This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

September 2, 2022

US equity markets ended mixed on Thursday with the S&P up 0.3% while Nasdaq was down 0.3%. Sectoral losses were led by Energy, down 2.3% and Materials falling 1.4% while Healthcare was up 1.7%. US 10Y Treasury yields were 6bp higher at 3.26%. European markets ended lower– DAX, CAC and FTSE declined 1.6%,1.5% and 1.9% respectively. Brazil’s Bovespa gained 0.8%. In the Middle East, UAE’s ADX and Saudi TASI were down 1.6% and 1.2% respectively. Asian markets have opened broadly lower today – HSI, STI and Nikkei were down 0.6%, 0.2% and 0.4% respectively while Shanghai was up 0.3%. US IG CDS spreads tightened 1.9bp and US HY spreads were narrower by 10.9bp. EU Main CDS spreads were 0.1bp wider and Crossover spreads tightened by 2.2bp. Asia ex-Japan IG CDS spreads widened 5.4bp.

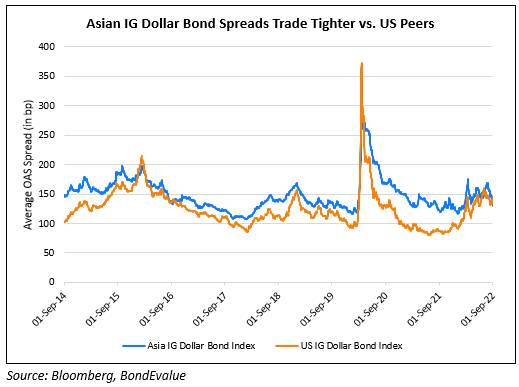

Average dollar bond spreads of Asian IG corporates are now tighter than that of its US IG peers as measured by Option-Adjusted Spreads (OAS) (Term of the Day, explained below). This would imply that Asian IG corporates currently have a lower credit, liquidity and optionality risk than US IG counterparts. Overall, this is an infrequent occurrence in financial markets although it is the second time that Asian IG spreads have gone below US IG spreads this year, after a similar move occurred in June. Prior to June, this spread tightening was observed at the peak of the pandemic in 2020, and before that, one has to look back at late-2016 when such a move happened (as seen in the chart below). Analysts note that this move has been fueled in-part by divergent monetary policies from the regions – the Fed has been hiking rates with a hawkish stance while Asian spreads that are primarily dominated by China have seen the nation cut its policy rates and ease monetary policy.

Unemployment rate in the Eurozone for July fell to an all-time low of 6.6% vs. 6.7% in June and down from 7.7% a year ago. ECB will hold a policy meeting next week amid record high inflation and low unemployment rate with 75bp rate hike expectations. In the US, initial jobless claims fell by 5k to 232k for August 27, lower than estimates of 248k indicating a healthy demand for labor in moderate economic growth. In Pakistan, inflation rose to 47-year high of 27.26% for August, higher than estimates of 26.6% and July’s 24.93% print, led by transport and food prices shooting higher by 63% and 29.5% respectively.

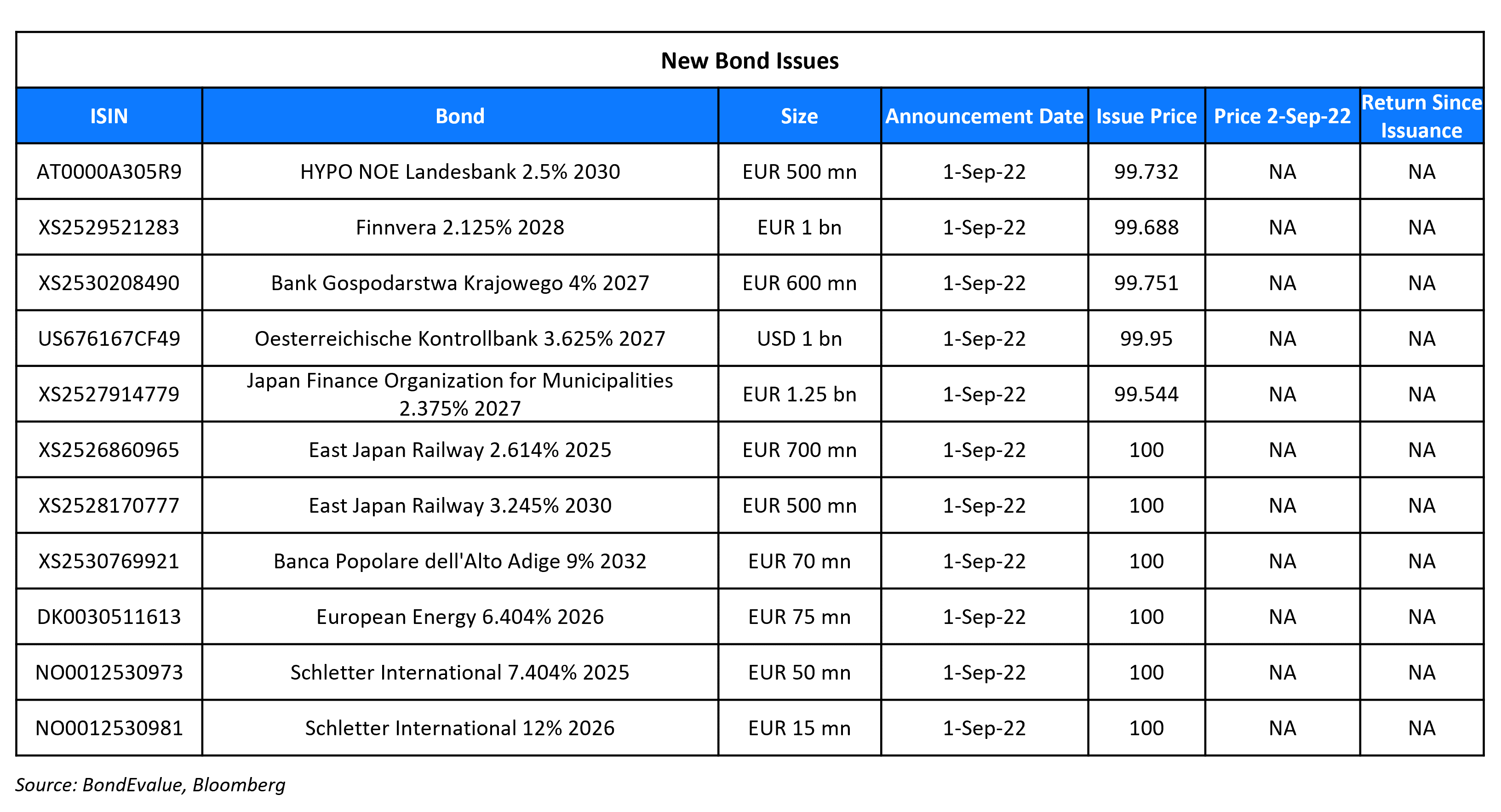

New Bond Issues

- Zhenjiang Transportation Industry Group $ 3Y at 5.2% area

East Japan Railway Company raised €1.2bn via a two-tranche deal. It raised

- €700mn via a 3Y bond at a yield of 2.614%, 18bp inside initial guidance of MS+60bp area. The bonds received orders over €1.3bn, 1.9x issue size.

- €500mn via a 8Y bond at a yield of 3.245%, 5bp inside initial guidance of MS+90bp area. The bonds received orders over €575mn, 1.2x issue size.

The senior unsecured bonds have expected ratings of A1/A+. Proceeds will be used for general corporate purposes.

New Bonds Pipeline

- Macquarie Bank hires for € 5Y bond

- Aozora Bank hires for $ 3Y Green bond

- Tianjin Binhai New Area Construction & Investment hires for $ bond

- NH Investment hires for $ 3Y and/or 5Y Green bond

Rating Changes

- Fitch Downgrades Credito Real to ‘D’ on Initiated Liquidation Process; Withdraws Ratings

- Bed Bath & Beyond Inc. Senior Unsecured Debt Rating Lowered To ‘CCC-‘ On New FILO Facility And Upsized ABL

- Singtel, Optus Outlook Revised To Stable From Negative On Leverage Management; ‘A/A-1’, ‘A-/A-2’ Ratings Affirmed

- Apache Corp. Outlook Revised To Positive On Improving Metrics, Ratings Affirmed

Term of the Day

Option Adjusted Spread (OAS)

Option Adjusted Spread (OAS) refers to a measure of the credit spread of a bond with embedded options relative to a benchmark, similar to the Z-Spread. The key difference between OAS and Z-Spread lay in the optionality. When comparing two bonds – one with an embedded option and one without – OAS is a better measure compared to Z-Spread as the former adjusts for/removes the impact of optionality for a like-to-like comparison. Put simply, OAS ≈ Z-Spread + Option cost.

On a technical note, the above formula is not an exact equation as the Z-Spread is calculated from the spot curve while the OAS is calculated from the forward curve. The OAS is less than the Z-Spread for callable bonds and greater than Z-Spread for puttable bonds

Talking Heads

On Goldman Cutting India Growth Outlook as Deutsche Flags Slower Hikes

Goldman Sachs economist Santanu Sengupta

“Despite the main drivers of domestic demand coming in line with our expectations, a large drawdown in inventories and statistical discrepancies came as a surprise”

Deutsche Bank economist Kaushik Das

“We will not be surprised, if RBI decides to slow down its pace of rate hikes to 25 basis points clips from September onwards”

Citi economists Samiran Chakraborty and Baqar M Zaidi

“Emergence of downside risk to growth and upside risk to inflation would further complicate RBI’s aim of calibrated monetary policy actions”

On ECB Seen Playing Catch-Up as Rate-Hike Path Steepens

Nerijus Maciulis, an economist at Swedbank

“The ECB will continue hiking rates at an accelerated pace and will send a hawkish message. It needs to repair its reputation and be able to claim victory once inflation starts retreating.”

Claus Vistesen, an economist at Pantheon Macroeconomics

“The ECB will continue to drive a hard line against inflation, despite evidence that growth is slowing. We even expect the ECB to outright recognize that the economy is now entering a recession, but that it will continue to hike regardless”

Carsten Brzeski, an economist at ING

“The unanswered question is still how the ECB’s reaction function will look in what increasingly looks like a severe winter recession”

On Man Group Warning of Contagion to European Firms From EM Defaults

We may be on the cusp of a distressed debt supercycle. But unlike in 2008, the crisis is likely to originate from EM, not DM

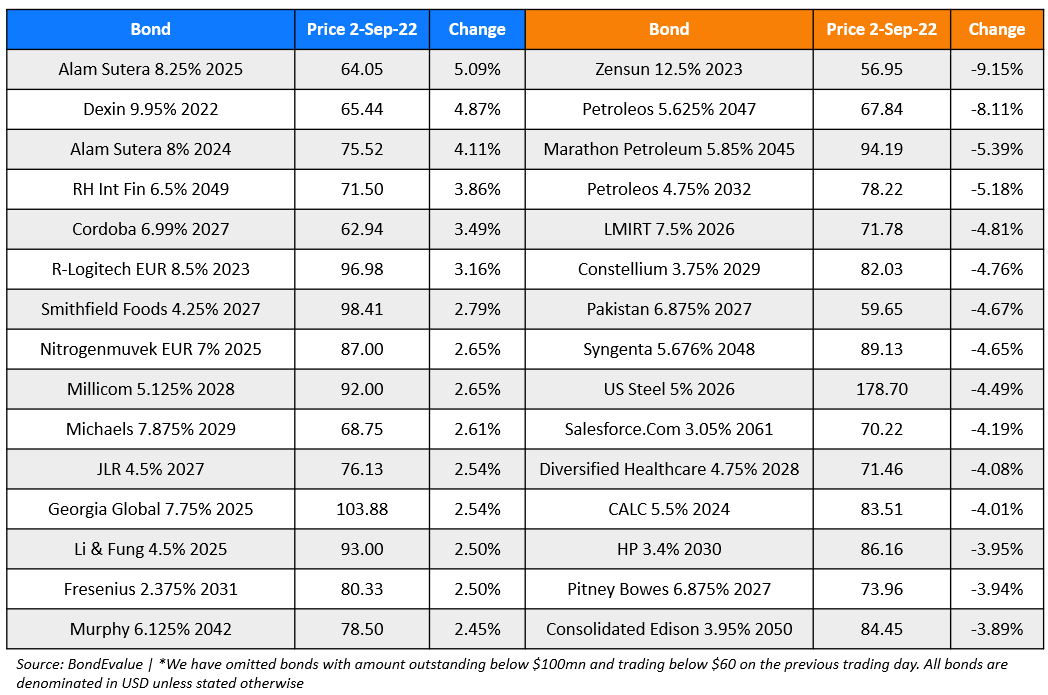

Top Gainers & Losers – 02-September-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.