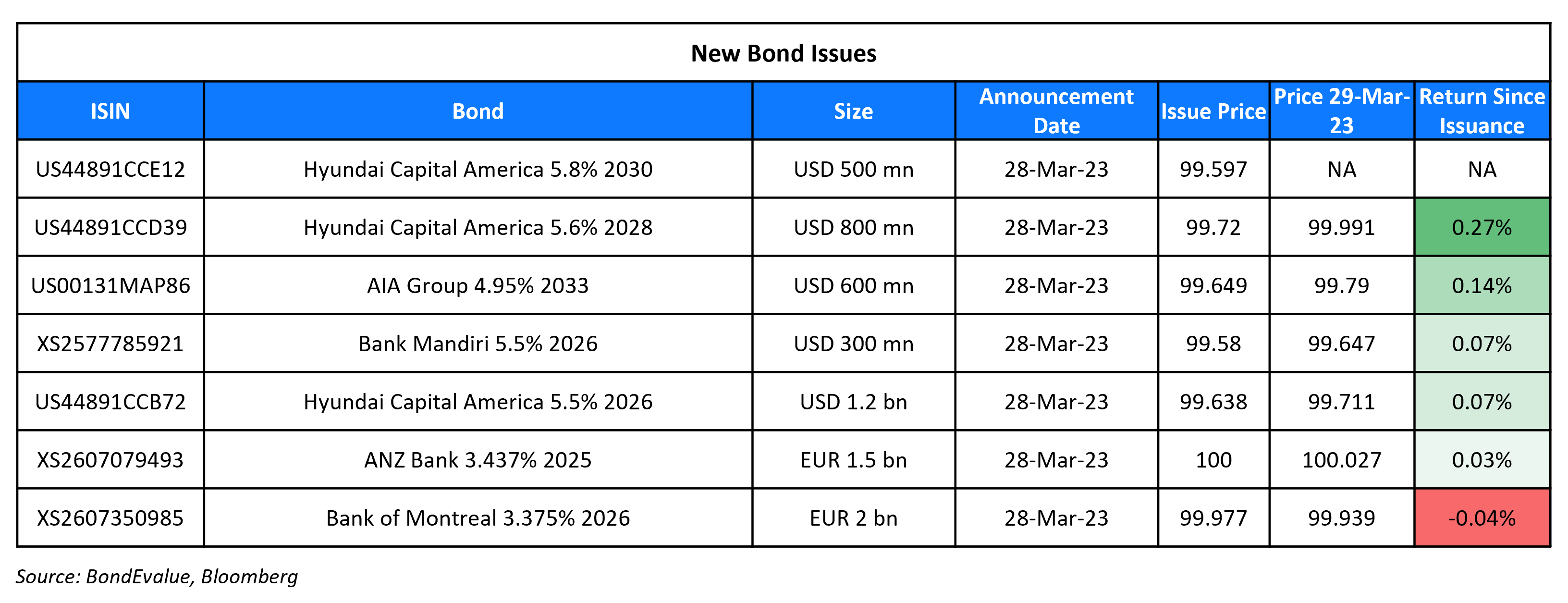

New Bond Issues

- Komir $ Long 5Y at T+210bp area

Bank Mandiri raised $300mn via a 3Y bond at a yield of 5.654%, 42bp inside initial guidance of T+225bp area. The senior unsecured bonds are rated Baa2/BBB- and received orders over $3.1bn. Asia took 78% and EMEA 22%. Fund managers took 76%, public sector/insurers/ pension funds took 11%, banks 10% and private banks 3%. The bonds have a change of control trigger if the Government of Indonesia ceases to directly or indirectly own 51% of Bank Mandiri and if the issuer witnesses a rating decline. The government currently holds 60% of the bank. Proceeds will be used for general corporate purposes. Bank Mandiri last issued dollar bonds in April 2021 with a $300m 2% sustainability bond due 2026. The new bonds are priced at a new issued premium of 11.4bp over its 2% sustainability bonds due 2026 that yield 5.54%.

Hyundai Capital raised $2.5bn via a three-tranche deal. It raised

- $1.2bn via a 3Y bond at a yield of 5.633%, 35bp inside initial guidance of T+210bp area. The new bonds are priced at an attractive new issue premium of 25.3bp to its existing 1.3% 2026s that yield 5.38%.

- $800mn via a 5Y bond at a yield of 5.665%, 30bp inside initial guidance of T+230bp area. The new bonds are priced at a new issue premium of 11.5bp to its existing 2% 2028s that yield 5.55%.

- $500mn via a 7Y bond at a yield of 5.871%, 30bp inside the initial guidance of T+255bp area. The new bonds are priced at a new issue premium of 9.1bp to its existing 6.375% 2030s that yield 5.78%.

The senior unsecured bonds have expected ratings of Baa1/BBB+. Proceeds will be used for general corporate purposes. The new notes are backed by a support agreement from the issuer’s South Korean parent, Hyundai Motor Co.

AIA Group raised $600mn via a 10Y bond at a yield of 4.995%, 35bp inside initial guidance of T+180bp area. The senior unsecured bonds have expected ratings of A1/A+/A+. Proceeds will be used for general corporate purposes. The issuer last launched a deal less than half a year ago with its 5.625% 2027s that were priced at a spread of T+150bp on 18 October 2022.

New Bonds Pipeline

- Cyprus hires for first ever sustainable bond

- REC hires for $ Long 5Y Green bond

- Shinhan Bank hires for $ senior bond

Rating Changes

- United Airlines Holdings Inc. Upgraded To ‘BB-‘ From ‘B+’ On Strong Credit Measures; Outlook Stable

- Moody’s downgrades Carvana’s CFR to Ca; deems proposed debt exchange a distressed exchange

- Fitch Downgrades Japfa to ‘B+’/’A(idn)’; Outlook Stable

- Moody’s changes outlook to positive for Rio Tinto; affirms ratings

- Fitch Revises Qatar’s Outlook to Positive; Affirms at ‘AA-‘

Term of the Day

Scheme of Arrangement (SoA)

Scheme of Arrangement (SoA) is a legal mechanism used by a company in financial difficulty to reach a binding agreement with its creditors to pay back all, or part, of its debts over an agreed timeline. Typically, the company draws up scheme proposals for its creditors and sends it to them with notice of a creditors meeting. During the meeting, the company explains the proposals and creditors decide to vote in (or against) favor of the scheme. The scheme is then approved by a High Court, after which debts are written down as per the SoA. SoAs go through a court approval, making it different from consent solicitations.

Talking Heads

On A Single Bet on Deutsche Bank’s CDS Seen Behind Friday’s Rout

Andrea Enria, the ECB’s top oversight official

“There are markets like the single name CDS market which are very opaque, very shallow, very illiquid… With a few millions, you can move the CDS spreads and contaminate also stock prices and possibly also deposit outflows”

Suvi Platerink Kosonen, a banking credit analyst at ING Groep NV

“Investors see Deutsche Bank as one of the higher beta names; so in case you want to bet generally against weak sentiment, then these kind of names may be interesting”

On ECB Saying Regulators Should Review CDS Market After Bank Turmoil

Andrea Enria, ECB’s Supervisory Board Lead

FSB could review “how these markets really work… It’s always the last resort for a supervisor to intervene. If you had good transparency, for example having these markets all centrally cleared rather than have OTC opaque transactions where you don’t know who is trading, I think that would be already great progress.”

On Traders Go Long Treasuries After Hedge Funds Unwind Short Bets

Citigroup strategists Ed Acton and Bill O’Donnell

“Fast- and medium-term positioning has flipped long as yields squeeze lower driven by short covering (capitulation)”

On Global Creditors Facing Long Fight With China Developers for Money

Charles Chang, Greater China country lead at S&P Global HK

“We haven’t seen a cluster of this many defaulted cases in China in many years. It’s difficult to use past benchmarks. It’s a precedent-setting moment”

Jenny Zeng, CIO for Asia fixed income at Allianz Global Investors

“There remain obstacles in execution due to the size and complexity of the capital structures of most of defaulted developers… The cross-border feature also adds another layer of execution challenges… The first-ever real credit default cycle China is now experiencing should also provide better visibility on restructuring processes and recovery value”

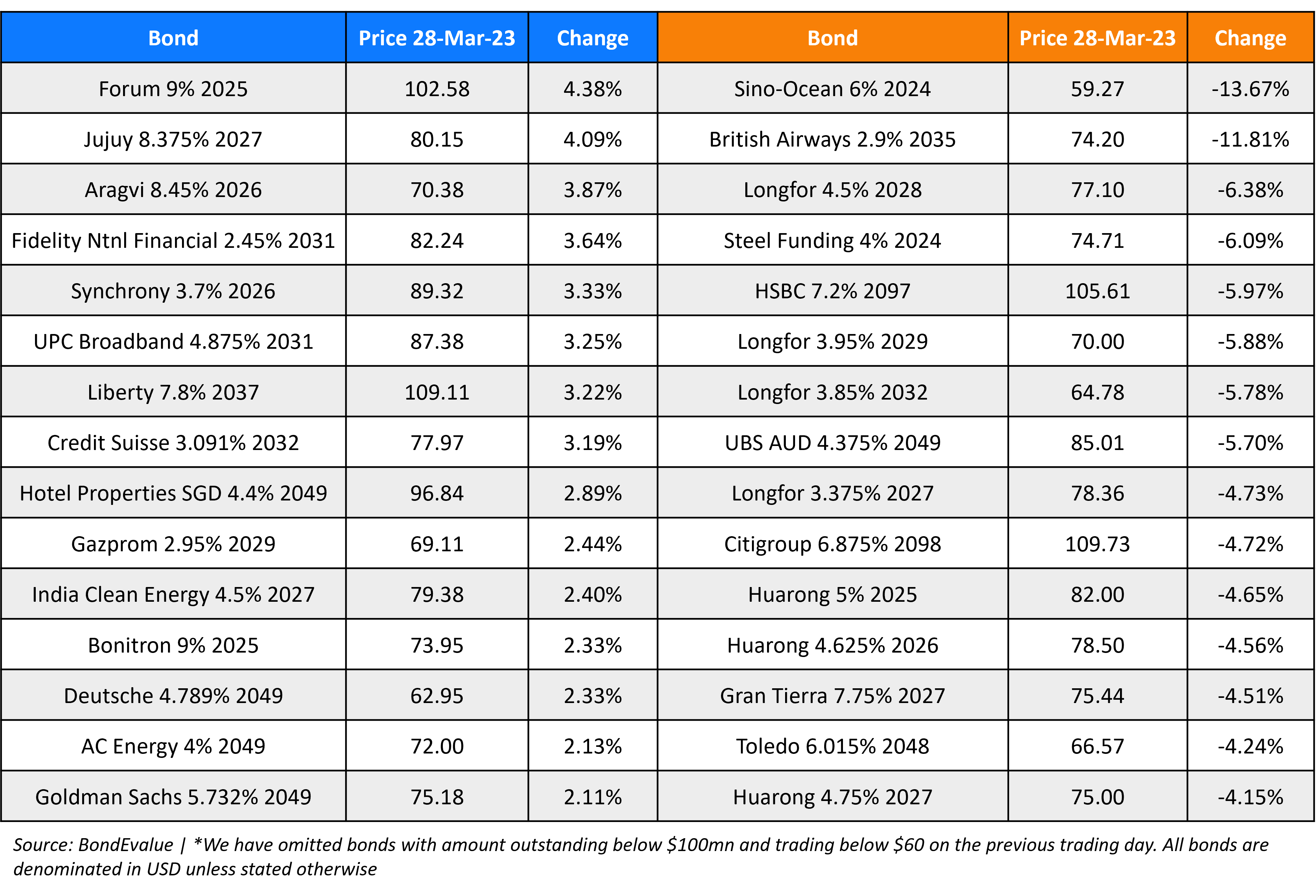

Top Gainers & Losers – 28-March-23*

Other News:

Alibaba to overhaul business into six independently run entities

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.