This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

November 2023: Bullish Month for Dollar Bonds as 95% End Higher

December 1, 2023

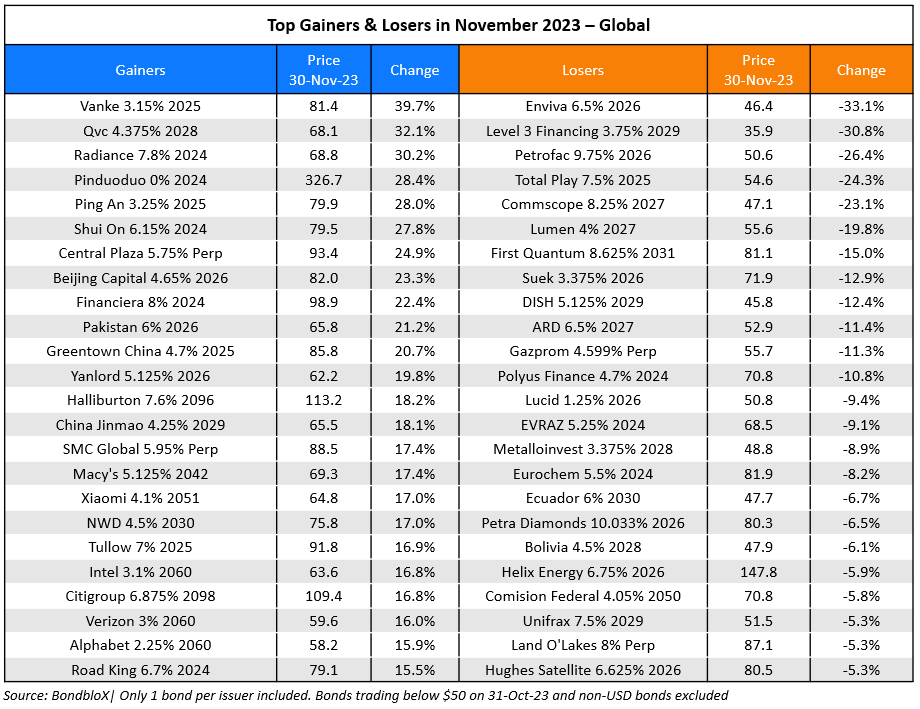

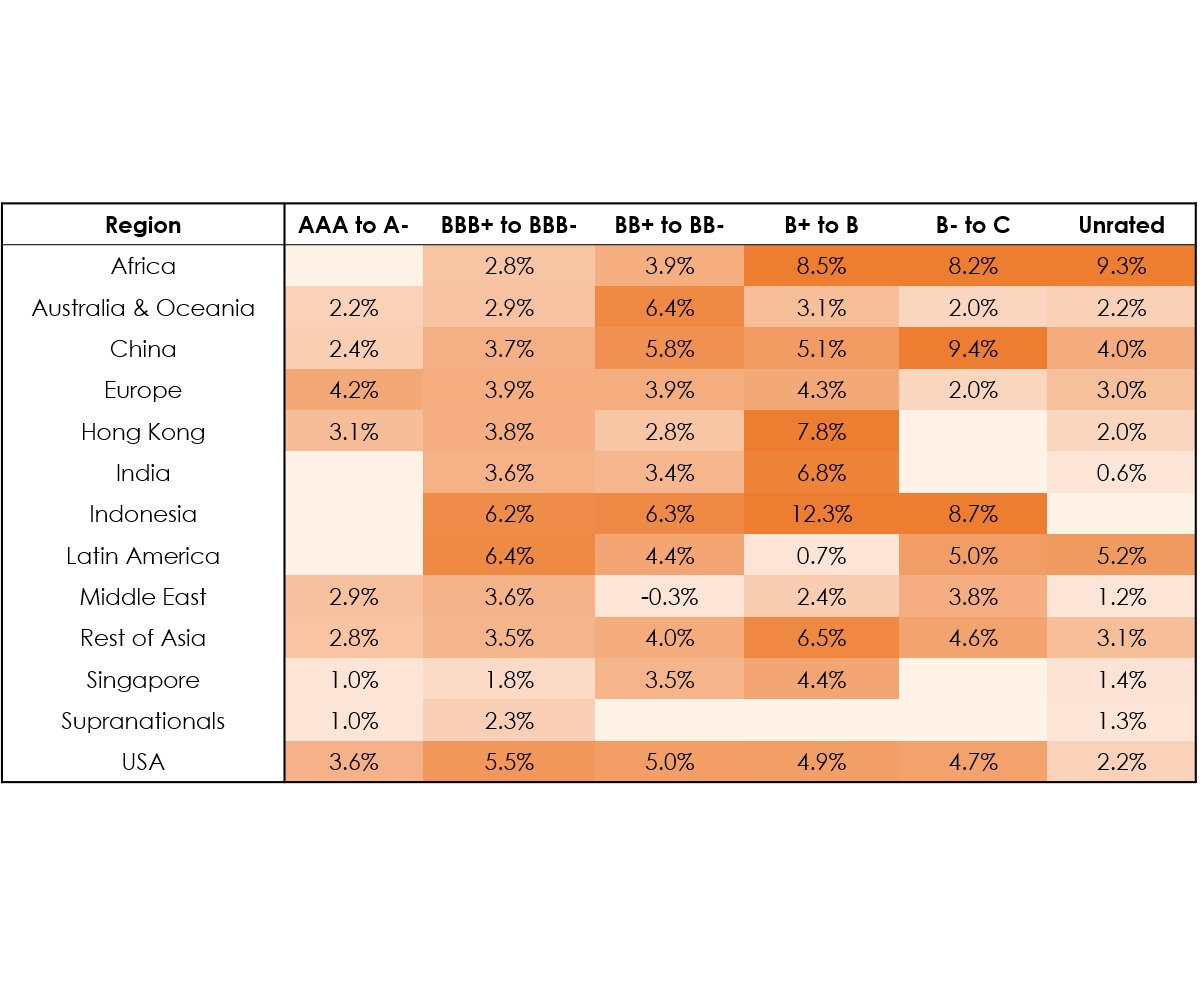

The month of November saw a major boost for bond markets with a whopping 95% of dollar bonds ending higher. Both, investment grade and high yield bonds showed almost equally strong performances – 97% of IG bonds ended in the green and 90% of HY bonds ended higher. This marks a reversal to the trend of three consecutive months of negative returns for bonds. With 10Y Treasury yields falling sharply by as much as 60bp through the month (see chart below), spreads across IG and HY dropped significantly by 17bp and 117bp to 63bp and 400bp respectively. This is the tightest level for US HY spreads since April 2022. The Asia ex-Japan dollar bond market witnessed its best performance since November 2022, up 3.6% last month.

November saw a massive rally in Treasuries as yields significantly came off their highs and the curve flattened. The 2Y yield fell 38bp to 4.71% and the 10Y yield fell 61bp to 4.33% during the month. The 2s10s curve bull flattened by 22bp during the month to -38bp currently. While the US economy continued to show resilience, the broad softening trend in inflation and initial signs of weaker data saw FOMC members indicate the possibility of either a pause or the end of rate hikes. US Headline CPI for October 2023 rose by 3.2%, lower than expectations of 3.3% and the previous month’s 3.7%. Core CPI came at 4.0%, lower than expectations and the previous month's 4.1% print. Markets priced out any further hikes by the Fed and many analysts expect the Fed to cut rates in the second half of 2024. Besides, the ISM Manufacturing Index fell 2.3 points in October, the biggest monthly decrease in over a year, to 46.7. Similarly, NFP for October rose by 150k, lower than the surveyed 180k and last month's 336k. Moreover, the US Treasury surprised markets with a slowdown in the pace of increases in its quarterly debt issuances. Owing to all of the above coupled with market sentiment, Treasury yields dropped and corporate bonds across the spectrum witnessed a rally.

In the IG space, the biggest gainers were long-dated bonds of corporates like Apple, Amazon, Alphabet, Salesforce, Boeing, Verizon and several others maturing over 15-20 years from today, thanks to the sharp drop in Treasury yields. Also, popular gainers included Chinese property developers and related REITS like Beijing Capital, China Vanke and Jinmao on the back of the government drafting a ‘white list’ of 50 developers, both private and state-owned, to be eligible for a range of funding options to help the property market. Other gainers included Macy's that rallied over 15% after better than expected Q3 results.

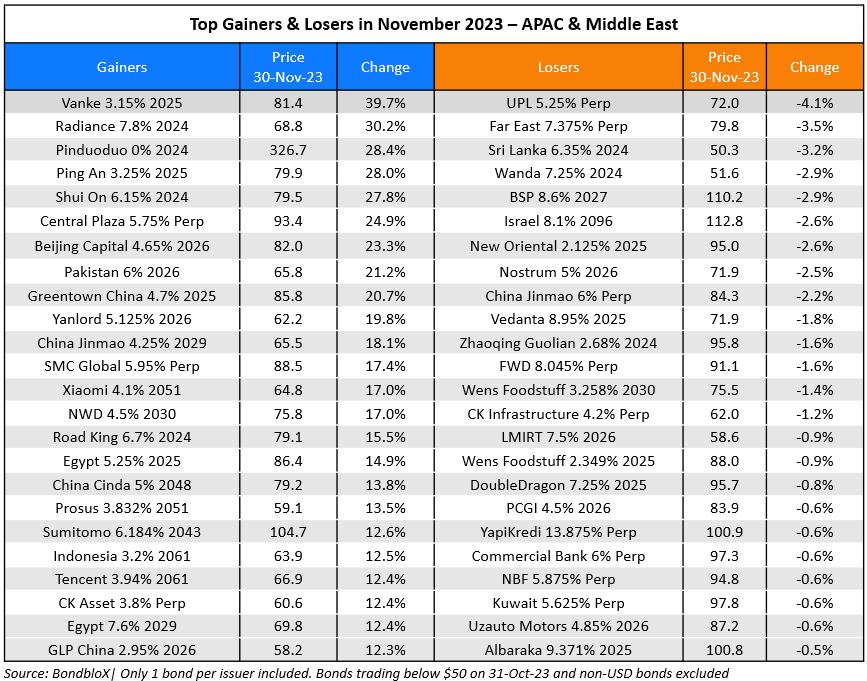

In the HY space, gainers included Chinese corporates related to the real estate sector like Ping An, Central Plaza, Greentown, Road King, Yanlord, Radiance Holdings and others. Other top gainers included Pakistan's dollar bonds that rose ~20% after it received a $700mn agreement from the IMFs executive board, improved funding prospects and news of political stability. Other gainers included Mexico's Financiera Independencia, America's QVC, the Russian sovereign etc. Besides, Hong Kong real estate companies like Shui On and NWD also saw their dollar bonds gain over 15%. Among the biggest losers were bonds of Lumen and its acquired company Level 3 Financing, that fell as much as 30% on continued downgrades and financial difficulties that it continues to face amid $9bn in net losses. Other popular losers in the HY space were bonds of DISH Network that sank ~15% points across the curve after reporting weak earnings, missing estimates by a large margin.

Issuance Volumes

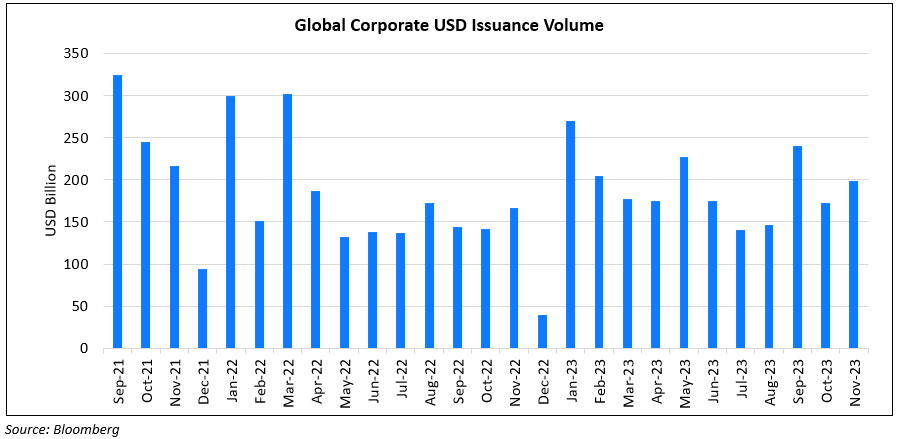

Global corporate dollar bond issuances stood at $199bn in November, 15% higher than October. As compared to November 2022, issuance volumes were up 20% YoY. 80% of the issuance volumes came from IG issuers with HY comprising 16% and unrated issuers taking the remainder.

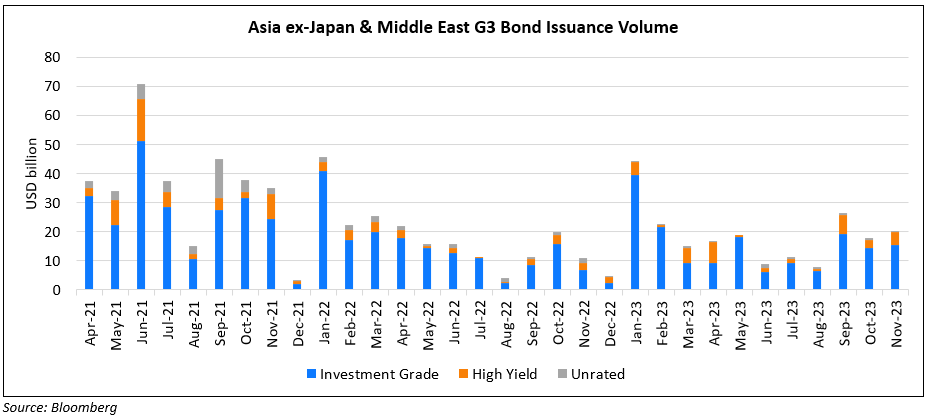

Asia ex-Japan & Middle East G3 issuance stood at $20.4bn, up, 14% MoM and 83% YoY. 76% of the volumes came from IG issuers with HY issuing 22% and unrated issuers taking the rest.

Largest Deals

The largest deals globally were led by led by several big banks across the US & Europe - Morgan Stanley’s $6bn four-trancher, Santander's $3.75bn three-part deal and UBS’s $3.5bn dual-trancher led the table, followed by Intesa Sanpaolo and SocGen's $3bn and €2.25bn two-tranchers each and HSBC’s $2bn deal. Besides, RTX’s $6bn five-trancher and Tapestry’s $4.5bn five-trancher also featured among the largest deals. Among the sovereigns, Colombia's $2.5bn two-tranche deal and Brazil $2bn issuance led the tables.

In the APAC and Middle East region, deal volumes were led by Westpac raising $3.5bn via a four-trancher and Indonesia’s $2bn dual-tranche deal. This was followed by NAB’s $1.5bn issuance, CCB’s ~$1.4bn dual-currency three-trancher.

Top Gainers & Losers

Go back to Latest bond Market News

Related Posts:

Bond Yields – Explained

November 16, 2018

Bond Investors Up $75.4 Billion in 1Q19

April 10, 2019

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.