This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

UOB, First REIT Launch Bonds; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

March 31, 2022

US equity markets trudged lower with the S&P and Nasdaq down 0.6% and 1.3%. Sectoral losses were led by Consumer Discretionary and IT, down over 1% each. US 10Y Treasury yields eased 1bp to 2.33%. European markets were mixed – the DAX and CAC were down 1.5% and 0.7% while FTSE was up 0.6%. Brazil’s Bovespa ended 0.2% higher. In the Middle East, UAE’s ADX was down 0.6% and Saudi TASI was down 0.5%. Asian markets have opened with a negative bias – Shanghai, HSI, STI and Nikkei were down 0.1%, 0.8%, 0.2% and 0.5%. US IG CDS spreads widened 0.4bp and HY spreads were 4.3bp wider. EU Main CDS spreads were 0.5bp wider and Crossover CDS spreads were 5.5bp wider. Asia ex-Japan CDS spreads tightened 1.6bp.

The People’s Bank of China said that it will step up the magnitude of monetary policy and make it more forward-looking, targeted and autonomous. Thus it indicated its intention to boost confidence and support the economy.

Happening Today | Masterclass on New Bond Issues & Credit Ratings

Today’s session will be a deep dive on new bond issues – terminologies, process, timeline, pricing and analysis. The session will also cover credit ratings – how to find and interpret them. The session is at 5pm Singapore / 1pm Dubai / 9am London. Sign up by clicking on the banner below:

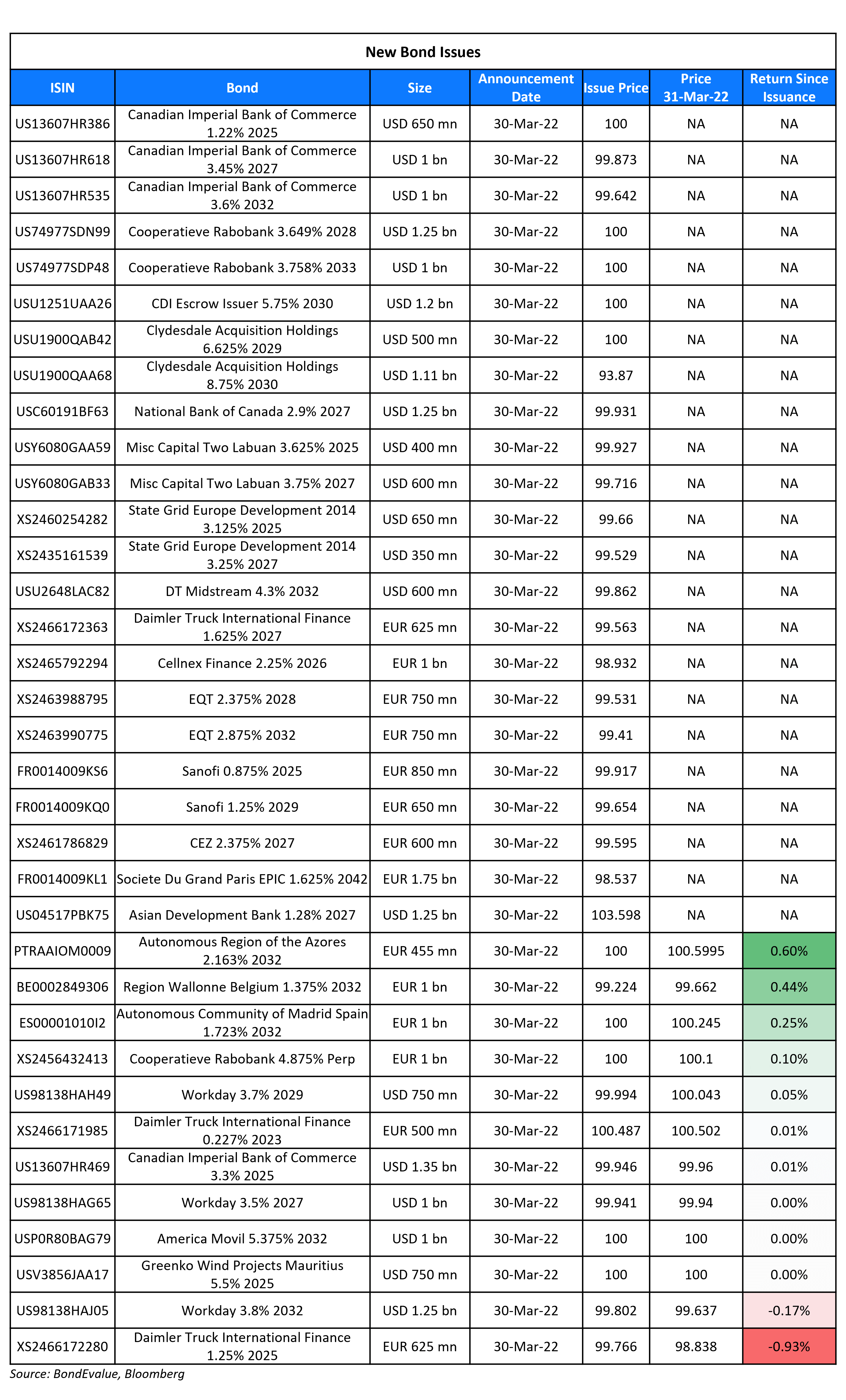

New Bond Issues

- First REIT Management S$ 5Y Social at 3.5% area

- UOB $ 3Y/3Y FRN/10.5NC5.5 T2 at T+90bp/SOFR equivalent/T+185bp area

Greenko Wind Projects (Mauritius) raised $750mn via a 3Y bond at a yield of 5.5%, 30bp inside the initial guidance of 5.8% area. The bonds are rated Ba1/BB (Moody’s/Fitch) and received orders over $2bn, 2.7x issue size. Asian investors were allocated 46% of the deal, the US 32% and EMEA 22%. Asset and fund managers took 90%, banks and private banks 5%, insurers and pension funds 4% and others 1%. Greenko Energy Holdings will provide a guarantee. The new bonds priced 39bp wider to related-entity Greenko Solar’s 5.55% bonds due January 2025 that are currently yielding 5.11%.

Singapore Post raised S$250mn via a PerpNC5.25 bond at a yield of 4.35%, 30bp inside initial guidance of 4.65% area. The bonds are rated BBB- and received orders over $850mn, 3.4x issue size. About 54% went to private banks, 42% to insurers and fund managers and 4% to banks and corporations. The distribution rate for the notes will be reset every five years after the initial 5.25Y call date. The notes have a 25bp step-up initially, and an additional 75bp step-up from year 25.5. The proceeds will be used for general corporate purposes, including refinancing.

Rabobank raised $2.25bn via a two-tranche deal. It raised $1.25bn via a 6NC5 bond at a yield of 3.649%, 23bp inside the initial guidance of T+145bp area. It also raised $1bn via a 11NC10 bond at a yield of 3.758%, 23bp inside the initial guidance of T+165bp area. The bonds have expected ratings of A3/A-.

Rabobank raised €1bn via a PerpNC7.25 AT1 bond at a yield of 4.876%, 49.9bp inside initial guidance of 5.375% area. The bonds are rated Baa3/BBB (Moody’s/Fitch) and received orders over €3bn, 3x issue size. The coupon is fixed at 4.875% until the first reset date of December 29, 2029). If not called, it refixes every five years at 5Y MS+371.7bp, from an annual to a semi-annual rate. The bonds are callable from and including June 29, 2029 to and including the first reset date and each interest payment date thereafter. A trigger event occurs if the CET1 ratio of Rabobank Group has fallen below 7%; and/or Rabobank’s CET1 ratio has fallen below 5.125%.

Chinese state-owned utility State Grid International raised $1bn via a two-tranche deal. It raised $650mn via a 3Y bond at a yield of 3.245%, 45bp inside the initial guidance of T+120bp. It also raised $350mn via a 5Y green bond at a yield of 3.353%, 45bp inside initial guidance of T+135bp area. Wholly owned subsidiary State Grid Europe Development (2014) Public Co is the issuer with a guarantee from the parent. The bonds have expected ratings of A1/A+/A+. Proceeds from the five-year tranche will be used to finance and/or refinance eligible assets under SGID’s green framework.

Malaysian state-owned shipping company MISC raised $1bn via a two-tranche deal. It raised $400mn via a 3Y bond at a yield of 3.651%, 45bp inside the initial guidance of T+160bp area. It also raised $600mn via a 5Y bond at a yield of 3813%, 45bp inside the initial guidance of T+180bp area. The bonds have expected ratings of Baa2/BBB (Moody’s/S&P). The bonds are issued by wholly owned subsidiary MISC Capital Two (Labuan), and guaranteed by the parent. The proceeds from the Singapore and Malaysia-listed trade will be used for general corporate purposes, including capex, working capital and refinancing.

Asian Development Bank (ADB) raised $1.25bn via a 5Y FRN bond, 1bp inside the initial guidance of SOFR+29bp area. The bonds have expected ratings of Aaa/AAA.

New Bonds Pipeline

- Shinhan Bank hires for $ Green bond

- Aluminium Corporation of China hires for $ bond

- Petron hires for $ 7NC4 bond

- Electricity Generating (EGCO) hires for $ 7Y or 10Y bond

Rating Changes

- Qatar-Based Ezdan Holding Upgraded To ‘B-‘ From ‘CCC’ On Improved Liquidity From Sukuk Refinancing; Outlook Stable

- Marfrig Global Foods Upgraded To ‘BB+’ From ‘BB’ On Significant Influence On BRF And Controlled Leverage; Outlook Stable

- Moody’s downgrades Agile’s ratings to B2/B3; ratings on review for further downgrade

- Fitch Downgrades Zhenro Properties’ IDR to ‘RD’ on Completion of Exchange Offer

- Airbus SE Outlook Revised To Stable On Strong Operating Performance; ‘A/A-1’ Ratings Affirmed

Term of the Day

Duration

Duration or Macaulay Duration for a fixed income security is the weighted average time until repayment of the invested amount. Duration is measured in years and for coupon-bearing vanilla fixed-rate bonds, duration is less than the tenor of the bond. The higher the duration, the higher will be the change in a bond’s price for a given change in interest rates. Given duration’s weightage to coupon payments, it is a more-accurate measure of interest rate risk vs. the tenor of the bond. Higher the bond’s coupon, lower will be its duration; and higher the tenor, greater will be the bond’s duration, all else equal. For very long tenor bonds like century (100Y) bonds or very high coupon bonds, the duration is significantly less than the years to maturity. On the other hand, zero coupon bonds’ duration is equal to its tenor.

Austria’s 0.85% bond maturing in 2120 has a duration of ~59 years and its price is down 55% from its peak in late 2020 to 62.

Explore BondbloX Kristals – a basket of single bonds listed on the BondbloX Exchange following themes such as SGD REIT Perps, USD Bank Perps, and SGD Bank Perps. Avail an introductory discount of $1,000 for every purchase of $100,000 worth of BondbloX Kristals*. Click on the banner above to know more.

Talking Heads

On Favoring ‘Steady, Deliberate’ Series of Rate Hikes – Kansas City Fed President Esther George

Recognizing risks to the outlook “is not an argument for stalling the removal of accommodation, but it does suggest a steady, deliberate approach for the path of policy could provide space to monitor developments as they unfold. It is clear that removing accommodation is required. How much and how aggressively accommodation should be removed is far more uncertain… Given the state of the economy, with inflation at a 40-year high and the unemployment rate near record lows, moving expeditiously to a neutral stance of policy is appropriate”

On Half-Point Hike Depends on Economy in May – Richmond Fed President Thomas Barkin

“I’m open to it. I think the question — and we will make this decision when we get to the meeting in May — is how strong does the economy still look in terms of its ability to take rate increases and how high is inflation persisting. I’m looking at both of those and we’ll make our call in May.”

On An AA+ Rated Government Bond Down 55% Shows the Pain of Higher Rates\

Peter Boockvar, CIO at Bleakley Financial Group

“Duration bites right now and there is no better example than this bond. This is not a meme stock and not a high flying tech stock but a sovereign bond with an AA+ credit rating. The problem is the duration is so long and thanks to the enticement of the ECB at the time, the coupon is just 0.85%

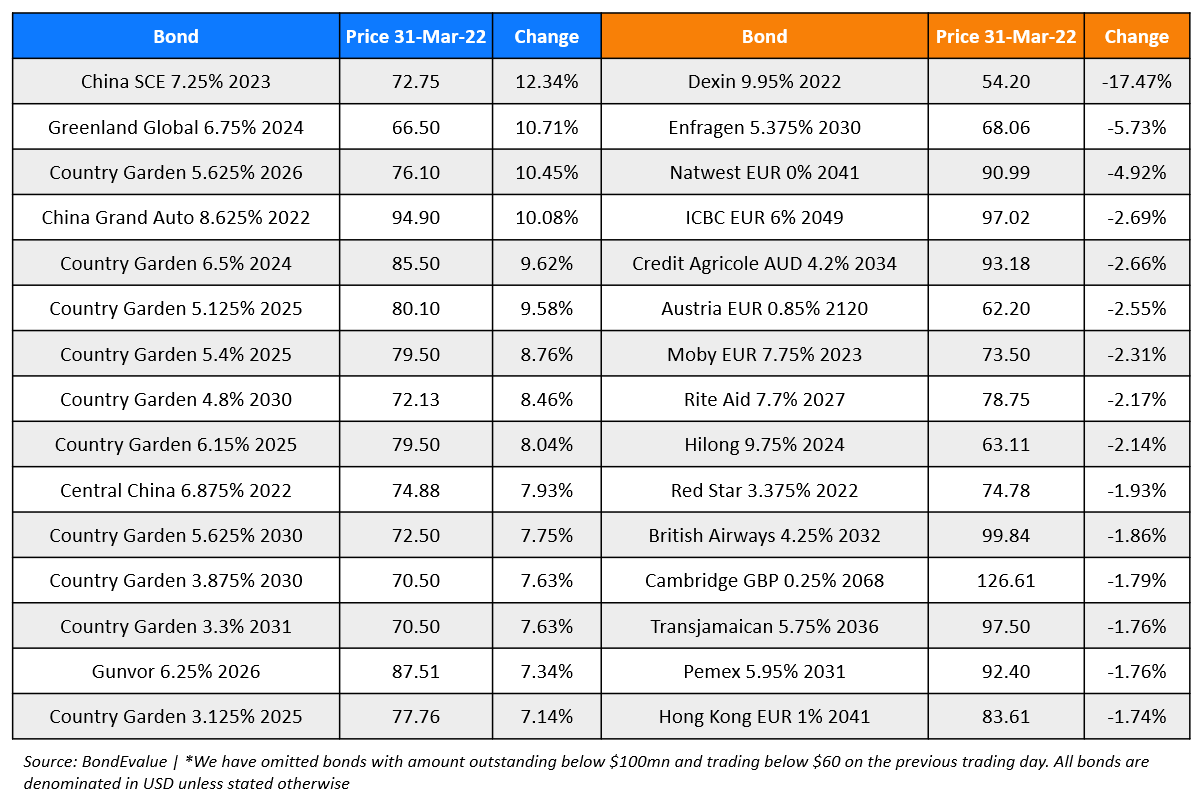

Top Gainers & Losers – 31-Mar-22*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.