This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Q1 2024: Dollar Bonds Hold Steady While Yield Curve Shifts Parallelly Higher

March 31, 2024

The first quarter of 2024 was a relatively modest one with 59% of dollar bonds in our universe delivering a negative price return (ex-coupon). While bonds were broadly mixed in January, they traded with a negative bias in February as strong economic data led markets to reprice their expectations of Fed rate cuts in 2024. Some of the losses were recouped in March as 89% of dollar bonds ended in the green. During the month, 92% of IG bonds and 80% of HY bonds ended higher.

Given the continued resilience in the US economy, the US Treasury yield curve shifted parallelly higher during the quarter by about 20bp across the 2Y up to the 30Y. Non-farm Payrolls (NFP) continued to stay solid at over 200k and wage inflation held steady at 4.3-4.4%. While US CPI trended slightly lower towards 3.1-3.2%, the pace of deceleration was slower than expected. Additionally, hard data points including GDP, retail sales and durable goods orders continued to indicate a resilient economy. This first lead to a reduction in the expectations of the number of rate cuts by the Fed (from 150bp to 75bp in rate cuts in 2024) and later, a delay in the timeline for the expected first rate cut (from March to June 2024).

The Asian HY space saw the biggest gains in Q1, up by over 6.3%; this space also saw the largest tightening in Z-Spreads, having tightened over 100bp to 583bp. The LatAm dollar bond index followed, with a 2.9% gain and the US HY index that rose 1.5%.

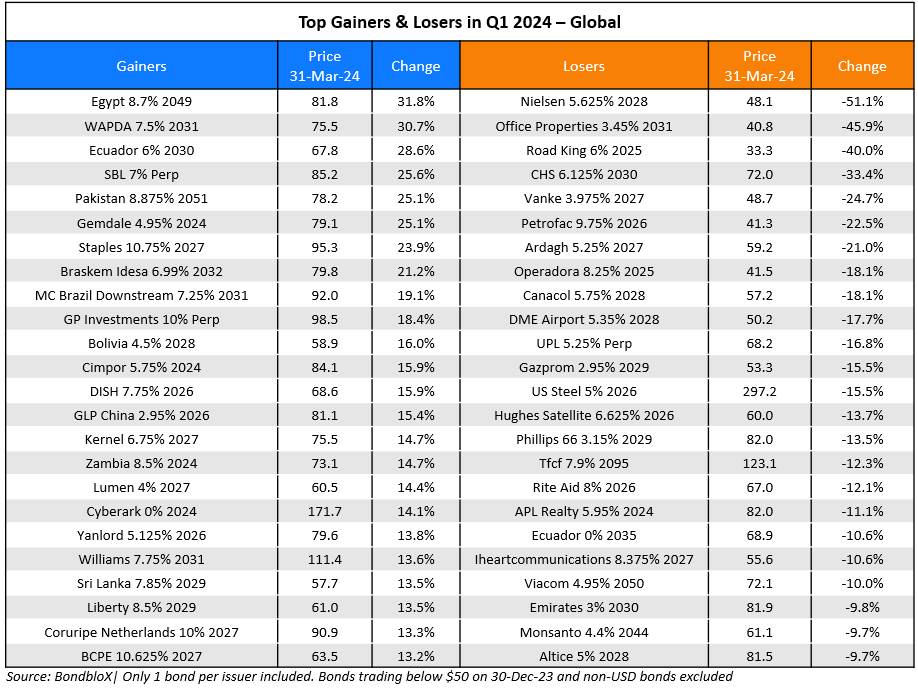

Some of the top gainers in the IG-space included American insurer RGA's 2031s that rose 16%, pipelines company Williams' 2031s that rose 13% and Carvana's 2031s that rallied 11%. The biggest drop in dollar bonds were seen in China Vanke, beginning with reports that it was negotiating with lenders to delay payments. As the developer continues to face financial stress, it has now been downgraded two notches to HY-status of BB+ by Fitch.

In the HY space, Egypt's dollar bonds were among the top gainers after several positive updates. This included striking an investment deal with the UAE for $35bn, followed by its 30% currency devaluation and subsequent 600bp rate hike that saw it secure an $8bn IMF deal. Pakistan's dollar bonds featured in the gainers list, up ~18% as it came closer to securing an IMF loan facility. Braskem’s dollar bonds also were among the top gainers as concerns over its mine rupture receded, coupled with reports that it received interest from Kuwait’s PIC and Saudi’s Aramco to acquire a stake in it. Road King’s dollar bonds were the biggest loser amid the broad sell-off in Chinese developers’ bonds after persistently weak sales. Also, UPL's dollar bonds featured amongst the large losers, down over 15%, after it became a fallen angel on its downgrade to Ba1 from Baa3 by Moody’s given weak quarterly results.

Issuance Volumes

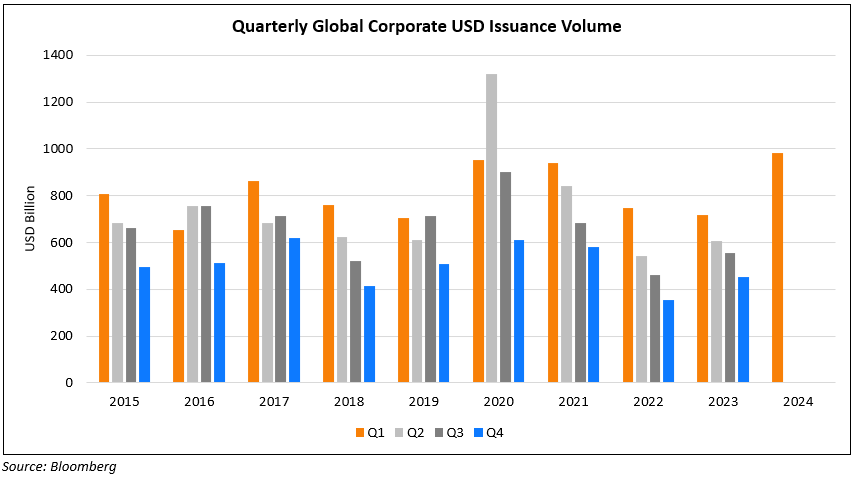

In Q1 2024, global corporate dollar bond issuances stood at $983bn, 65% higher than the prior quarter which was at $593bn. In comparison to Q3 2022, issuance volumes were 20% higher. Issuance volumes were primarily helped by May, which saw $227bn in new bond deals.

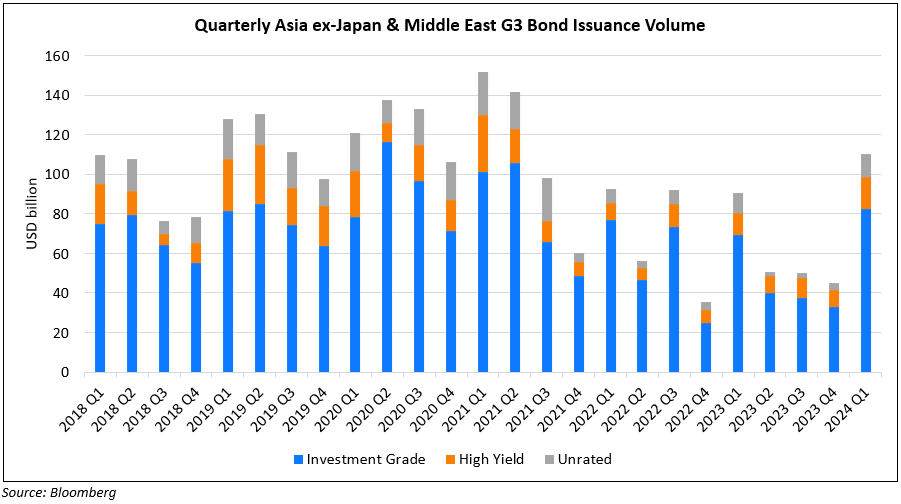

Asia ex-Japan & Middle East G3 issuances in Q1 2024 stood at over $110bn, 2.4x that of Q1 2023, and 21% higher than that of Q4 2023. The region also recorded its highest issuance volumes since Q2 2021 where volumes stood at over $141bn, prior to the Chinese real estate sector's impending collapse. 74% of the volumes in the recently concluded quarter came from IG issuers while HY contributed to 15% of deal volumes and the remainder was taken up by unrated issuers.

Largest Deals

The largest deals globally in Q1 were led by AbbVie’s $15bn and Cisco’s $13.5bn seven-part deals, followed by Saudi Arabia’s $12bn four-trancher. Besides these, big banks also topped the tables including JPMorgan's and Wells Fargo’s $8.5bn and $8bn four-trancher deals each, SocGen’s $5bn five-trancher, Lloyds' ~$4.35bn dual-currency issuance, Barclays’ $4.5bn and Santander’s $4bn four-part deals each.

In the APAC & Middle East region, apart from Saudi Arabia’s $12bn deal, there were large issuances. This was led by Saudi PIF’s $5bn three-tranche sukuk, ANZ’s $4.75bn three-trancher, NAB’s $3.25bn and KDB’s $3bn four-part and two-part deals respectively.

Top Gainers & Losers

Go back to Latest bond Market News

Related Posts:

Bond Yields – Explained

November 16, 2018

Bond Investors Up $75.4 Billion in 1Q19

April 10, 2019

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.