This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

September 13, 2022

US 10Y Treasury yields were flat at 3.34%, with US IG CDS spreads tightening 3.1bp and US HY spreads tightening 17.7bp. The broad risk-on tone continued as US equity markets continued its upward move on Monday – the S&P and Nasdaq were higher by 1% and 1.3% respectively. US CPI is forecasted at 8.1% and Core CPI at 6.1% for August, with the data release due later today. As per economists, headline inflation is expected to soften from its 8.5% print in July while core inflation is set to rebound from 5.9% in July. The New York Fed’s consumer expectations survey noted that the 3Y inflation outlook in the US fell to 2.8% in August from 3.2% and 3.6% in July and June respectively. The 1Y inflation outlook fell to 5.7% from 6.2% in July.

European markets posted solid gains with the DAX, CAC and FTSE up by 2.4%, 2% and 1.7% respectively. EU Main CDS spreads tightened by 3.6bp and Crossover spreads were 15.8bp tighter. Brazil’s Bovespa was up 1%. In the Middle East, UAE’s ADX and Saudi TASI ended up 1.4% and 0.7% respectively. Asian equity markets have opened broadly positive, up ~0.5% today. Asia ex-Japan CDS spreads were flat.

IBF-STS Course on Digital Assets | 29 Sep 2022 (In-person in Singapore)| 70/90% Funding

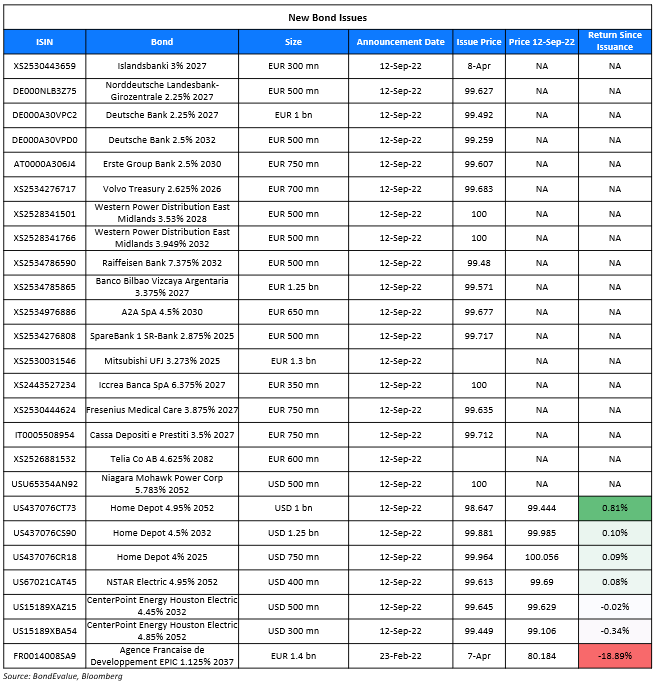

New Bond Issues

Deutsche Bank raised €1.5bn via a two-tranche covered bond deal. It raised:

- €1bn via a 5Y bond at a yield of 2.359%, 4bp inside the initial guidance of MS+8bp area. The bonds received orders over €1.9bn, 1.9x issue size.

- €500mn via a 10Y bond at a yield of 2.585%, 2bp inside the initial guidance of MS+14bp area. The bonds received orders over €1.5bn, 3x issue size.

The bonds had expected ratings of Aaa (Moody’s). The bonds are issued under the Mortgage Pfandbrief (Hypothekenpfandbrief) format as per Bloomberg.

Erste Bank raised €750mn via a 8Y covered bond at a yield of 2.555%, 3bp inside the initial guidance of MS+19bp area. The bonds have expected ratings of Aaa (Moody’s), and received orders over €1.4bn, 1.9x issue size.

New Bonds Pipeline

- Ganzhou Urban Investment Holding Group hires for $ bond

- Aozora Bank hires for $ 3Y Green bond

- NH Investment hires for $ 3Y and/or 5Y Green bond

Rating Changes

Term of the Day

Sustainability-Linked Bonds (SLBs)

Sustainability-linked bonds (SLBs) are bonds wherein the issuer commits to sustainability outcomes within a timeline set in the bond document based on five elements:

- Selection of Key Performance Indicators (KPIs)

- Calibration of Sustainability Performance Targets (SPTs)

- Bond Characteristics

- Reporting

- Verification

Here however, the proceeds can be used for general purposes but the characteristics of the bond can change depending on the issuer meeting their KPIs set in the document. SLBs come with a coupon ste-up if the issuer fails to meet its goal(s) within the specified time period in its framework.

Talking Heads

On Jumbo ECB Hike Aimed at Inflation Expectations – ECB’s Guindos

For a central bank its credibility is fundamental… We decided to raise rates by 75 basis points and have announced that we’ll continue to raise… How many times we do so and by how much will depend fundamentally on data

On US Inflation Expectations Dropping in August – New York Fed

Expectations for US inflation three years ahead fell to 2.8% in August, from 3.2% the previous month and 3.6% in June… Median home-price expectations declined sharply by 1.4 percentage points to 2.1%, its lowest reading since July 2020. The decline was broad based across demographic groups and geographic regions.”

On Credit Calculus Turning Against Stocks With Yield Edge Over Bonds Vanishing

Lisa Shalett, CIO of Morgan Stanley Wealth Management

“Because the spreads on investment grade corporate bonds have recently widened, stocks no longer look attractively priced versus comparable corporate debt”

Mike Wilson, Morgan Stanley’s chief US equity strategist

“The argument is that stocks are a better asset to own than bonds in such a regime and therefore deserve a lower risk premium… While we agree with the premise of that argument and, in fact, used that exact statement to go all in on stocks in late March 2020, we don’t think it’s an appropriate rationale today if one believes we are entering a significant cyclical downturn for earnings forecasts”

On JPMorgan slashing EM corporate debt issuance forecast by a third

“The primary market remains subdued with little signs of pick-up, compelling us to revise down our 2022 (EM corporate) issuance forecast once more to $260 billion from $400 billion… We do not anticipate a strong rebound in issuance in the foreseeable future”

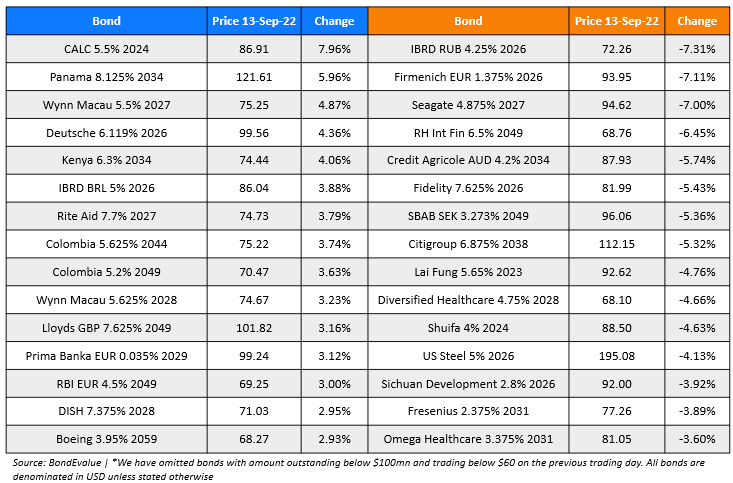

Top Gainers & Losers – 13-September-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.