This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

CapitaLand Launches S$ Bond; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

April 5, 2022

US equity markets moved higher to start the week with the S&P and Nasdaq up 0.8% and 1.9% each. Sectoral gains were led by Consumer Discretionary and Communication Services up over 2%. US 10Y Treasury yields moved 2bp higher to 2.40%. European markets were higher – the DAX, CAC and FTSE were up 0.5%, 0.7% and 0.3%. Brazil’s Bovespa ended 0.2% lower. In the Middle East, UAE’s ADX was up 1.3% and Saudi TASI was up 0.6%. Asian markets have opened with a positive bias – Shanghai, HSI and STI were up 0.9%, 2.1% and 0.4% while Nikkei was down 0.1%. US IG CDS spreads tightened 3.2bp and HY spreads were 11.8bp tighter. EU Main CDS spreads were 2.5bp tighter and Crossover CDS spreads were 6.3bp tighter. Asia ex-Japan CDS spreads tightened 2.4bp.

Turkey’s inflation for March came at 5.46% MoM, lower than forecasts of 5.77%.

Happening Today | Masterclass on How to Analyze CoCo/AT1 Perpetual Bonds

Sign up for today’s masterclass on ESG/Sustainable bonds that will cover Key Definitions, Growth of the ESG Bond Market, Types of ESG Bonds, ESG Bond Standards, External Reviews, Deep dive on ESG Bond Examples, Greenium and Greenwashing. The session will begin 5pm Singapore / 1pm Dubai / 9am London. Click on the banner below to register.

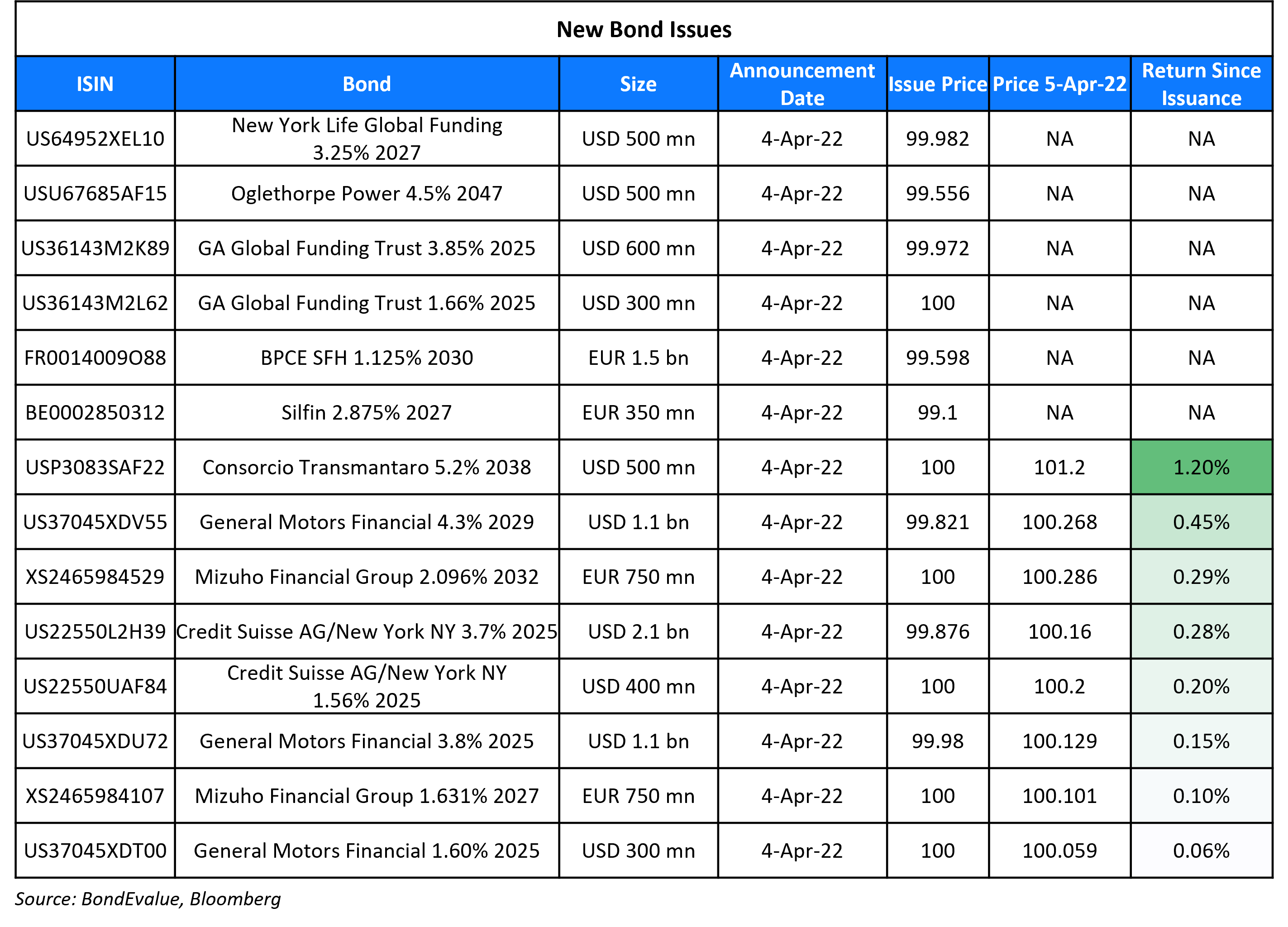

New Bond Issue

- CapitaLand Investment S$ 5Y at 3.6% area

- $2.1bn via a 3Y bond at a yield of 3.747%, 20bp inside initial guidance of T+135bp area

- $400mn via a 3Y bond FRN at SOFR+126bp vs. initial guidance of SOFR equivalent area

The bonds are rated A1/A+. The issuer is Credit Suisse AG/New York NY. Proceeds will be used for general corporate purposes. The new 3Y fixed bond was priced ~17bp tighter to Credit Suisse’s existing 3.75% bonds due March 2025 that yield 3.92%.

GM Financial raised $2.5bn via a three-tranche deal. It raised:

- $1.1bn via a 3Y bond at a yield of 3.807%, 25bp inside initial guidance of T+145bp. The new bonds are priced at a new issue premium of 22.7bp over its existing 4% 2025s that yield 3.58%.

- $300mn via a 3Y FRN bond at a yield of 1.6% vs. initial guidance of SOFR equivalent.

- $1.1bn via a 7Y bond at a yield of 4.33%, 25bp inside initial guidance of T+205bp.

The bonds have expected ratings of Baa3/BBB. Proceeds will be used for general corporate purposes. The bonds are issued by General Motors Financial Co Inc (GM).

Lendlease Global Commercial REIT raised S$200mn via a PerpNC3 bond at a yield of 5.25%, 25bp inside initial guidance of 5.5% area. The bonds are unrated and received orders over S$775mn, 3.9x issue size. Private banks, which will receive a 25-cent concession, were allotted 70% of the deal with insurance companies, fund managers and banks taking 30%. Singapore accounted for 98% while others took 2%. RBC Investor Services Trust Singapore is the issuer. The coupon will reset at the end of year three to the prevailing SORA-OIS plus the initial credit spread of 304.3bp, if not called. Proceeds will be used for debt refinancing and potential acquisitions, including the purchase of the remaining stake in the Jem shopping mall, as well as for general working capital needs.

New Bonds Pipeline

- Sael Limited hires for $ 7Y Green bond

- JR East hires for € 11Y bond

- Kalyan Jewellers India hires for $ bond

- South32 hires for $ bond

- Korea Mine Rehabilitation and Mineral Resources hires for $ 5Y bond

- Shinhan Bank hires for $ Green bond

- Aluminium Corporation of China hires for $ bond

- Petron hires for $ 7NC4 bond

- Electricity Generating (EGCO) hires for $ 7Y or 10Y bond

Term of the Day

Acceleration Notice

An acceleration notice is a bond clause which allows lenders to demand a borrower to immediately repay a bond if specific requirements are not met. Thus the borrower must immediately pay unpaid principal and accumulated interest prior to the invocation of the notice. These notices are generally given when a borrower materially breaches the loan/debt agreement.

Explore BondbloX Kristals – a basket of single bonds listed on the BondbloX Exchange following themes such as SGD REIT Perps, USD Bank Perps, and SGD Bank Perps. Avail an introductory discount of $1,000 for every purchase of $100,000 worth of BondbloX Kristals*. Click on the banner above to know more.

Talking Heads

On Sri Lanka Default Seen ‘Inevitable’ as Bond Losses Deepen

Carlos de Sousa, an investor at Vontobel Asset Management

“The reckoning time has come. The government and the central bank have ignored it. What’s not clear is whether the current president will survive this episode of protests.”

International Monetary Fund

“Rollover risk is very high. [The country’s debt service needs each year] “will require access to very large amounts of external financing at concessional rates and long maturities, sustained over many years.”

Johanna Chua, chief economist for Asia Pacific at Citigroup

“The government will likely need to secure private creditor participation in debt reduction”

Charles Robertson, global chief economist at Renaissance Capital

“Sabry defended the president against corruption charges in the past… appointment doesn’t appear to be based on his technical expertise… unfortunate as the previous finance minister was supposed to be seeing the IMF for talks in Washington next week — all very messy.”

On ECB’s Vasle Says Negative Rates May End by Turn of the Year

“The most important thing for me is that we will start this process not very late in the year and have the opportunity to be out of negative territory by the turn of the year… We’re still expecting quite strong positive growth rates, and if that scenario materializes I don’t see any reasons why we wouldn’t continue with policy normalization after the turn of the year and go above zero with interest rates”

On Morgan Stanley Says ‘Bear Market Rally’ Is Now Over

Morgan Stanley Chief U.S. Equity Strategist Michael Wilson

“The bear market rally is over. That leaves us more constructive on bonds than stocks over the near term as growth concerns take center stage – hence our doubling down on a defensive bias.”

JPMorgan strategists led by Mislav Matejka

“Geopolitics remains a wild card, but we do not see equities fundamental risk-reward to be as bearish as it is currently fashionable to portray”

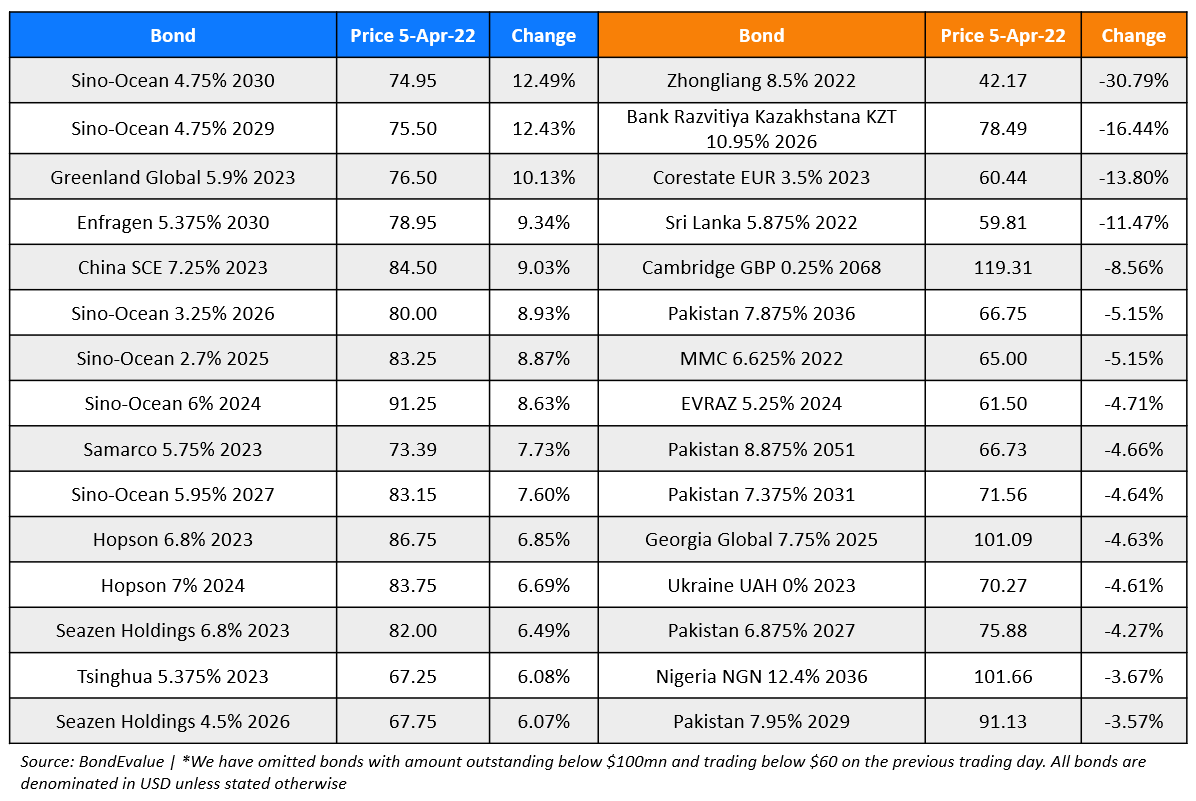

Top Gainers & Losers – 05-Apr-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.