This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Treasuries Edge Lower Post CPI Data

March 13, 2024

US Treasury yields moved higher across the curve by 5-6bp. US Headline CPI rose 3.2% YoY in February, slightly higher than both, the expectations and the prior reading of 3.1%. Core CPI rose 3.8%, higher than expectations of 3.7% but lower than the prior reading of 3.9%. Market expectations for the Fed’s first rate cut were not impacted much following the inflation prints, with a 25bp rate cut in June still being priced with a 70% probability. Credit markets saw US IG CDS spreads tighten 1.1bp and HY spreads tighten by 5.7bp. Looking at equity indices, S&P and Nasdaq rallied 1.1% and 1.5% respectively.

European equity indices were higher too. European IG CDS spreads tightened 0.9bp and HY spreads were 2.1bp tighter. Asian equity markets have opened mixed today. Asia ex-Japan IG CDS spreads were 1bp tighter.

New Bond Issues

Goldman Sachs raised $3bn via a two-part deal. It raised $2.25bn via a 3NC2 bond at a yield of 5.283%, 22bp inside initial guidance of T+90bp area. It also raised $750mn via a 3NC2 FRN at a yield of SOFR+77bp vs initial guidance of SOFR equivalent. The new 3NC2 fixed rated notes were priced at a new issue premium of 22.3bp over its existing 1.431% March 2027s that currently yield 5.06%. Both notes are rated A1/A+/A+. Proceeds will be used for general corporate purposes.

Avic International Leasing raised $500mn via a 3Y bond at a yield of 5.153%, 42.5bp inside initial guidance of T+130bp area. The notes are rated A-, and proceeds will be used for debt replacement.

New Bond Pipeline

- EHi Car Services hires for $ bond

- Shinhan Bank hires for bond

Rating Changes

-

Moody’s downgrades CommScope’s CFR to Caa2; outlook negative

- EQT Corp.’s Outlook Revised To Negative On Announced Transaction; ‘BBB-‘ Ratings Affirmed

- Various Rating Actions Taken On Portuguese Banks Amid Easing Economic Risks

-

Moody’s changes outlook to positive for Ferroglobe; affirms B2 rating

Term of the Day

Standby Letter of Credit (SBLC)

Standby Letter of Credit (SBLC) is a note issued by the buyer’s bank to the seller’s bank, where the former guarantees to pay a sum of money to the latter if the buyer defaults on the agreement. Particularly in the shipping of goods, SBLCs are used to reduce risks associated with the transaction on unforeseen events leading to a default. Bonds backed by the above structure are called SBLC-Backed Bonds. Unlike guarantees, which are direct obligations of a bank to cover the timely payment of related bonds, SBLCs require trustees of the bonds to provide demand notices to the banks in the event that issuers fail to make bond payments.

Talking Heads

On Shorting Japan Government Bonds

Mark Dowding, chief investment officer at RBC BlueBay Asset Management

“This is the largest macro-risk position we are currently running as it offers the best risk-rewards. We are running short JGBs and see real opportunity in the trade.”

“Ten-year Japan bond yields are currently “supported at levels which are artificially rich”. It is possible the BOJ could push back its rate hike to April, but rather than the timing, the more interesting aspect will be indications on the future trajectory of rates in the country.”

On Going Slow to Avoid Devastation

Ken Griffin, founder of Citadel Securities

“Pausing and then changing direction back toward higher rates quickly, that would, be the most devastating course of action to pursue. So I think they’re going to be a bit slower than people were expecting.”

On Risk of Fed QT Tapering Starting from Later Date

Peter Boockvar, chief investment officer at Bleakley Financial Group

“We’re nearing a point where QT starts to exceed the reduction in the Fed’s reverse repo facility and liquidity starts to drain as a result. That is more relevant now than whether the Fed cuts once, twice, three times or not at all this year off a 5.33% effective fed funds rate.”

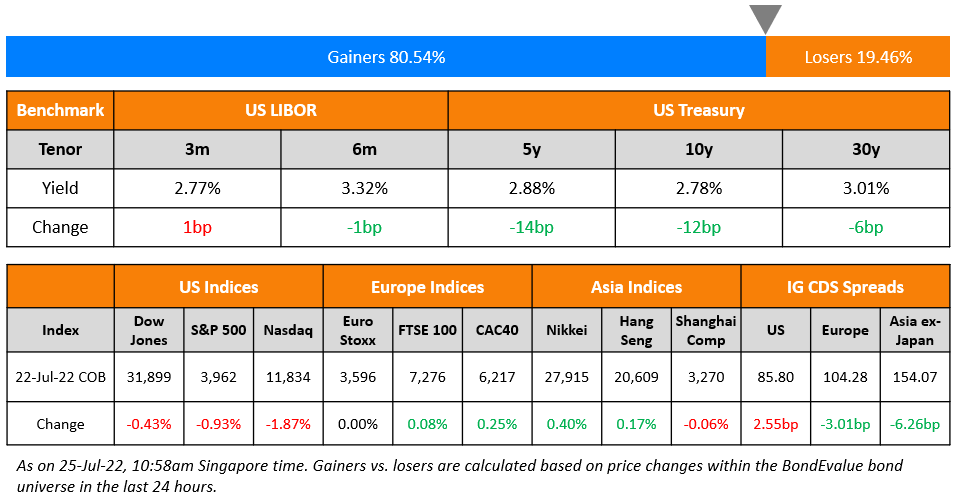

Top Gainers & Losers- 13-March-24*

Other News

Angola Plans Foreign-Currency Bond Sale to Boost FX Liquidity

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.