This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; Talking Heads; Top Gainers and Losers

August 4, 2023

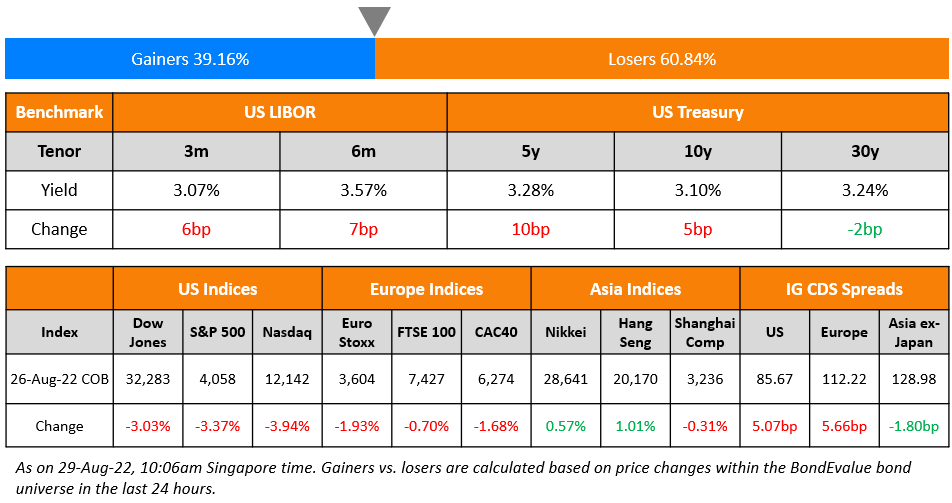

US 10Y and 30Y Treasury yields continued to jump higher by 7-8bp as the curve continued to bear steepen with the 2s10s now at -72bp. US initial jobless claims rose 6k to 227k, in-line with expectations but still hovering over the lowest levels this year, supporting claims of a resilient labor market. ISM Services PMI for July fell to 52.7 from 53.9 the month prior, missing expectations of 53.0. On the positive side, the print still remains above the 50-mark which indicates expansion in the services sector. The peak Fed Funds rate was up 1bp to 5.42%. US IG credit spreads widening 0.7bp and HY CDS spreads widening by 1.8bp. The S&P and Nasdaq were lower by 0.3% and 0.1% respectively

European equity markets were lower too. The Bank of England (BoE) raised its policy rates by 25bp to 5.25% as expected to tackle inflation that is at 7.3%. However, unlike the US Fed and ECB, they maintained a hawkish stance saying that they will ensure that the Bank Rate is “restrictive for sufficiently long to return inflation to the 2% target”. In credit markets, European main CDS spreads were 0.3bp wider and Crossover CDS widened 4.1bp. Asia ex-Japan CDS spreads widened by 0.8bp. Asian equity markets have opened higher this morning, following global bourses.

New Bond Issues

.png)

Rating Actions

- Fitch Upgrades Cenovus to ‘BBB’; Outlook Stable

- Moody’s downgrades Country Garden to B1; outlook negative

- Fitch Upgrades Wanda Commercial, Wanda HK to ‘CC’ After Coupon Paid Within Grace Period

- Fitch Downgrades China Great Wall AMC (International) to ‘A-‘; Maintains RWN

- Casino Guichard – Perrachon Downgraded To ‘CC’ From ‘CCC-‘ On Virtual Certainty Of Default; Outlook Negative

- Vedanta Resources Ltd. Outlook Revised To Negative On Increased Funding Risks; ‘B-‘ Ratings Affirmed

Term of the Day

Floater/FRN

Floating Rate Bonds are also known as floaters or FRNs (floating rate notes). These are bonds with a variable interest rate unlike fixed rate bonds. Floaters are considered attractive for investors in a rising interest rate environment since the interest rate/coupon gets re-adjusted periodically (semi-annually/quarterly etc.), linked to benchmark rates such as SOFR.

Wells Fargo raised $5bn via a four-part deal of which it raised $400mn each via a 2Y and 3Y FRN.

Talking Heads

“We are short in size the 30-year T…(if long-term inflation is 3% not 2%, the 30-year Treasury yield could rise to 5.5%) and it can happen soon…There are few macro investments that still offer reasonably probable asymmetric payoffs and this is one of them.”

On BoJ’s Second Intervention in the JGB Market

David Forrester, strategist at Credit Agricole

“Two observations do not make a pattern, but for now five basis points increments could be the BOJ’s tolerance for movements higher in the 10-year Japan government bond yield…Such a slow grind higher would help limit yen downside against the dollar in an environment of rising US Treasury yields”

Shoki Omori, chief desk strategist at Mizuho Securities

“It’s too early to tell whether they are focusing on the level or speed at which yields rise…The 10-year yield can go to 0.7% in a week if the BOJ’s message remains unclear.”

Moh Siong Sim, FX strategist at Bank of Singapore

“This is likely to cap prospects for lower USD/JPY in the near term amid a backdrop of rising US yields.”

On Companies Shifting Away from Leveraged Loans to HY Bonds

John Cokinos, global head of leveraged finance at RBC Capital Markets

“It’s a good way to balance each of these markets off each other, and honestly, a better cost of capital…You can hedge naturally by just having fixed-rate debt.”

Lauren Basmadjian, co-head of liquid credit and head of US loans and structured credit at Carlyle Group

“As buying capacity shrinks, that’s making the high-yield market an attractive place to issue.”

Valerie Kritsberg, head of capital markets and trading at Blackstone Credit

“Historically, to the extent that the loan market was open, it was preferable for sponsors to finance their (leverages buyouts) with loan-heavier structures…Almost everything right now is being underwritten with loan and bond flex to give the banks and the sponsors maximum flexibility between the two markets, given the uncertainty on execution created by market volatility.”

On England’s Interest Rates Outlook After Rate Hike

Statement from the Bank of England

“…if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required…The MPC would ensure that Bank Rate was sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit…. (Key indicators especially wage growth) suggest that some of the risks from more persistent inflationary pressures may have begun to crystallize.”

Andrew Bailey, BoE Governor

“We have to balance the risks here, and we’ve got risks both ways…There is no presumed path of interest rates…(it is) far too soon to speculate on when we might see a cut.”

Luke Hickmore, investment director at abrdn

“The vote split (on interest rates among MPC members) indicated we are nearing the peak now…Some of the language used today also suggests they are getting nervous about the economy’s reaction to the hikes in place so far.”

Dan Hanson, senior economist at Bloomberg

“The Bank of England’s decision to step down the pace of tightening in August suggests it is a little less troubled by the inflation outlook than it was in June. That said, the messaging around the decision suggests there is a little further to go in the tightening cycle before the central bank will feel comfortable pausing.”

Martin Weale, former member of the BoE’s MPC

“There is a risk of overtightening…But hindsight’s a wonderful thing and, if there is a recession and inflation does come down quickly, then people will say the bank overtightened.”

On Recovery Rates for HY Bonds and Leveraged Loans – JPMorgan

JPMorgan has published a credit research report that says recoveries for high-yield bonds and leveraged loans over the last 12 months are 19.6% and 39.7%, well below its 25-year and 24-year annual averages of 40.2% and 64.3%. Therefore, debtholders of defaulted or bankrupt issuers are getting back less money compared to historical averages. While loan recoveries tend to be higher than HY bonds due to their higher seniority, many companies sold only loans to investors over the last decade due to lower rates, creating a potential pileup of claimants should the company falter.

Top Gainers & Losers –04-August-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.